SpaceX Is Going Public. Every Single Thing You Need to Know.

A complete, forensic breakdown of the SpaceX S-1/A #2 preliminary prospectus, dated June 3, 2026. Read it once, know SpaceX better than most institutional analysts.

Nobody expected this day to come.

SpaceX has been the most valuable private company in the world for years. The one everyone wanted a piece of and nobody could touch. The company that made the US the dominant force in space again, built the internet for the other half of the planet, and quietly became one of the most consequential technology businesses in human history, all without ever answering to a single public shareholder.

That changes now.

On June 3, 2026, SpaceX filed its S-1 with the SEC. The IPO price is expected to be $135 per share. The company is selling 555,555,555 shares. Net proceeds: approximately $74.4 billion, making this one of the largest public offerings ever attempted.

Most people will read a headline about this and move on. That would be a mistake.

What follows is a complete, forensic breakdown of every material detail in the 405-page preliminary prospectus. The rockets. The satellites. The AI business almost nobody is talking about. The financials. The risks. The compensation structure has Mars colonization written into the CEO’s equity vesting conditions.

This is not a hype piece. It is the document, translated into plain language, so you understand exactly what you are looking at before the market opens on IPO day.

P.S. Since it will be a hefty piece, here’s the table of contents. If you’re solely interested in a couple of things, here you can see when and where this will be discussed:

What Will Be Discussed

Before We Begin: What This Document Is

The Company in Three Sentences

Corporate History and Structure

The Three Business Segments

Part I: The Space Business

The Reusability Revolution: Historical Context

The Falcon 9: Detailed Specification

The Falcon Heavy: Detailed Specification

Dragon: The Human Spaceflight Vehicle

Starship: The Everything Vehicle

Launch Operations Data

Government Space Business

Part II: The Connectivity Business

The Origin of Starlink

The Constellation

Starlink Performance Specifications

Satellite Manufacturing

The Subscriber Business

Connectivity Segment Financial Performance

Enterprise Solutions: Named Partners

Government Solutions and Starshield

Next-Generation Satellites

Starlink Mobile: The Direct-to-Device Network

Additional Connectivity Markets

Part III: The AI Business

The xAI Acquisition: Background

AI Compute Infrastructure: COLOSSUS and COLOSSUS II

Grok: The AI Model

Grok Product Suite

The X Platform

AI Segment Financial Performance

The Orbital AI Vision

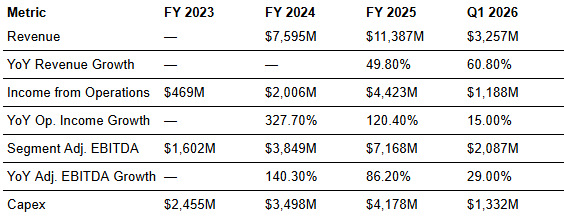

Part IV: Detailed Financials

Consolidated Income Statement

Cash Flow Statement

Capital Expenditure by Segment

Segment Summary: Space

Segment Summary: Connectivity

Segment Summary: AI

Balance Sheet

Part V: The IPO Structure

Share Count and Voting Rights

The Dual Vesting Awards

Directed Share Program

Use of Proceeds

Part VI: The Facilities Map

The Recovery Fleet

Part VII: The Market Opportunity

The $28.5 Trillion TAM Breakdown

Part VIII: Leadership, Governance, and Compensation

Management Team

Board of Directors

Compensation Philosophy

Part IX: The Competition

Part X: The Complete Risk Landscape

Part XI: The Underwriting Syndicate

Part XII: The Vision Statement

Final Data Summary

All information in this article is drawn exclusively from Space Exploration Technologies Corp.’s S-1/A #2 preliminary prospectus, dated June 3, 2026. The preliminary prospectus is subject to completion and change. Securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This article is for informational and analytical purposes only. It does not constitute investment advice, a solicitation to buy or sell any security, or an endorsement of any investment product.

Before We Begin: What This Document Is

On June 3, 2026, SpaceX quietly filed an amended registration statement with the SEC, 405 pages of dense legal and financial disclosure that most people will never read, but probably should.

The offering is straightforward on the surface: 555,555,555 shares of Class A common stock at $135.00 per share, listed under the ticker SPCX on Nasdaq. Do the math, and the primary offering alone raises roughly $74.4 billion in net proceeds, or $85.7 billion if underwriters exercise their overallotment option in full. Either number puts this among the largest IPOs ever attempted.

A few things worth noting before anyone gets too excited: this is still a preliminary filing. The SEC hasn’t declared it effective yet, the price can still move, and nothing is sold until that changes.

But the numbers are what they are. At $135 a share, Elon Musk’s rocket company is asking the public markets to write one of the biggest checks in stock market history.

SpaceX in Three Sentences

Elon Musk founded SpaceX in 2002 with one stated goal: to make humanity a multiplanetary species. That mission isn’t just marketing copy, it’s written into the company’s founding documents and baked into how employees get paid.

