Deep Dive: Life360, Inc. ($LIF)

~96M monthly active users globally, just turned profitable, targeting Gen Z and parent head-on, but there's missing something....

It’s a typical story of how I came across this business, a typical Peter Lynch style story.

I was hanging around with some friends at the bar. After having a good time, we slowly left one by one. We all said our goodbyes and told everyone, "Let us know when you arrive home safely." We always tell each other, and we are always sure to do so.

Then, all of a sudden, one friend said, ‘You know you all can see where I am going, how fast, and when I arrive home, right?’ Another friend said, 'We know, but it’s baked into us to say it.' Then I, and some other friends, said ‘What, how?’’ The friend showed me the app that those two were referring to.

It’s a fun UI experience app that shows where we are, how fast we’re going, whether there have been any emergencies, etc.

After downloading the app, messing around with it, and, of course, having other friends download it and connect with each other, I started seeing the value-accumulating aspect of this app.

After digging a bit more, I found heaps more features, like a pet feature that lets you buy hardware, place it in your dog's collar, and see where your dog is!

I knew there and then that I had to see if there was more to this business, and there is.

Here’s my deep dive on Life360, a stock I found in the Peter Lynch style.

What Will be Discussed?

Corporate Analysis

Business Overview

Revenue Breakdown

Executive Leadership

Management

Management Compensation

Management Value Creation

Competitive and Sustainable Advantages (Economic Moat)

Industry Analysis

Industry Growth Prospects

Competitive Benchmarking

Risk Assessment

Financial Stability

Asset Evaluation

Liability Assessment

Capital Structure

Expense Analysis

Capital Efficiency Review

Profitability Assessment

Profitability, Sustainability, and Margins

Cash Flow Analysis

Growth Projections & Expect Annual Return

Value Proposition

Dividend Analysis

Share Repurchase Programs

Debt Reduction Strategies

Bullish Thesis

Bearish Thesis

Valuation Assessment

Disclaimer: This content is for informational and educational purposes only. Nothing here constitutes investment advice, a solicitation, or a recommendation to buy or sell any security. Always consult a qualified financial advisor before making investment decisions.

I may hold positions in securities mentioned, which creates potential conflicts of interest that readers should factor into how they weigh my analysis. All analysis reflects my personal opinions and may contain errors, omissions, or outdated information — do not rely on it as a complete or accurate account of any company or security. Past performance of any security or strategy discussed is not indicative of future results. Any securities, funds, or assets mentioned are illustrative only and may not be suitable for your individual financial situation, risk tolerance, or investment objectives. You are solely responsible for conducting your own due diligence before acting on anything discussed here.

I make no representations or warranties, express or implied, as to the accuracy, completeness, or timeliness of the information provided. I accept no liability for any loss or damage arising from reliance on this content.

For full terms, see my complete disclaimer here.

Corporate Analysis

Business Overview

Life360 is a family-tracking app. You install it on everyone’s phones, and then you see where each other is on a map in real time.

Parents mostly use it to keep tabs on their children. You get a notification when your son or daughter arrives at school or when they get home safely. You can also see how fast someone is driving, which is either reassuring or a source of arguments, depending on your family.

Life360 also offers a feature that alerts you if someone’s phone battery is dying or if they’re in a car crash (it detects impact automatically and can call emergency services).

Some people love it for the peace of mind. Others, like the teens, find it quite suffocating. It’s one of those apps that works great if everyone in the family is on board, but could create friction if they’re not.

So, in short, it’s a ‘‘where's my family right now’’ app with some safety features bolted on.

