Top 7 High-Quality Serial Acquirers You Should Know

Serial acquirers can make shareholders wealthy, extremely wealthy. With excellent capital allocation and vertical integrations, significant shareholder value is created.

Welcome back, Fluenteers!

Serial acquirers can be wealth-generating machines, especially if you pick the right ones. Picking the right one can be challenging, and therefore, I’ve compiled seven high-quality serial acquirers for you. All you need to do is evaluate them and add these compounders to your watchlist. When the time is right, all you need to do is STRIKE!

Here are seven high-quality serial acquirers!

7. Constellation Software (Ticker: $CSU)

Buy Small. Compound Quietly.

Constellation Software isn’t chasing headlines. It’s rewriting the playbook on software M&A.

This is not a growth story driven by hype.

It’s a machine engineered for quiet, repeatable excellence.

Constellation specializes in one thing:

Acquiring vertical market software businesses that others overlook.

Not for turnarounds.

Not for synergies.

But for what they already are: niche, profitable, essential.

While tech giants hunt for scale, Constellation builds networks.

Each acquisition adds another node to its decentralized empire:

Mission-critical software serving obscure but resilient markets

High switching costs, stable cash flows, loyal customers

Run independently with minimal interference from HQ

This isn’t about building a unified brand.

It’s about building a mosaic of enduring businesses.

Decentralization as a strategy.

Constellation doesn’t integrate—it liberates.

Founders stay. Cultures stay. Systems stay.

The value is in autonomy and alignment.

No rebrands

No bloated playbooks

Just proven operators staying in the driver’s seat

Each business contributes cash.

That cash funds the next smart acquisition.

Rinse, repeat, compound.

Capital discipline baked into the DNA.

This is one of the rare firms that prefers passing on a deal to overpaying for growth.

ROIC, not vanity metrics

Price sensitivity, not market cycles

Cash flow reinvestment, not dilution

Even when capital is cheap, Constellation remains stubbornly rational.

It’s how they’ve turned hundreds of small acquisitions into billions of value, without ever chasing trends.

More Berkshire than Big Tech.

If Berkshire had been built for software, it might look like this.

Multi-decade horizon

Owner-operator model

Relentless reinvestment of free cash flow

And while most tech companies overpromise and underdeliver,

Constellation barely markets itself—and still outperforms.

Optionality through discipline.

Each small bet creates:

Local monopoly economics

Geographic and sectoral diversification

Talent development within a decentralized structure

Its venture arm, TSS, mirrors the same formula, giving rise to its own serial acquirers under the umbrella.

Every layer adds optionality.

Every deal adds durability.

Constellation isn’t for everyone.

It doesn’t scream innovation.

It doesn’t chase quarterly narratives.

But if you value:

Consistent capital allocation

Rational operators

Quiet compounding over loud promises

Then this just might be the highest-quality compounder .

Constellation isn’t building an empire.

It’s building a legacy of software businesses—one smart acquisition at a time.

6. Danaher Corporation (Ticker: $DHR)

Precision Compounding. Built in the Lab.

Danaher doesn’t just acquire companies.

It engineers ecosystems—where innovation, margin, and mission coexist.

This isn’t Big Pharma.

And it’s not just another industrial roll-up.

Danaher is what happens when operational excellence meets scientific purpose.

The Danaher Business System isn’t a slogan. It’s the strategy.

While others buy growth and hope for the best, Danaher installs a system:

Lean manufacturing

Kaizen culture

Relentless performance tracking

Every acquisition becomes sharper.

Every team gets tools, not rules.

This is M&A with muscle memory.

From microscopes to molecules.

Danaher quietly transformed itself from a tools conglomerate into a biotech backbone:

Diagnostics (Cepheid, Beckman Coulter)

Life sciences (Cytiva, Pall)

Environmental & applied solutions

Its portfolio touches the core of global health, from research labs to ICU beds.

Not loud. Just vital.

Acquisition discipline is shaped by science.

Danaher doesn’t buy on scale.

It buys for strategic fit and long-term value creation.

Targets essential, defensible niches

Pays up only when it sees platform potential

Integrates with care—never haste

Its Cytiva acquisition (from GE) became a cornerstone of the pandemic response.

A $21 billion bet that already paid off.

Margins over mania.

Danaher’s edge isn’t just in what it buys—it’s how it runs it:

Operating margins consistently above peers

Strong free cash flow to reinvest

Minimal reliance on the goodwill fairy tales

While biotech valuations rise and fall, Danaher continues to extract real returns.

