7 Under The Radar Swedish Compounders You Need To Know!

Sweden is often overlooked by investors. But Sweden offers high-quality compounders Wall Street isn't paying attention to!

Welcome back, Fluenteers! 👋🏻

Sweden is a favorite on my list of countries to live in and invest in. Besides high records of excellent standards of living, equality, and prosperity, Sweden offers high-quality compounders. These are companies that hedge funds, money managers, pension funds, and even retail investors tend to miss.

Here are seven under-the-radar high-quality companies in Sweden.

Happy compounding!

Swedish Compounder #7: Mycronic AB (Ticker: $MYCR)

Built for precision. Trusted for complexity.

Mycronic designs high-end production equipment for electronics manufacturing.

Their machines enable the precise, the intricate, the almost impossible.

Electronics aren’t getting simpler. They’re getting denser. Smaller. Faster.

That’s where Mycronic thrives.

Where perfection is mandatory

Where tolerances are razor-thin

Where mistakes cost millions

Mycronic doesn’t compete on price.

It competes on performance.

Core domains:

Surface Mount Technology (SMT) assembly

Photomask writers for semiconductors and displays

Advanced dispensing solutions

High-flexibility pick-and-place machines

Once embedded, rarely replaced.

Contracts don’t lock in switching costs.

They’re locked in by trust, training, and system compatibility.

A change risks production stability

A change risk yields rates

A change risks product quality

When speed and precision converge, Mycronic stays.

The install base builds the future.

Growth isn’t just from winning new orders.

It compounds inside the current footprint.

New equipment installations

Capacity upgrades

Maintenance contracts

Software enhancements

Spare parts and consumables

Every sale plants a seed.

Every upgrade strengthens the root.

Global scale. Local expertise.

Present in over 50 countries.

Sales engineers, not just salespeople.

On-site training

Immediate service support

Strong regional partnerships

Customers don’t just buy a machine.

They buy uptime, reliability, and long-term process stability.

Financially disciplined. Operationally sharp.

Gross margins: consistently high

Strong cash flow generation

Low capital intensity

R&D focused on next-generation demands

Secular growth drivers:

Increasing electronics miniaturization

Rising demand for advanced packaging

OLED and semiconductor photomask complexity

Growth in automotive, medical, and consumer electronics

Each trend makes Mycronic more critical.

Not louder. Just more essential.

This is a business for the patient. For the precise.

Mycronic isn’t chasing trends.

It’s shaping the future of electronics manufacturing.

Quiet excellence. Reliable compounding. Installed to stay.

When precision defines the product,

Mycronic doesn’t pitch.

It delivers.

Swedish Compounder #6: Vitec Software Group (Ticker: $VIT.B)

Focused by design. Specialized by choice.

Vitec Software Group develops industry-specific software for niche markets.

They don’t build general tools.

They build tailored solutions.

Deep verticals. Long-term partnerships.

Vitec serves professionals who rely on software built around their workflows.

Not the other way around.

Core focus areas:

Real estate management

Healthcare administration

Energy distribution

Construction project management

Auto service operations

Education and welfare systems

Niche markets. Complex needs.

Vitec’s software isn’t one-size-fits-all.

Each solution is developed for a specific profession, often shaped alongside the users.

Embedded in daily processes

Adapted to industry regulations

Built to fit how people actually work

High switching costs through specialization.

Clients don’t just use the software—they build their processes around it.

Data migration is difficult

Staff is deeply trained on Vitec’s systems

Integrations run across multiple business functions

When workflows are aligned, changing providers isn’t just inconvenient—it’s disruptive.

Growth through acquisition and long-term care.

Vitec grows by acquiring proven niche software providers and improving them over time.

Focus on profitable, well-established companies

Decentralized operations with local management

Continuous product development

Stable, recurring revenues

Each acquisition strengthens Vitec’s network.

Each system is nurtured, not overhauled.

Financial profile built for stability.

High proportion of recurring revenue

Strong cash flow conversion

Predictable growth from embedded solutions

Disciplined capital allocation

Customer base built to last.

Long-term contracts

Deep integration into customer operations

Low churn across industries

Secular drivers:

Increasing digitalization of specialized sectors

Growing demand for industry-specific process automation

Regulatory complexity requires tailored solutions

Strong need for reliable, local support

Vitec’s relevance grows as complexity grows.

Not because it scales fast, but because it scales right.

A steady, deliberate compounder.

Vitec doesn’t chase mass markets.

It builds quiet strength in focused segments.

When software needs to understand the industry,

Vitec is already there.

Swedish Compounder #5: Invisio AB (Ticker: $IVSO)

Designed for clarity. Engineered for survival.

Invisio develops advanced communication systems for demanding environments.

