The 7 Biggest Red Flags in Companies Quality Investors Shouldn’t Ignore (And What To Look For)

Sometimes red flags are subtle, sometimes they're not. Here are seven you need to be on the lookout for!

Welcome back, Fluenteers!

There tend to be signs that require you, as a quality investor, to be extra cautious and keep them at the back of your mind.

Some signs, when viewed in isolation, do not reveal much or do not initially alarm you. But, once you group them with other red flags, you’re either better off leaving the company on the sidelines or diving even deeper to find explanations or reasoning for these red flags. You have the data; that’s your edge. You need to utilize it.

Here are 10 red flags to look out for in companies.

Red Flag #1: Consistently Negative Free Cash Flow

If a company is constantly burning cash, it signals underlying issues with profitability or capital discipline.

Free cash flow (FCF) is the money remaining after deducting operational and capital expenses. A persistently negative free cash flow (FCF) may indicate that the business isn’t self-sustaining or is chasing growth at all costs. Ultimately, this results in debt, dilution, or both.

Cash is not just king—it’s survival.

What to look for:

Multi-year negative FCF

High capex without improving returns

Regular equity raises or increasing debt

No guidance on breakeven timelines

Promises of future profits that never materialize

Red Flag #2: Frequent Management Turnover

A revolving door in the C-suite often points to deeper issues within the company.

Stable leadership is crucial for executing long-term strategies. Frequent changes disrupt vision, accountability, and company culture. It’s often a sign of boardroom conflicts or a broken business model.

Great companies rarely change captains mid-voyage.

What to look for:

CEO/CFO (management) changes every 1–2 years

Abrupt executive resignations

Interim titles lasting too long

Excessive executive severance packages

Lack of succession planning

Red Flag #3: Overly Complex Financials

When financials are hard to understand, risk is often hidden.

Complex accounting can be used to mask weakness or inflate results. Obscure segments and excessive non-GAAP metrics distort the real picture. If it smells like Enron, think twice.

If you can’t explain it, don’t invest in it.

What to look for:

Long footnotes and frequent accounting changes

Complicated segment reporting

Aggressive use of “adjusted” earnings

Delays in filing reports

Frequent restatements

Red Flag #4: Customer Concentration Risk

Too much reliance on a few customers is a dangerous game.

If one or two clients leave, it could gut the company’s revenue overnight.

This makes future cash flows highly uncertain. Even worse, dominant customers can squeeze margins and dictate terms.

Healthy businesses spread their bets.

What to look for:

A single customer generating 20%+ of revenue

Poor customer diversification in new markets

Sudden customer loss with no replacement

Dependency on the government or volatile industries

Lack of customer disclosure

Red Flag #5: Aggressive Insider Selling

If insiders don’t want to hold the stock, why should you?

While some selling is normal, consistent, large-scale dumping by insiders should raise concerns. It often signals a lack of confidence in the future or knowledge of issues not yet public. Especially bad when timed around buybacks or guidance.

Insiders may sell for many reasons, but buy for only one.

What to look for:

Multiple executives selling together

Selling after buyback or earnings hype

No recent insider buying

Sudden stock-based comp followed by cashing out

Selling ahead of major announcements

Red Flag #6: Overleveraged Balance Sheet

Too much debt turns small problems into existential crises.

High debt reduces flexibility, increases default risk, and eats into profits via interest costs. In downturns, it can force asset sales or bankruptcy.

Even good businesses can collapse if overleveraged.

Debt magnifies everything, especially mistakes.

What to look for:

Debt-to-EBITDA over 3x in cyclical businesses

Interest coverage ratio below 4x

Rising debt with falling cash flow

Refinancing dependence

Debt maturity cliffs are approaching fast

Red Flag #7: Weak or Declining (Gross) Margins

Falling margins usually indicate competitive pressure or pricing weakness.

Gross margin is a clear indicator of pricing power and cost efficiency.

Declining or low margins indicate that a company is losing control of its financial performance. It often precedes bigger earnings problems down the road.

Margin pressure is often an early warning sign.

What to look for:

Declining gross margin trend over time

Margins below industry peers

Rising cost of goods without pricing power

Lack of margin guidance

Management blames “temporary” headwinds too often

Final Thought

These red flags don’t always mean “run”—but they should always mean “dig deeper.”

Your job isn’t just to find great companies—it’s to avoid the disasters. And red flags are where that job starts.

🔥 Serious About Investing? Let’s Get to Work.

You’ve read the free stuff.