Compounder with a code.

Danaher’s secret? A repeatable code of:

Operational rigor

Industry focus

Cultural consistency

It doesn’t chase the spotlight, but commands respect in every boardroom it enters.

Optionality through specialization.

Every unit under Danaher adds to an ecosystem:

Academic research → biotech → diagnostics → patient care

Tools that feed insights, not just sales

Expansion into bioprocessing, gene therapy, and global health infrastructure

Each layer reinforces the next.

The flywheel turns, predictably.

Danaher isn’t sexy.

It’s surgical.

Not a momentum trade, but a machine built for decades.

If you believe M&A is a craft, not a shortcut, Danaher is the blueprint.

Operational excellence isn’t the goal.

It’s the baseline.

5. Roper Technologies (Ticker: $ROP)

It’s Not Industrial Anymore.

Don’t let the name fool you—Roper Technologies left the factory floor years ago.

What used to be an industrial roll-up is now a quiet force in mission-critical software.

Think healthcare, education, compliance, and billing—high-stakes, low-switching.

Roper doesn’t build trends.

It buys enduring infrastructure that businesses can’t run without.

This is software that sticks.

Roper’s acquisitions aren’t flashy. They’re foundational:

Medical data platforms that hospitals rely on

Insurance and compliance software

Education tech that districts renew year after year

Boring? Maybe.

But the margins say otherwise.

Recurring revenue, relentlessly pursued.

Roper isn’t in the volume game. It’s in the durability game.

Each acquisition brings:

High retention

Low capex

Strong free cash flow from Day 1

It’s not growth at any cost. It’s growth with discipline.

An acquirer with patience.

Roper has one of the most refined playbooks in modern M&A:

Buys niche market leaders

Pays based on cash yield, not comps

Leaves operations intact—no over-engineering

It doesn’t buy fixer-uppers.

It buys cash machines.

And it holds them. Often forever.

Margins like SaaS. A strategy like Berkshire.

Roper blends the best of both worlds:

60%+ gross margins

30%+ operating margins

Long-term compounding with capital-light assets

This isn’t a software rocket ship.

It’s a cruise liner with a map and a mission.

Under-the-radar and over-delivering.

Roper isn’t on CNBC.

It’s not tweeting product launches.

But while others chase headlines, it keeps stacking cash.

Revenue is stable through cycles

Reinvestment is methodical

Dividends grow alongside free cash flow

It’s a business built to not break.

Optionality through niche scale.

Roper’s portfolio may look scattered—healthcare, education, insurance—but it’s unified by:

Dominant positions in fragmented verticals

Pricing power from specialization

Long-term contracts that renew like clockwork

Each business adds ballast to the flywheel.

Roper doesn’t try to be everything.

It tries to be irreplaceable in what it owns.

If you're looking for flashy, look elsewhere.

If you want margin-rich, sticky software quietly compounding in the background, this is your stock.

This isn’t about software scale.

It’s about software stability.

And Roper has been delivering that for decades.

4. Judges Scientific (Ticker: $JDG)

Precision, Not Scale.

Judges Scientific isn’t chasing big markets.

It’s assembling a constellation of niche instrument makers—one carefully measured acquisition at a time.

There are no grandiose visions here.

Just tight execution, deep expertise, and relentless focus.

This is capitalism done with a ruler, not a megaphone.

Judges doesn’t integrate. It empowers.

Each acquisition stays independent.

Each brand retains its identity.

Each team continues to do what it does best—serving scientists, researchers, and engineers worldwide.

What binds them?

Essential instruments

Sticky customer bases

High margins with low capex

It’s a mosaic, not a machine.

Built for boring. And that’s the edge.

Judges buys small scientific instrument companies with:

Strong operating history

High repeat business

Recurring demand from labs, universities, and R&D centers

Think calorimeters, microreactors, laser diagnostics.

Not sexy—but critical.

The kind of gear you upgrade once every 10 years, from the same trusted supplier.

Acquisition philosophy: slow, steady, smart.

This is not private equity.

There’s no financial engineering.

Judges pay fair prices for real businesses with real cash flows—and then leave them alone.

No synergy hype

No flashy turnarounds

Just 20+ years of consistent bolt-ons

It has completed over 20 deals with a success rate that most M&A teams only dream of.

Margins through focus.