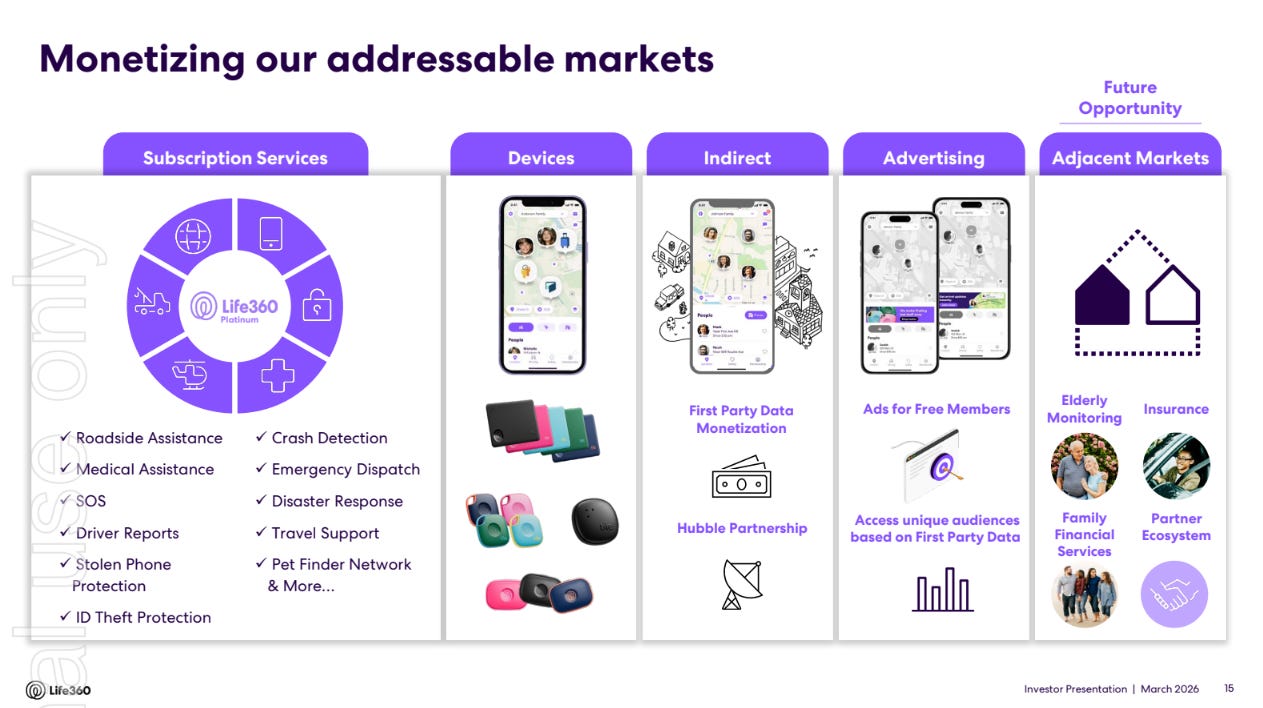

Revenue Breakdown

Life360 generates revenue via the following segments:

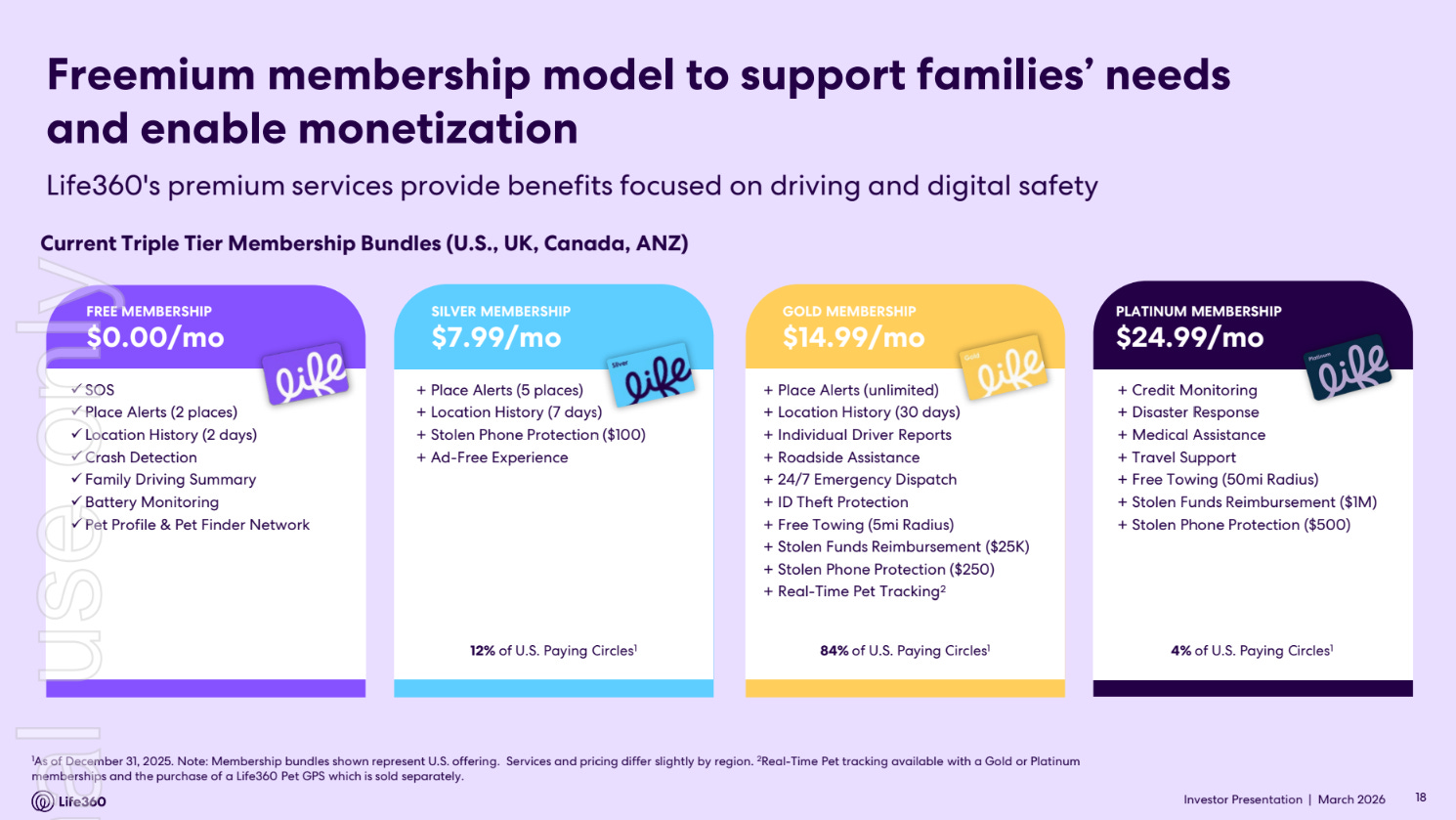

Subscriptions are the engine. $369M in 2025, up from just $25M in 2018. That's the premium membership families pay for to unlock features like more detailed location history, faster refresh rates, and roadside assistance. The free app gets you the basics, but it nudge you hard toward paying.

Hardware is the Tile tracker business. They acquired Tile (the little Bluetooth tracking tags you put on your keys/wallet) back in 2021. It's been flat at ~$52-58M the last few years, though. Not growing, just sitting there. Hardware is notoriously low-margin, too, so it probably looks better on paper than it does in reality.

"Other" is small but growing. $68M in 2025. This is data licensing and advertising, and honestly, this is the slightly uncomfortable one. Life360 has been known to sell anonymized location data to third parties. They've pulled back on some of that after bad press, but it's still a revenue line worth watching if you're thinking about the stock.

This is fundamentally a subscription SaaS business wearing a consumer app costume. The CAGR on subscriptions is 47% over 7 years, which is legitimately impressive. The question is whether growth can hold as they saturate the family-safety niche.

