The Art of Evaluating Management: A Masterclass for Long-Term Investors

Welcome back, Fluenteers! 👋🏻

Great businesses don’t run themselves.

Behind every enduring company lies a management team that shapes its trajectory, allocates its resources, and defines its culture. For long-term investors, evaluating management is not a peripheral exercise, it’s the cornerstone of intelligent capital allocation. A mediocre team can squander a great business; an exceptional team can transform a good one into a legend. This article serves as a definitive guide to analyzing the management of publicly listed companies, blending timeless wisdom, practical tools, and real-world examples to empower investors to make informed decisions.

Let’s go over everything you need to know so you can analyze every CEO globally.

Happy compounding!

Why Management Matters

“When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

— Warren Buffett

Investing is about buying pieces of businesses, and people run businesses. The quality of those people, executives, board members, and key decision-makers, determines whether your capital compounds or erodes. As Charlie Munger once said, “Good management can make a good business great, but bad management can destroy even the best.” Management is the steward of your investment, entrusted with navigating competitive landscapes, economic cycles, and unforeseen challenges.

Consider the stakes: a company with a dominant market position can falter under poor leadership (consider General Electric under Jeffrey Immelt), while a well-managed firm can defy industry headwinds (as seen with Constellation Software under Mark Leonard). Management’s decisions on capital allocation, strategy, and culture compound over time, much like your returns. Ignoring this factor is like buying a ship without inspecting the captain.

Philip Fisher, in Common Stocks and Uncommon Profits, emphasized that management is the “single most important factor” in assessing a company’s long-term potential. His 15-point framework for evaluating businesses dedicates significant weight to the people at the helm. Why? Because management is the bridge between a company’s present and its future. For long-term investors, understanding this bridge is non-negotiable.

Core Pillars of Great Management

Exceptional management rests on six pillars. These are the qualities that separate the stewards of wealth creation from the destroyers of value.

1. Capital Allocation

Capital allocation is the CEO’s primary job. As William Thorndike details in The Outsiders, great CEOs are not just operators but master allocators, deploying cash flows to maximize long-term value. They decide whether to reinvest in the business, pay dividends, buy back shares, reduce debt, or make acquisitions. Poor allocators chase growth for growth’s sake; great ones prioritize return on invested capital (ROIC).

Example: Warren Buffett at Berkshire Hathaway. Buffett’s genius lies in his disciplined allocation, buying high-return businesses, avoiding overpriced acquisitions, and holding cash when opportunities are scarce. Contrast this with companies that overpay for acquisitions (e.g., AOL-Time Warner) or hoard cash without a purpose.

2. Transparency

Great managers communicate with clarity and candor. Their shareholder letters, earnings calls, and public statements reveal not just what they’re doing but how they think. Transparency builds trust and signals intellectual honesty. As Nick Sleep, the legendary investor, noted, “The best managements are those who tell you the truth, even when it’s uncomfortable.”

Example: Satya Nadella’s shareholder letters at Microsoft are models of clarity, outlining strategy, risks, and progress without jargon or obfuscation.

3. Long-Term Thinking

Exceptional managers prioritize the next decade over the next quarter. They resist Wall Street’s pressure to chase short-term earnings at the expense of sustainable growth. In Quality Investing, authors Lawrence Cunningham and Torkell Eide argue that long-term thinkers build “durable” businesses that compound value over time.

Example: Mark Leonard of Constellation Software, who avoids short-term metrics like EPS growth in favor of acquiring cash-generative businesses for the long haul.

4. Alignment of Incentives

Managers should eat their own cooking. Insider ownership, where executives hold meaningful equity, ensures their interests align with shareholders’. Conversely, excessive stock-based compensation or short-term bonuses can incentivize reckless behavior. As Buffett says, “I’d rather have a manager who’s slightly underpaid and owns stock than one who’s overpaid and doesn’t.”