Now imagine what you could do with everything behind the paywall:

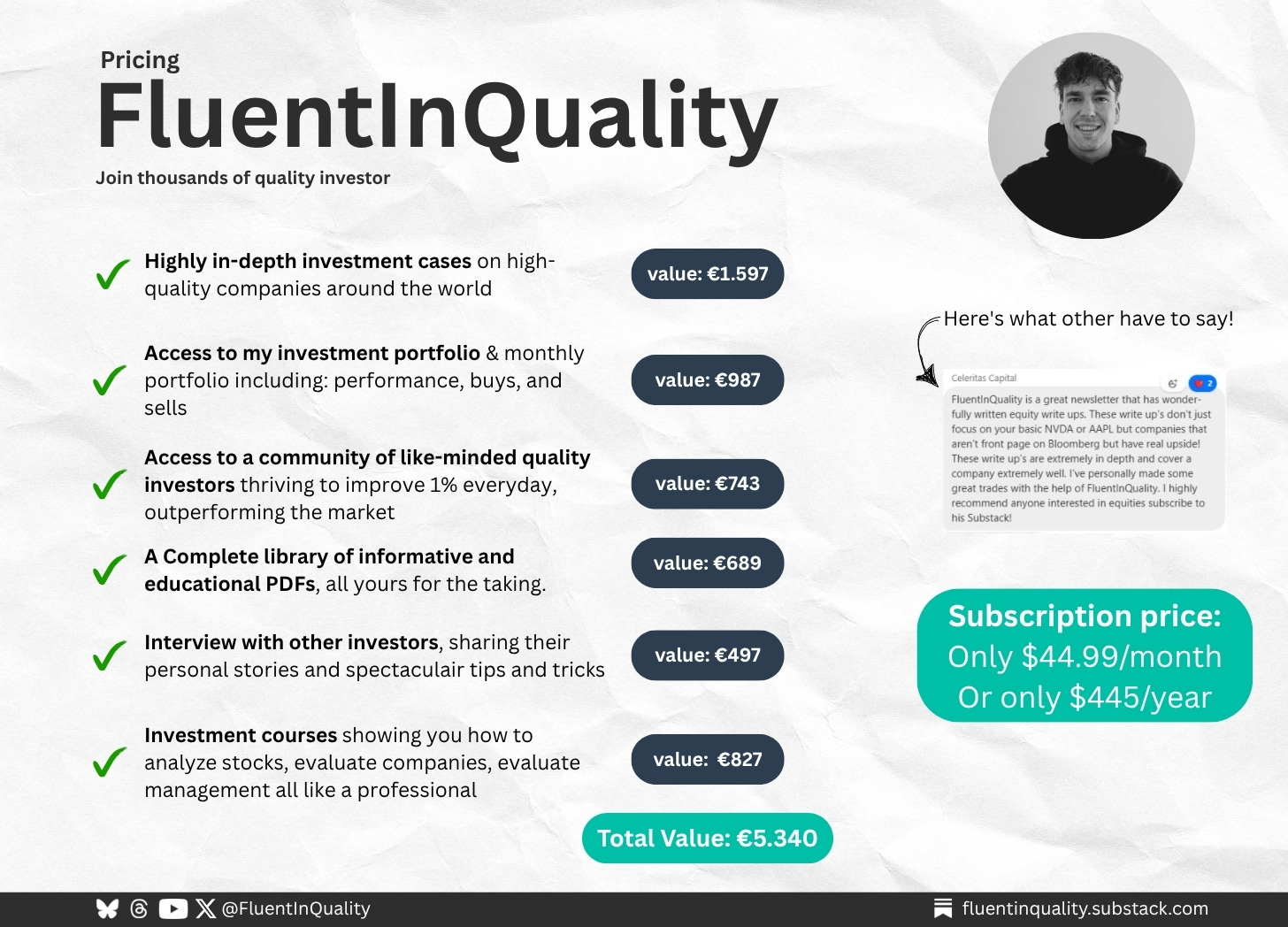

✅ In-depth investment breakdowns worth €1,597

✅ Access to my monthly portfolio: performance, buys, and sells (€987)

✅ A private community of like-minded investors (€743)

✅ Downloadable PDFs, tools, investor interviews, and more (€2,013 total)

Total value: €5,340 — Yours for just €44.99/month or €445/year.

This is not just information. It’s insight, strategy, and confidence — delivered weekly.

🟢 Join The Fluent Few and unlock your edge.

And that is it for today!

P.S.… if you’re enjoying FluentInQuality, could you take 3 seconds to refer this edition to a friend? It goes a long way in helping me grow the newsletter (and bring more Fluenteers into the world).

Great investments don’t shout—they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.

Excellent breakdown, Yorrin. The points on negative Free Cash Flow and overleveraged balance sheets are especially critical through a dividend investing lens.