Their products enable clear, secure communication when conditions are harsh, chaotic, or life-threatening.

Focused on frontline users.

Invisio serves military personnel, first responders, and security forces.

Where communication is mission-critical

Where background noise is extreme

Where the equipment must perform, always

Invisio’s solutions aren’t optional.

They’re essential to the task.

Core offerings:

Tactical communication systems

Bone conduction headsets

Hearing protection with situational awareness

Integrated control units for multi-device connectivity

Built to meet real-world demands.

Invisio’s products are developed with direct user input.

Lightweight and unobtrusive

Resistant to dust, water, and impact

Seamlessly integrates with radios and intercom systems

Every detail serves a purpose.

Every component must endure.

High barriers to entry.

Switching providers is not simple.

Requires full system integration

Demands retraining of personnel

Involves rigorous procurement and testing cycles

Customers don’t change lightly—too much is at stake.

Growth is driven by long adoption cycles and expanding use cases.

Invisio builds relationships with defense organizations that can span decades.

Multi-year procurement processes

Continuous product upgrades

Follow-on orders for existing platforms

Expanding into adjacent markets like police and firefighting units

Each sale opens the door for years of system support and complementary products.

Financially resilient. Mission-aligned.

High gross margins reflecting specialized technology

Strong order intake visibility

Scalable production with focused R&D investments

Low working capital requirements

Secular tailwinds:

Growing defense budgets in key markets

Rising need for soldier modernization programs

Increasing importance of noise protection and clear communication in urban operations

Expanding civil defense and emergency response capabilities

Each trend makes Invisio’s role more essential, not just preferred.

Specialized. Resilient. Trusted.

Invisio doesn’t aim to be everywhere.

It focuses on being irreplaceable where it matters most.

When clarity and protection decide the outcome,

Invisio is already in the field.

Swedish Compounder #4: Note AB (Ticker: $NOTE)

Built for flexibility. Trusted for precision.

NOTE AB is a manufacturing partner for high-end electronics.

They provide contract manufacturing that feels like an extension of their customers’ own operations.

Specializing in complex, small-to-medium series.

NOTE isn’t a mass producer.

They focus on where flexibility, speed, and precision matter most.

Core capabilities:

PCB assembly

Box build and system integration

Prototyping to full-scale production

Testing and final assembly

Close to customers. Close to markets.

NOTE operates with local production hubs across Europe and China.

Enables short lead times

Supports rapid design changes

Minimizes logistics complexity

Customers value the proximity.

Not just for convenience, but for responsiveness.

Positioned as a long-term partner, not just a supplier.

Switching isn’t just about cost.

Processes are co-developed

Quality standards are embedded

Logistics and inventory management are tightly integrated

When NOTE becomes part of the customer’s value chain, it tends to stay.

Growth from existing relationships and expanding niches.

NOTE grows by deepening ties with existing customers and serving industries where precision and reliability are key.

Medtech

Industrial electronics

Defense applications

Communication equipment

Each partnership often expands over time.

Operationally disciplined. Financially focused.

Strong gross margins for the sector

High share of recurring orders

Efficient working capital management

Low capital intensity relative to production scale

Growth drivers:

Outsourcing trends in high-complexity manufacturing

Shorter product life cycles are increasing the need for flexible partners

Regional supply chain strategies driving nearshoring

Rising demand for electronics in the medical, defense, and industrial sectors

Each trend strengthens NOTE’s position as a responsive, local manufacturing partner.

Steady, structured, dependable.

NOTE doesn’t aim to be the biggest.

It aims to be the most reliable, flexible partner its customers can find.

When precision needs to move fast,

NOTE is ready to build.

Swedish Compounder #3: Teqnion AB (Ticker: $TEQ)

Built to endure. Structured to adapt.

Teqnion is a diversified industrial group.

They acquire and empower small, profitable niche companies.

Focused on resilience, not headlines.

Teqnion’s companies aren’t market leaders.

They don’t need to be.

They serve stable, often overlooked niches

They operate close to their customers

They specialize in essential, low-risk products

It’s not about size. It’s about durability.

Decentralized by principle.

Teqnion doesn’t integrate its companies.

It lets them run independently.

Local management stays in control

Decisions are made near the customer

Culture and processes are preserved

The head office doesn’t micromanage.

It supports.

Disciplined acquirer. Patient builder.

Teqnion focuses on:

Companies with stable cash flows

Low cyclicality

Strong customer ties

Proven profitability

Each acquisition is meant to hold forever.

No turnarounds

No forced synergies

No fixed exit horizon

Growth is self-funded. Risk is contained.

Modest financial leverage

Cash flow from subsidiaries funds new acquisitions

Conservative capital structure

Small, manageable deal sizes

Teqnion grows in layers. Carefully. Quietly.