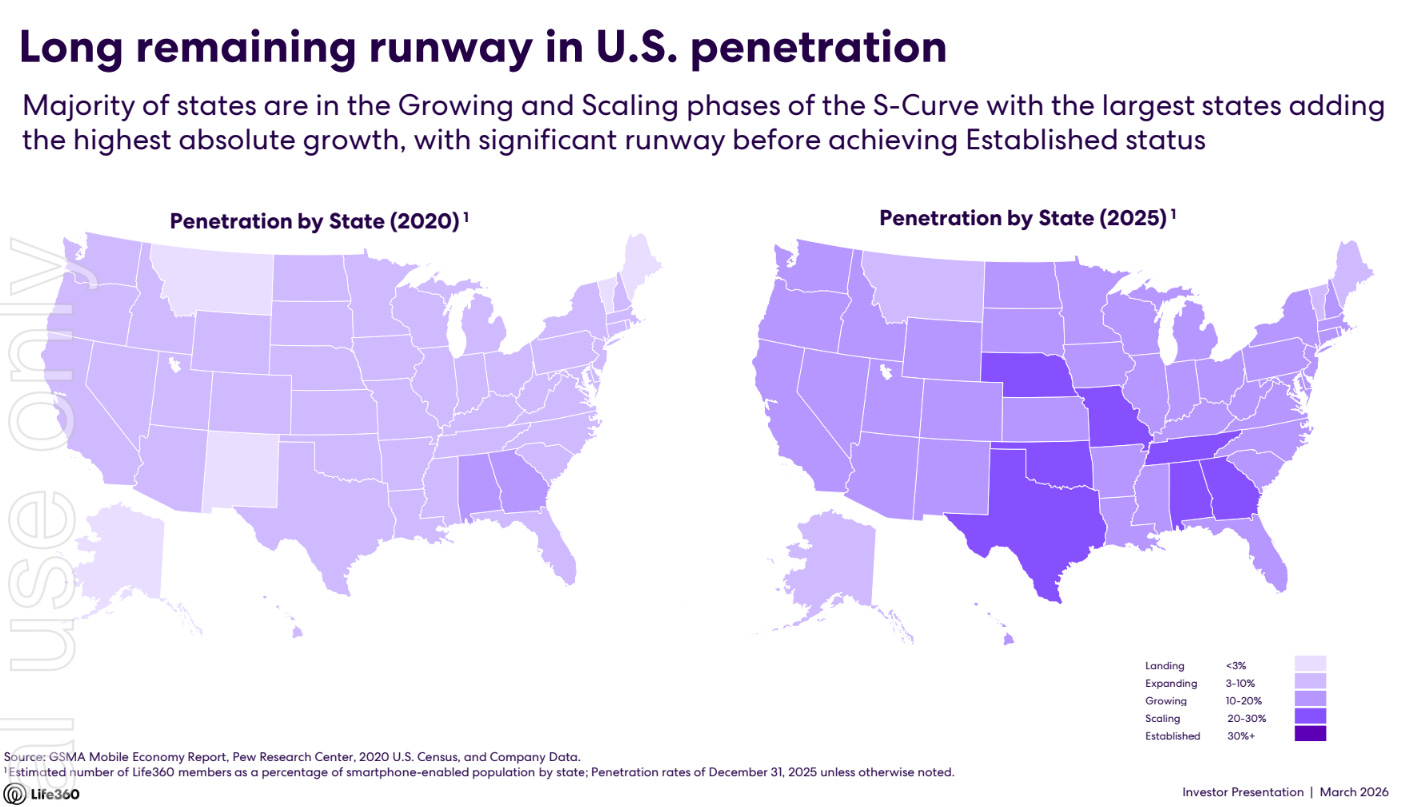

Most of their users are in the US, but families worrying about where their kids are is not an American thing. Europe, Latin America, Southeast Asia, there’s a real international growth story here if they execute. They’ve barely scratched it.