5. Culture-Building

A strong culture attracts talent, drives execution, and sustains competitive advantage. In The Art of Execution, Lee Freeman-Shor highlights how great managers foster environments where employees are empowered to innovate and take calculated risks. Culture is intangible, yet it can be measured through employee retention, innovation output, and customer satisfaction.

Example: Costco’s Jim Sinegal built a culture of frugality and customer focus, reflected in low employee turnover and industry-leading margins.

6. Adaptability

Markets evolve, technologies disrupt, and economies shift. Great managers adapt without losing sight of their core principles. They balance conviction with flexibility, as Fisher noted in his 15-point framework: “Does the management have a determination to continue to develop products or processes that will still further increase total sales potentials when the growth potentials of currently attractive product lines have largely been exploited?”

Example: Nadella’s pivot of Microsoft toward cloud computing (Azure) transformed the company into a growth machine.

Qualitative & Quantitative Indicators

Evaluating management requires blending qualitative insights with quantitative metrics. Here’s how to assess each pillar.

Qualitative Indicators

Shareholder Letters: Read annual letters for clarity, candor, and strategic insight. Compare Buffett’s Berkshire letters (decades of wisdom) with vague, promotional ones from failing companies.

Earnings Calls: Listen to how management addresses tough questions. Do they deflect or engage? Are they overly optimistic or grounded?

Track Record: Study the CEO’s history. Have they built value elsewhere, or do they continually fail? Look at their tenure and consistency.

Industry Reputation: What do competitors, employees, or customers say? Glassdoor reviews, industry reports, and news can reveal patterns.

Quantitative Indicators

Insider Ownership: High ownership (e.g., 5%+ of shares) signals alignment. Check SEC filings (Form 4) for insider buying/selling trends.

Compensation Structure: Scrutinize proxy statements (DEF 14A). Are bonuses tied to long-term metrics like ROIC or short-term EPS? Excessive stock grants or golden parachutes are red flags.

Capital Efficiency: Measure ROIC over time. Compare it to peers. A high ROIC with consistent reinvestment suggests a disciplined allocation.

Buybacks vs. Dilution: Are buybacks done at attractive valuations? Excessive share issuance dilutes shareholders and signals poor capital discipline.

Operational Metrics: Examine revenue growth, margin stability, and trends in free cash flow. These reflect management’s ability to execute.

Red Flags & Pitfalls

Poor management leaves clues. Here are warning signs to watch for:

Promotional Behavior: Overhyping results, making bold promises, or focusing on stock price over business fundamentals. Think Enron’s Jeff Skilling or Theranos’ Elizabeth Holmes.

Short-Termism: Cutting R&D or maintenance capex to hit quarterly targets. This erodes long-term value.

Misaligned Incentives: High cash bonuses or stock grants unrelated to performance. Check if executives sell shares immediately after vesting.

Opaque Communication: Vague shareholder letters, evasive earnings calls, or refusal to address risks.

Frequent Turnover: High executive or board turnover often signals instability or a poor organizational culture.

Overleveraged Balance Sheets: Excessive debt to fund acquisitions or buybacks, often to mask weak operations.

Related-Party Transactions: Deals with insiders or affiliates (e.g., family members) raise concerns about conflicts of interest.

Case Studies: Excellence vs. Failure

Exceptional Management

Warren Buffett (Berkshire Hathaway): Buffett’s capital allocation is legendary, buying undervalued businesses, holding cash when needed, and avoiding dilution. His shareholder letters are masterclasses in transparency, blending humor, candor, and insight. Berkshire’s 50-year CAGR of 20% speaks for itself.

Mark Leonard (Constellation Software): Leonard focuses on acquiring niche software businesses with high ROIC, avoiding Wall Street’s obsession with growth metrics. His shareholder letters are sparse but brutally honest, emphasizing long-term value over short-term noise.

Satya Nadella (Microsoft): Nadella transformed Microsoft by shifting to cloud computing and subscriptions, boosting the market cap from $300 billion to over $2 trillion. His culture-building, emphasizing collaboration and innovation, reinvigorated a stagnant giant.