Portfolio is built for the long haul.

Core segments include:

Industrial components

Safety equipment

Automation solutions

Niche production services

Every company is selected for its ability to thrive without constant oversight.

Tailwinds in Teqnion’s favor:

Aging industrial infrastructure needs ongoing service and replacement parts

Increasing demand for flexible, small-batch production

Stable need for safety and precision equipment

Owners of small businesses seeking succession solutions

Each trend quietly expands Teqnion’s opportunity set.

Steady hands. Selective growth. Durable cash flows.

Teqnion doesn’t chase scale.

It accumulates resilience.

When businesses need a permanent home,

Teqnion is built to hold.

Swedish Compounder #2: Dedicare AB (Ticker: $DEDI)

Staffing where it matters most.

Dedicare is a specialist in healthcare and social work staffing.

They connect qualified professionals with organizations in need—quickly, reliably, and across borders.

Focused on critical roles.

Dedicare doesn’t fill just any vacancy.

They focus on where skills are scarce and needs are urgent.

Core areas:

Doctors and nurses

Social workers

Life science professionals

Special education staff

When essential services need support, Dedicare is often the first call.

A cross-border network.

Dedicare operates in Sweden, Norway, Denmark, Finland, and the UK.

Their international reach enables fast, flexible staffing across regions.

Broad pool of vetted professionals

Deep understanding of local regulations

Strong relationships with public and private healthcare providers

Reliable when time is short.

Rapid response to temporary staffing gaps

Scalable for long-term assignments

Handles recruitment, vetting, contracts, and relocation logistics

Clients don’t just hire people.

They hire peace of mind.

Specialized staffing drives retention.

Dedicare focuses on building trusted relationships.

High client retention

Strong candidate loyalty

Deep specialization increases placement success

When a provider understands both the job and the industry, they tend to stay involved.

Financially sound. Operationally responsive.

Revenue is driven by long-term staffing needs, not short-term cycles

Asset-light business model

Strong cash flow generation

Regional diversification reduces risk

Tailwinds behind the model:

Growing staff shortages across healthcare systems

Rising demand for cross-border mobility of medical professionals

Increased outsourcing of recruitment and staffing

Aging populations are driving long-term healthcare demand

Each structural trend extends Dedicare’s relevance.

A partner to essential services. A bridge for critical skills.

Dedicare isn’t in the business of general staffing.

They specialize where the stakes are highest.

When care can’t wait,

Dedicare is ready.

Swedish Compounder #1: Intrum AB (Ticker: $INTRUM)

Managing complexity. Enabling recovery.

Intrum is Europe’s leading credit management company.

They help individuals, businesses, and financial institutions resolve unpaid debts ethically and efficiently.

Focused on solutions, not just collections.

Intrum doesn’t simply recover payments.

They manage the full lifecycle of credit and debt.

Core services:

Credit management

Debt collection

Purchase of non-performing loan (NPL) portfolios

Advisory on credit risk and cash flow improvement

Intrum works at the intersection of finance, regulation, and customer care.

Built for scale. Designed for trust.

Presence across 20+ countries.

Trusted by banks, telecom providers, utility companies, and public institutions.

Deep regulatory knowledge in each market

Multinational operations with local expertise

Large, diversified client base

Relationships are built on performance and compliance.

Strict adherence to regulatory frameworks

Focus on fair, respectful treatment of debtors

Systems aligned with data security and privacy standards

Intrum balances recovery with responsibility.

Growth through diversification and disciplined portfolio management.

Intrum’s model combines recurring service revenue with investment in purchased debt portfolios.

Long-term cash flow from portfolio returns

Steady income from credit management services

Balanced exposure across geographies and sectors

Each side of the business strengthens the other.

Operationally rigorous. Financially focused.

Strong cash flow generation

Prudent capital deployment

Debt portfolio purchases selected with disciplined return thresholds

Scalable platform for future growth

Structural trends supporting demand:

Rising consumer debt levels

Ongoing divestment of non-performing loans by banks

Increasing regulatory complexity requires professional credit management

Corporate focus on cash flow optimization

Each trend reinforces the need for experienced, compliant partners.

A steady hand in complex environments.

Intrum isn’t driven by short-term gains.

It’s built to manage long-term financial recovery.

When credit risks must be resolved,

Intrum provides the path forward.

Interested in more high-quality compounders? Check out more down here! 👇🏻

You won’t regret it.

🔥 Ready to go from reading about great businesses to owning them with conviction?