The Tile hardware could get interesting again. Right now, it’s flatlined, but if they deeply integrate Tile into the family safety experience, like your kid’s backpack has a Tile, and you track it through Life360, that’s a genuine ecosystem play. Apple AirTags showed there’s an appetite for this.

AI could actually be useful here. Imagine the app proactively flagging “Your teenager is driving erratically at 11pm on a Friday” rather than you having to check. That kind of smart alerting could justify higher subscription tiers and reduce churn.

Elder care is an untapped market. Right now, it’s mostly parents tracking kids. But adult children tracking aging parents? That market is massive and growing as populations age. They haven’t really gone there yet.

However, aside from some catalysts, there are potential headwinds.

Apple and Google are lurking. Apple already has Find My built into every iPhone for free. If Apple decides to go deeper into family safety, Life360 has a serious problem. You can’t out-resource Apple.

The data privacy thing won’t go away. The moment another journalist writes a big exposé about Life360 selling location data, the stock gets hit, and subscriber trust takes a beating. It’s an overhang that never fully disappears.

Churn risk as kids grow up. Their core customer is parents with young kids. Once the kids leave for college and stop tolerating the tracking, families cancel. They need to keep acquiring new young families faster than they’re losing older ones.

Subscription fatigue is real. Families are cutting every $10-15/month subscription that isn’t essential. In a tough economy, a “family tracking app” might not make the cut.

Great growth story so far, but the moat question is real. Subscriptions are sticky until they're not, and the thing keeping me up at night, if I owned this, would be Apple deciding to get serious about this space.

Executive Leadership

Management

Chris Hulls — the founder

This is the man who started it all. Co-founded Life360 back in the day, ran it as CEO for almost twenty years, and took it from a raw idea to the family safety platform it is today with millions of users worldwide. That’s a serious founder run, most CEOs don’t last that long, let alone the person who built the thing from scratch.

He’s recently stepped back from the day-to-day as CEO and moved into an Executive Chairman role, which basically means he’s still very much in the building, focused on long-term vision, product innovation, and specifically championing the free user experience. That last part is interesting because the free tier is how Life360 grows its funnel. Keeping someone with founder-level conviction focused on that is probably smart.

Before all of this, he served in the US Air Force and did a tour in Afghanistan. Then went to UC Berkeley and graduated with highest honors in Business Administration. So, not someone who just stumbled into tech, there’s genuine grit in the background.

Stepping from CEO to Executive Chairman after nearly two decades is worth watching. Sometimes it’s a graceful transition that keeps the founder’s vision alive. Sometimes it creates tension with the new CEO. With Lauren Antonoff now running the show, how well those two work together will matter a lot.

If Chris is the business brain behind Life360, Alex is the tech brain. Co-founded the company alongside Chris, has been on the board since 2010, and at various points ran both the engineering side as CTO and the broader business as President. So he was basically there for every critical scaling decision from scrappy startup to global platform.

What’s interesting about Alex is that he’s clearly not someone who just coasts on founder status. He’s already deep into his next thing, Hubble Network, where he’s co-founder and CEO. The pitch there is pretty wild, actually: they’re building the first global satellite network that talks directly to regular Bluetooth devices. Meaning your AirTag or Tile tracker could work anywhere on earth, no cell signal needed. If that works, it’s genuinely big. Notably, Life360 has already cut a strategic partnership deal with Hubble and invested $5M in it, so the two companies are linked.

Before Life360, he worked on Orbited, an open-source project for real-time browser communication. Classic early-internet builder type.

He studied computer science at Pomona College and Harvey Mudd, both serious schools for technical people.

The Hubble relationship is the thing to watch here. He’s a board member at Life360 and CEO of a company Life360 just invested in. That’s a related-party situation that the proxy even flags explicitly. Probably fine, but it’s worth keeping an eye on whether Hubble’s interests and Life360’s interests stay aligned over time.