Despite its modest size, Judges delivers:

60%+ gross margins

High return on capital employed

Conservative debt management

Why? Because niche instruments mean pricing power.

And because the team doesn’t chase growth, it earns it.

Optionality in obscurity.

This is one of the few listed serial acquirers that still flies under most radars.

That’s by design.

No investor hype cycles

No buzzwords

Just methodical, long-term wealth creation

And with the UK’s deep pool of under-loved, under-scaled manufacturers, the runway remains long.

Judges isn’t for everyone.

It doesn’t dominate headlines.

It doesn’t throw capital around.

It doesn’t pretend to be a unicorn.

But if you believe in:

Capital discipline

Compounding through niche markets

Quiet excellence over loud ambition

Then, Judges Scientific might be one of the purest compounders you’ll find in Europe.

Small cap. Big discipline.

And it’s just getting started.

Before we get to the top 3…

If you’ve read this far, you’re not just browsing. You’re the kind of investor who wants to go deeper.

👇🏻 Subscribe now and become part of the Fluenteer inner circle.

3. Relx Plc (Ticker: $REL)

From Pages to Power.

RELX isn’t a publishing company anymore.

It’s a data and analytics machine—powering the decisions that shape science, law, and finance.

This isn’t about headlines or hot sectors.

It’s about infrastructure that professionals trust.

Day in, day out.

If Bloomberg had siblings in academia and regulation, they’d look like RELX.

Information, elevated.

RELX owns assets that others can't replicate:

Elsevier (scientific journals & medical content)

LexisNexis (legal, regulatory, and compliance data)

ICIS & FlightGlobal (pricing, trade, and transport intelligence)

It doesn’t sell news.

It sells confidence through validated, searchable, high-stakes information.

Built for professionals, not consumers.

RELX serves knowledge workers who demand:

Depth

Accuracy

Speed

Whether you’re diagnosing a rare disease, navigating international law, or modeling commodity flows, RELX data is often the first (and only) stop.

Its products don’t trend.

They endure.

A serial acquirer in disguise.

RELX doesn’t announce deals with fanfare.

But behind the scenes, it has quietly executed:

Dozens of tuck-in acquisitions

Strategic bolt-ons to enrich its data layers

New capabilities in AI, risk scoring, and predictive analytics

No platform bets. No hype cycles.

Just smart additions that enhance pricing power and retention.

Margins from mission-criticality.

RELX’s model is stunningly efficient:

Subscription-based revenue

High renewal rates

Low marginal cost of delivery

And once embedded, it rarely gets replaced.

That’s why:

Operating margins hover around 30%+

ROIC remains strong and consistent

Cash flow is both durable and growing

This is what defensibility looks like in digital disguise.

Optionality through layering.

Every division benefits from the other:

Legal tools powered by real-time risk data

Scientific research enhanced by AI-driven discovery

Compliance software strengthened by regulatory feeds

RELX isn’t a sum of its parts.

It’s a web, tightly woven around professionals’ daily workflows.

It doesn’t shout. It compounds.

RELX doesn’t need to tell a new story every quarter.

Its story is consistent:

Mid-single-digit organic growth

High-margin bolt-ons

Smart reinvestment into product development and analytics

It wins by embedding itself into industries too complex for newcomers to disrupt.

RELX isn’t flashy. It’s foundational.

If you’re looking for the next AI darling or retail rocket ship, this isn’t it.

But if you want:

Strong pricing power

Resilience through cycles

Quiet dominance in regulated, information-heavy industries

RELX might be one of the most overlooked compounders on the market.

It’s not just data.

It’s indispensable.

2. Lifco AB (Ticker: $LFABF)

Buy Weird. Hold Forever.

Lifco doesn’t chase megatrends.

It buys profitable, often obscure businesses, and lets them run.

Where others seek scale, Lifco seeks resilience through randomness.

To the outside world, it may look scattered.

But under the surface, this is controlled, cash-generating chaos.

A collection of niches. A discipline of steel.

Lifco has quietly acquired over 200 businesses.

Each one is small, specialized, and vital in its own corner of the world.

Dental supplies? Check.

Demolition robots? Check.

Funeral equipment? Also check.

If it’s profitable, boring, and overlooked, Lifco is interested.

This isn’t spray-and-pray.

It’s sniper-style M&A.

Decentralization is the rule, not the goal.

Once acquired, Lifco doesn’t integrate.

It delegates.