Destructive Management

Adam Neumann (WeWork): Neumann’s charisma masked reckless spending, self-dealing (e.g., leasing properties he owned to WeWork), and a lack of focus on profitability. His exit cost investors billions.

Elizabeth Holmes (Theranos): Holmes’ fraudulent claims and lack of transparency destroyed a $9 billion valuation. Her refusal to engage with scrutiny was a glaring red flag.

Jeffrey Immelt (General Electric): Immelt’s overpriced acquisitions (e.g., Alstom) and focus on financial engineering over core operations led to GE’s decline from a $500 billion giant to a struggling conglomerate.

Wisdom from the Greats

Charlie Munger: “The best way to judge a manager is to look at their record and talk to people who’ve worked with them. Numbers alone don’t tell the story.”

Nick Sleep: “We look for managers who think like owners, not hired hands. They should be obsessed with the business, not their stock options.”

Tom Gayner (Markel): “I want to invest with people who wake up every day thinking about how to make the company better, not richer.”

Philip Fisher (Common Stocks and Uncommon Profits): “Does the management talk freely to investors about its affairs when things are going well, but clam up when troubles or disappointments arise?”

William Thorndike (The Outsiders): “The best CEOs are not the flashiest, they’re the ones who quietly compound value through disciplined capital allocation.”

The Investor’s Checklist for Analyzing Management

Use this checklist to evaluate management systematically. Apply it to every company you consider.

Capital Allocation: Does management prioritize high-ROIC investments? Are acquisitions disciplined or empire-building?

Transparency: Are shareholder letters and earnings calls clear, candid, and strategic? Do they address risks head-on?

Long-Term Focus: Does management prioritize sustainable growth over quarterly EPS? Are they willing to sacrifice short-term results for long-term gains?

Alignment: Do executives own significant equity? Are compensation structures tied to long-term performance?

Culture: Does the company attract and retain talent? Are employees empowered to innovate?

Adaptability: Has management navigated industry changes successfully? Do they balance conviction with flexibility?

Track Record: What’s the CEO’s history? Have they created value consistently across roles or companies?

Red Flags: Are there signs of promotional behavior, short-termism, or misaligned incentives? Check insider selling, debt levels, and related-party deals.

Final Thoughts

Evaluating management is both an art and a science. It demands qualitative judgment, reading between the lines of a shareholder letter or sensing a CEO’s integrity, and quantitative rigor, from ROIC to insider ownership. The best managers are rare: they think like owners, act with discipline, and build cultures that endure. The worst destroy value through hubris, greed, or incompetence.

As a long-term investor, your job is to find the former and avoid the latter. Use the pillars, indicators, and checklist in this guide to separate the stewards from the charlatans. As Buffett reminds us, “You don’t have to swing at every pitch.” Wait for companies led by exceptional managers, and your portfolio will thank you for decades.

Ready to go from reading about great businesses to owning them with conviction?