You’ve just gotten some of my archive of the best gems that no one talks about…

Now imagine having the full edge—every single week:

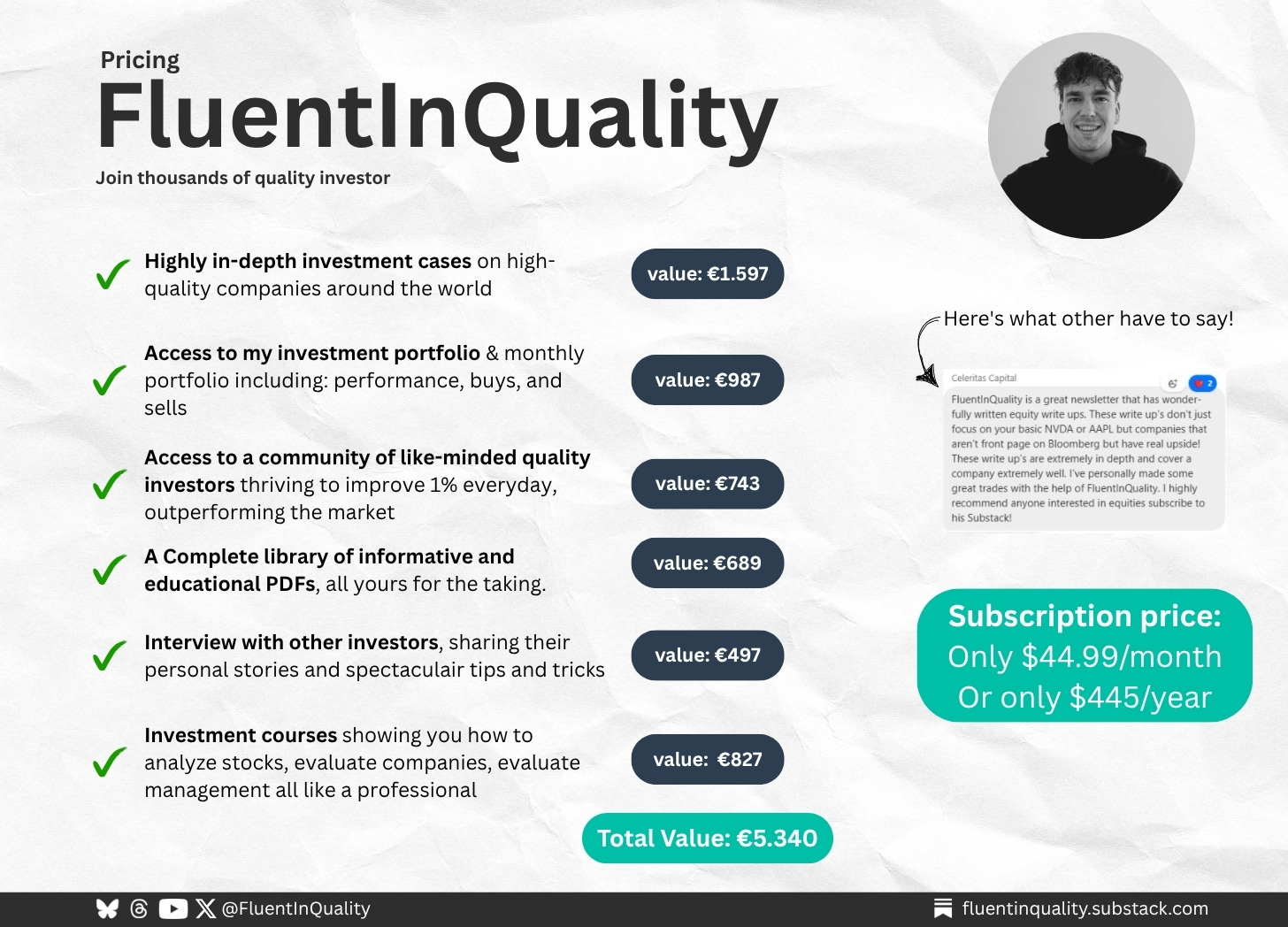

✔️ Full research reports and timeless deep dives (valued at €1,597)

✔️ Monthly buy/sell portfolio updates with commentary (€987)

✔️ Access to a private Discord of high-conviction investors (€743)

✔️ Tools, templates, investor interviews & PDF briefs (€2,013)

Total value: €5,340 — yours for just €44.99/month or €445/year.

No fluff. No noise. Just real work, trusted by 1,200+ long-term investors.

This isn’t just insight. It’s an investing advantage.

Delivered weekly. Backed by research. Built to compound.

🟢 Become one of The Fluent Few

Let’s build wealth the right way—brick by brick.

PS…. if you’re enjoying FluentInQuality, can you take 3 seconds to refer this edition to a friend? It will go a long way in helping me grow the newsletter (and bring more quality investors into the world).

Great investments don’t shout, they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.