Every business:

Keeps its management

Controls its own destiny

Reports lean metrics and tight cash flow

HQ doesn’t micromanage—it empowers.

Because the people who built the company are still the best ones to run it.

Margins from the mundane.

Lifco thrives on businesses that:

Don’t need reinvention

Serve stable, recurring demand

Can raise prices without losing customers

That’s how they consistently deliver:

High operating margins

Strong ROIC

Minimal capex needs

No moonshots. No dilution. Just steady compounding.

Acquisition strategy: small, smart, constant.

Lifco’s M&A engine runs year-round:

Dozens of bolt-ons per year

Disciplined pricing (often below 8x EBIT)

Focus on cash conversion and return on equity

While others hunt unicorns, Lifco collects cash cows.

It’s not about growing fast.

It’s about never slowing down.

Optionality through obscurity.

Every new acquisition adds:

Industry insight

Local moats

Revenue diversity

And the more eclectic the portfolio gets, the more anti-fragile the whole system becomes.

Volatility in one corner? Irrelevant to the rest.

It’s optionality disguised as clutter.

Lifco isn’t a household name. And that’s the point.

It doesn’t advertise.

It doesn’t dazzle investors.

It just buys smart, holds forever, and reinvests profits with ruthless efficiency.

If you want:

Exposure to niche markets

Serial acquisition mastery

A decentralized compounding machine with Scandinavian restraint

Lifco might be one of the most underappreciated public companies in Europe.

Weird portfolio. Wonderful results.

1. Teqnion AB (Ticker: $TEQ)

Small Cap. Big Philosophy.

Teqnion doesn’t look like much on the surface.

A scattered portfolio.

A low-key founder.

A market cap you could miss in a blink.

But beneath the quiet exterior lies a compounder engineered for the long haul—

Fueled by culture, cash flow, and careful acquisitions.

Not tech. Not trendy. Just tenacious.

Teqnion isn’t building platforms.

It’s collecting niche, profitable industrial businesses that quietly dominate their markets.

From power tools to ventilation systems to specialized testing equipment—

If it’s overlooked, cash-generative, and founder-led, Teqnion wants it.

It doesn’t chase hype.

It buys moats so narrow that nobody else notices them.

Decentralization with trust baked in.

Acquired companies stay local.

Stay independent.

Stay lean.

There’s no integration playbook.

Just one mandate: keep doing what made you great.

HQ supports when needed—but never smothers.

Because Teqnion believes alignment beats control.

Acquisitions are slow, careful, personal.

The team doesn’t use bankers.

They build relationships.

They look for founders ready to hand off their life’s work to a steward—not a spreadsheet.

Price discipline is non-negotiable

Fit matters more than flash

Long-term cash flow over short-term revenue boosts

It’s not a race to scale.

It’s a craft.

Margins matter. Cash is king.

Teqnion’s businesses don’t burn capital—they print it.

Low capex requirements

Strong free cash flow conversion

High returns on invested capital

Each bolt-on adds to the flywheel without creating drag.

That’s how you compound quietly.

Optionality in simplicity.

Every new business deepens the moat:

More cross-industry knowledge

More operational freedom

More cash to deploy—carefully

Teqnion isn’t optimizing for today.

It’s building a holding company that could last decades.

This is patient capital. With a pulse.

Teqnion isn’t trying to impress Wall Street.

There are no splashy presentations.

No "synergy" stories.

No moonshots.

Just:

Owner-operators building real businesses

Capital allocators focused on cash, not noise

A founder who thinks in decades, not quarters

If you want shiny, this isn’t it.

If you want sustainable, sticky, and small-but-mighty—it just might be.

Teqnion is still early in its journey.

But if you believe that discipline beats drama—and cash beats pitch decks—

This little Swedish acquirer might be one of the most promising compounders you’ve never heard of.

Buy boring. Build quietly. Compound forever.

🔥 Ready to go from reading about great businesses to owning them with conviction?

You’ve just read 7 of the world’s most underrated compounders.