Russell Burke — the CFO

So the CFO holding the purse strings is Russell Burke. He’s done this rodeo before, CFO stints at Sony Music, Weight Watchers, and Magic Leap, so he knows what it looks like to scale a consumer business fast and keep the finances from falling apart in the process. He’s got roots in both the US and Australia, which makes sense given Life360 is dual-listed on Nasdaq and the ASX.

What I like about him, from a “does management actually use the product” perspective, is that Russell literally lives the use case. He and his wife are on the East Coast tracking three daughters: one still at home, one at college, and one building her career on the West Coast. He’s not using it because he has to. His favorite features are the driving tools and location alerts. That’s a CFO who gets why customers pay for this thing.

Lauren Antonoff — the CEO

Lauren took over as CEO in 2025, and honestly, her background is pretty serious. Almost 20 years at Microsoft working on SharePoint and Office, so she knows how to build and scale products that millions of people actually use daily. Then she ran the SMB segment at GoDaddy as President before joining Life360 as COO in 2023 and stepping up to CEO.

The COO-to-CEO path is worth noting, she wasn’t parachuted in, she spent two years inside the business first learning the operations before taking the top job. That usually means fewer nasty surprises.

She also uses the app personally, tracking her husband, adult kids, and apparently her cats and dog too. Which is kind of funny, but also tells you the product has enough range that even the CEO finds daily utility in it.

If you wanted to design a CTO resume for a location-tracking platform, you’d basically draw up Justin’s. Instagram, Facebook, Lyft, Foursquare, that’s literally a masterclass in building consumer apps that need to work for millions of people simultaneously without falling over. Foursquare, in particular, is basically location data as a business, so he’s been in this exact world before.

What stands out is he’s not a “big company guy who theorizes about scale”, he’s someone who’s actually been in the engine room while these products were growing fast and chaotic. That’s exactly what you want when you’re trying to take a family app global.

He’s based in Austin with his wife and two kids, and his favorite feature is arrival alerts, knowing his kids got to school and practice safely without having to text them. Again, he uses the product for exactly the reason most customers do.

This is a pretty solid technical leadership hire. The risk with consumer platforms at scale is always reliability, if Life360 goes down or gives wrong location data at the wrong moment, trust evaporates fast. Having someone who kept Instagram and Lyft running under pressure is the right person to have solve that problem.

Management Compensation

Three buckets throughout: base salary, cash bonus tied to hitting targets, and equity (RSUs and performance-based RSUs). Roughly 75-87% of total pay is “at risk”, tied to the stock price or hitting goals. No fat guaranteed cheques. That’s the right foundation.

2023 — Pre-IPO holding pattern

This was essentially a quiet year on comp. Chris Hulls took home $1.9M total, but that included a $904K one-time retention bonus that had been sitting on the books since 2016, plus a $600K cash payment the board gave him because they literally couldn’t grant him equity that year. Strip those out, and it’s a modest CEO package. Russell Burke earned $2.3M, base $400K, bonus $220K, RSU grant worth $1.66M. Straightforward. Lauren Antonoff joined mid-year, so her $5.4M looks big, but most of it was a $4.8M signing RSU package to lure her away from GoDaddy. Susan Stick also joined mid-year with a similar deal. Performance linkage was weak this year, equity grants existed, but PRSUs didn’t yet. Pre-IPO holding pattern is the honest description.

2024 — IPO year, things got real

Revenue up 22% to $371.5M. First year of positive Adjusted EBITDA at $45.5M. The company is dual-listed on Nasdaq and ASX. Pay went up meaningfully.

Chris Hulls pulled in $4.4M total, base $515K, bonus $489K, and a $400K one-time IPO bonus on top. The bulk was equity. Russell Burke got $2.6M, also got a $450K IPO bonus, which is actually bigger than the CEO’s, which raised a few eyebrows. Lauren Antonoff got $2.7M as COO, with her guaranteed $2M second-anniversary RSU refresh landing, too.