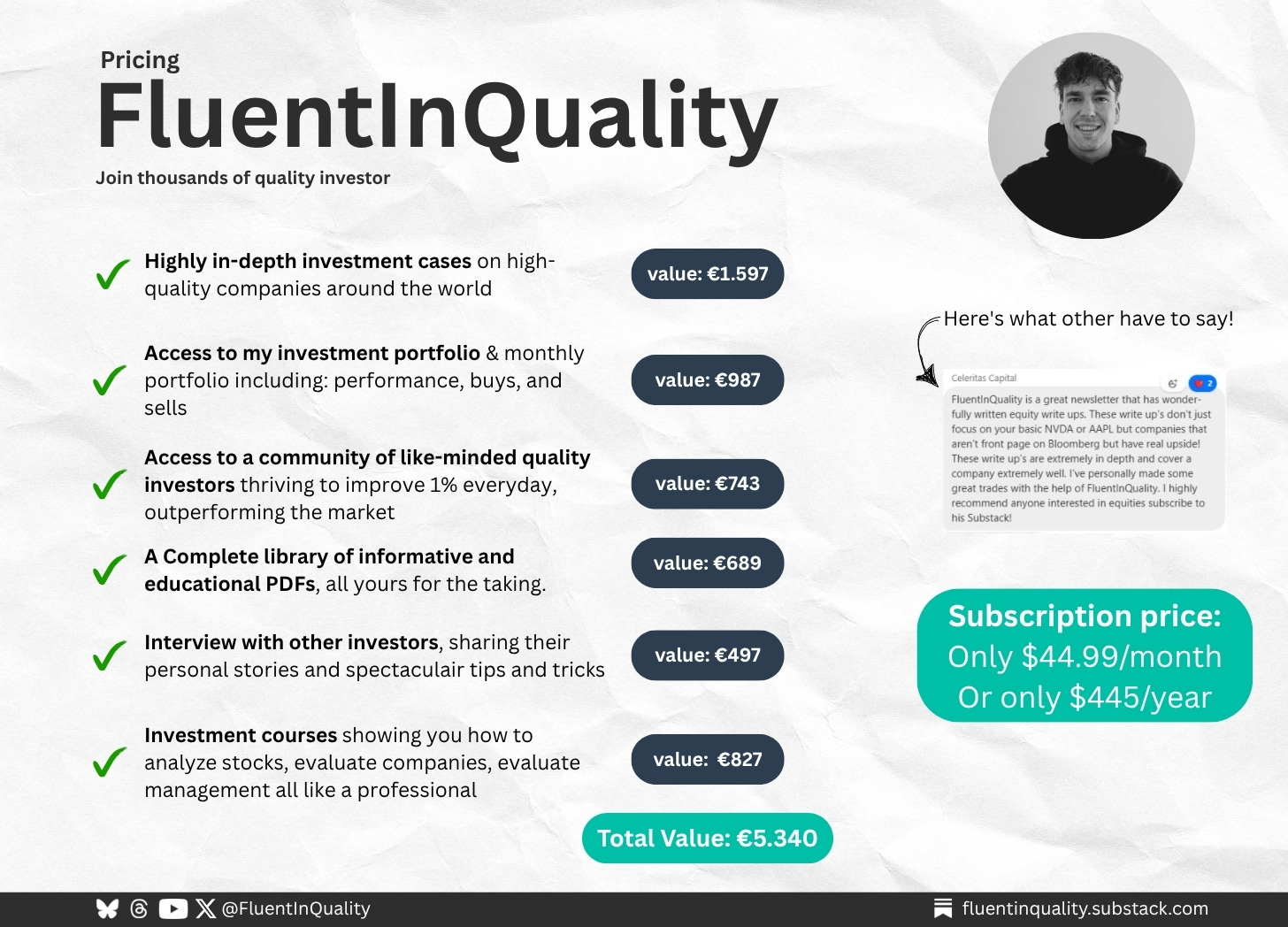

✔️ Full research reports and timeless deep dives (valued at €1,597)

✔️ Monthly buy/sell portfolio updates with commentary (€987)

✔️ Access to a private Discord of high-conviction investors (€743)

✔️ Tools, templates, investor interviews & PDF briefs (€2,013)

Total value: €5,340 — yours for just €44.99/month or €445/year.

No fluff. No noise. Just real work, trusted by 1,200+ long-term investors.

This isn’t just insight. It’s an investing advantage.

Delivered weekly. Backed by research. Built to compound.

🟢 Become one of The Fluent Few

Let’s build wealth the right way—brick by brick.

PS…. if you’re enjoying FluentInQuality, can you take 3 seconds to refer this edition to a friend? It will go a long way in helping me grow the newsletter (and bring more quality investors into the world).

Great investments don’t shout, they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.

Remember Guru, an asshole in the management can screw up the best reputed company in an Industry.