Now imagine what you could do with the full toolkit:

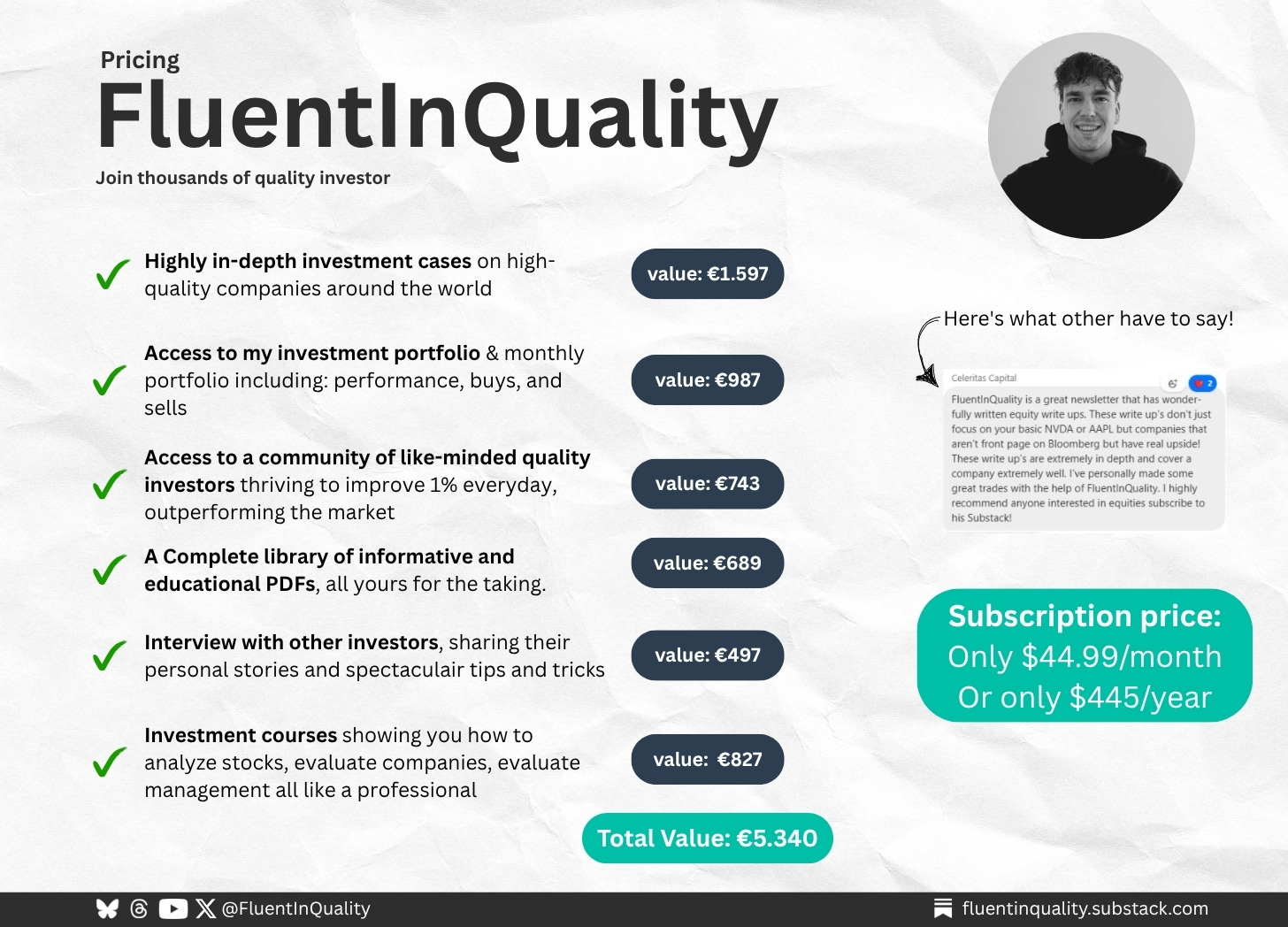

🔍 Full research reports and deep dives worth €1,597

📊 My monthly buy/sell portfolio updates (€987)

🧠 Private Slack group of high-conviction investors (€743)

🗂️ Downloadable tools, investor interviews & PDF briefs (€2,013)

Total value: €5,340 — yours for €44.99/month or €445/year.

This isn’t just insight. It’s an edge.

Delivered weekly. Backed by work. Trusted by 1,200+ investors.

🟢 Become one of The Fluent Few.

Let’s build wealth the right way — brick by brick

And that is it for today!

P.S.… if you’re enjoying FluentInQuality, could you take 3 seconds to refer this edition to a friend? It goes a long way in helping me grow the newsletter (and bring more Fluenteers into the world).

Great investments don’t shout—they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.

Nice list.

$CRM - Salesforce, should at least deserve honorable mention.