The big structural upgrade in 2024 was introducing performance-based RSUs. For the first time, 40-60% of equity only vests if they actually hit revenue and EBITDA targets. They hit 134.9% of the target that year, so executives got paid well for genuinely good performance. That’s the alignment you want to see.

The CEO-to-median-employee pay ratio was 19.5:1. For a US tech company, that’s modest; most tech CEOs run 50-100x the median worker.

What wasn’t great was that the IPO bonuses felt like double-dipping.

Executives already had equity that appreciated massively when the company listed, then got additional cash bonuses on top just for the IPO happening. The board justified it, but it’s the kind of thing that makes investors roll their eyes. The say-on-pay vote at the 2024 meeting passed, but with low support, the company basically admitted it was “well below the level we desire.” Corporate-speak for shareholders not being happy. They’ve been engaging with investors since.

2025 — Landmark year, pay reflected it

Revenue jumped 32% to $489.5M. First-ever profitable year in the company's history. Adjusted EBITDA more than doubled to $93.2M. The biggest change was Lauren Antonoff becoming CEO in August 2025, with Chris Hulls moving to Executive Chairman.

Lauren’s base jumped to $515K, the same as what Hulls was earning as CEO. But the real number is her promotion equity package: $4.8M RSU grant vesting over four years, a target $3.6M performance RSU tied to 2026 revenue and EBITDA goals, and a target $3.6M relative TSR award benchmarked against the S&P Software and Services Index. That’s roughly $12M in new equity on top of everything she already had unvested. Big number, but she earned it. The business genuinely performed.

Continuing executives earned cash bonuses at 108.1% of target, and PRSUs were paid out at 112.1% of target. Given the results, it's hard to argue that those weren’t deserved. Russell Burke stayed steady, base $450K, bonus target 50%, same solid quiet-engine role he’s always played.

Chris Hulls stepped back financially as you’d expect from an Executive Chairman versus a CEO. Still very much in the building, still holds significant equity, just not running the day-to-day P&L anymore.

Susan Stick, as General Counsel, is gone, replaced by Matthew Cullen. No details yet on his package.

The overall arc

Going from 2023 to 2025, the compensation structure materially improved. In 2023, it was essentially discretionary with a weak performance linkage. In 2024, they introduced PRSUs and got shareholder pushback on quantum. In 2025, they added relative TSR awards, arguably the most shareholder-friendly equity structure there is, because you only get paid if the stock outperforms peers. The trajectory is clearly in the right direction.

The thing to keep watching is equity dilution.

They’ve been granting heavily to attract and retain talent, and with a share base around 76-77 million, that dilution adds up over time. It’s not alarming yet, but it’s a number worth tracking alongside the business performance story.

Management Value Creation

All three metrics, ROIC, ROCE, and ROE, are negative because the company has been losing money until recently. That’s literally it. All of these ratios have some form of profit in the numerator. No profit, or a net loss, means the ratio goes negative.

Life360 was burning cash for years while it invested heavily in growth, building the platform, acquiring Tile, scaling internationally, and hiring. The -112% ROIC in 2021 looks alarming, but it just means they were losing more than their entire invested capital base at the time.

The good news in the chart is the direction. That steep climb from -67% ROIC in 2022 to -4% by LTM is a company rapidly closing in on profitability. So these metrics are about to flip positive, which will be a big moment.

Why they’re the wrong lens right now

These are all backward-looking, accounting-based profitability metrics. They tell you how efficiently a company is generating profit from its capital base right now. The problem is they completely miss what Life360 actually is, a freemium subscription platform where you deliberately lose money upfront to acquire users cheaply, then monetize them over a long horizon.

Think about it this way. Life360 has roughly 96 million monthly active users, most of them free. Every one of those free users costs money to acquire and serve, but they’re also a massive monetization opportunity that doesn’t show up anywhere in ROIC, ROCE, or ROE. The returns on those users are deferred, sometimes for years.

That’s why I’ll be covering their KPIs as a value-accretive part from management and the business.

MAUs, Monthly Active Users, meaning every person who opens the app at least once a month, went from 19M in 2018 to 96M in 2025. That’s a 26% CAGR over seven years, almost entirely through word of mouth. No massive ad spend is driving that. Families tell other families. That’s the kind of organic growth that’s genuinely hard to buy.

Paying Circles grew from basically nothing to 3M at a 22% CAGR. A Circle is Life360’s term for a family group on the platform, so one Paying Circle might be two parents and three kids, all sharing location. It’s not individual subscribers, it’s family units paying. That distinction matters because it means the revenue per Circle understates how many actual humans are inside the product. Annualized Monthly Revenue, AMR, basically what their current monthly run rate looks like extrapolated to a full year, went from $19M to $478M. That’s a 537% total change.

ARPPC, Average Revenue Per Paying Circle, meaning how much each paying family unit spends annually, went from $80 in 2021 to $137 in 2025, a 74% increase over four years. That’s 14.9% per year. Think about what that means: they’re not just adding more subscribers, they’re getting more money from each one. Families are upgrading to higher tiers, adding features, and staying longer. That’s genuine pricing power in a consumer subscription business, which is rare and valuable. The Net Average Sales Price line in chart one is slightly declining at -5% CAGR, but that’s a different metric measuring hardware pricing, the subscription side is the opposite story.

The number of Tile tracking devices physically sold, declining from 6M units in 2021 to 4M in 2025, down 32% total. That looks bad on the surface, but it’s actually somewhat intentional. They’re exiting physical retail in 2026 and going direct-to-consumer online only. The Tile business was never the point. It’s a funnel into subscriptions. If hardware units decline but every device sold converts into a Life360 subscriber, that’s a better outcome than moving high volumes at a thin margin through Best Buy.

The subscription count, Number of Subscriptions, meaning individual paid membership plans, growing from 2M to 3M (88% total, 17% CAGR), alongside ARPPC growing 75%, tells you the real story. Fewer but more valuable paid relationships. That’s a quality-over-quantity shift that actually improves the business.

Here’s the thing that ties it all together.

They have 96M MAUs and only 3M Paying Circles. That’s roughly a 3% conversion rate on a massive free base. The freemium model, free app with basic features, paid tiers for the full experience, means most of those 96M people are using the product for nothing today, which costs Life360 money to serve but builds the habit and emotional lock-in that eventually converts them. Even in the US, where they’re most mature, penetration is only 16%. Internationally, it’s low single digits. So you’ve got a proven conversion machine, a growing ARPPC, a sticky product with emotional lock-in, and the vast majority of the addressable market still untouched. The growth in MAUs today is essentially the pipeline for paying subscribers in 2, 3, and 5 years.

Going back to the ROIC chart, all those negative returns make complete sense now. They were spending heavily to acquire and serve 96M free users who don’t generate revenue today but represent enormous future value. The accounting metrics punish that strategy. The KPIs reward it. AMR at $478M growing 36% year-over-year, ARPPC at $137 and climbing, MAUs still compounding at 26%, these are the numbers that tell you whether the machine is working.

The data together paint a picture of a business that has quietly built one of the stickiest consumer platforms on the planet, is still in early innings internationally, and is just now crossing into the profitability phase where all that deferred value starts showing up on the income statement. The ROIC chart is about to look very different over the next three years. That trajectory from -112% to -4% to now positive, that’s the whole investment thesis in one line, going up.

Competitive and Sustainable Advantages (Economic Moat)

This is arguably one of the most important parts of this deep dive. A business without an economic moat is not worth your capital. Why? Because disruption is lurking around the corner, it could potentially wipe out the business. If you’ve invested your capital into this business, it’s gone forever.

So, let’s go into great detail, figuring out if Life360 has an economic moat. If so, what does it look like?