Twenty-four years later, SpaceX has become something far broader than a rocket company. It operates the most capable rocket fleet in the world, runs the largest satellite internet constellation ever built, and, following its acquisition of xAI and X in February 2026, now controls a major AI platform and social media network too.

At this point, “aerospace company” barely covers it.

Corporate History and Structure

SpaceX was incorporated as Space Exploration Technologies Corp. in Delaware on March 14, 2002, and reincorporated as a Texas corporation on February 14, 2024. Its principal executive offices are at 1 Rocket Road, Starbase, Texas 78521, situated in the newly created city of Starbase in Cameron County, Texas, on the Gulf of America.

The consolidated financial statements include the historical results of two transactions between entities under common control: X Holdings Corp. was acquired by X.AI Holdings Corp. (xAI), effective March 28, 2025. xAI was then acquired by SpaceX, effective February 2, 2026 (the “xAI Merger”). Because these were common-control transactions, Elon Musk controlled all entities, and accounting rules require the combined financial statements to be presented retrospectively for all periods, as if the companies had always been together. Every financial comparison in this document reflects the combined SpaceX + xAI + X entity.

A five-for-one stock split was effected on May 4, 2026. All share and per-share data in the filing is post-split.

The Three Business Segments

SpaceX operates as three distinct but interdependent segments:

Segment 1: Space -> Customer launch operations and spacecraft services, including Falcon 9, Falcon Heavy, Dragon, and Starship.

Segment 2: Connectivity -> The Starlink global broadband satellite internet service, enterprise solutions, government solutions, Starlink Mobile, and Starshield.

Segment 3: AI -> xAI’s artificial intelligence platform (Grok models, COLOSSUS/COLOSSUS II data centers), the X social media platform, and consumer/enterprise AI products.

The prospectus is emphatic that all three are interdependent: Space enables Connectivity and AI through launch cost and cadence; Connectivity generates the cash that funds Space and AI investment; AI, via orbital compute, is the long-term amplifier of the entire system.

Part I: The Space Business

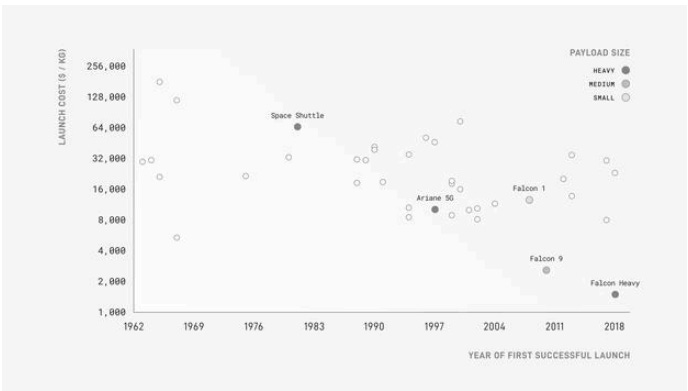

The Reusability Revolution: Historical Context

For decades, getting to space was expensive by design. Government cost-plus contracts gave launch providers no reason to cut costs, overruns were billable, efficiency was unrewarded, and the industry settled into a comfortable rhythm of 25 to 35 missions per year globally at roughly $18,500 per kilogram to Low-Earth Orbit. Nobody was particularly motivated to change that.

SpaceX’s founding insight was almost embarrassingly simple in hindsight: the reason launches cost so much was that you threw the rocket away every time. Fix that one thing, land the booster, refurbish it, fly it again, and the entire economics of space access falls apart in the best possible way.

Turning that insight into reality took thirteen years. Then, on December 21, 2015, a Falcon 9 first-stage booster lifted off from Cape Canaveral, reached space, and came back down to land upright. Four months later, SpaceX did it on a drone ship floating in the Atlantic. By 2017, booster recovery wasn’t a milestone anymore, it was just how SpaceX operated.

What happened to launch economics after that:

The numbers tell the story more clearly than any narrative could.

When the first Falcon 9 flew in 2010, NASA pegged the launch cost at roughly $2,700 per kilogram to Low-Earth Orbit, about 85% below the historical average. Falcon Heavy, which debuted in 2018, pushed that down to approximately $1,400 per kilogram. A 92% reduction from where the industry started. And if full Starship reusability works as projected, SpaceX expects to cross 99%.

That’s not incremental progress. That’s a different industry.

The downstream effects showed up fast. In 2015, fewer than 1,000 active maneuverable satellites orbited Earth. By March 2026, that number had grown to approximately 12,700. Global payload launched to orbit went from roughly 220 metric tons in 2012 to approximately 2,600 metric tons in 2025, a twelvefold increase in thirteen years. SpaceX launched more than 80% of it.

The Falcon 9: Detailed Specification

Falcon 9 made its first flight on June 4, 2010, and has since become the most flown orbital rocket in history.

The architecture is straightforward: two stages, burning liquid oxygen and RP-1 kerosene. The first stage runs nine Merlin 1D engines producing over 1.7 million pounds of thrust at sea level. The second stage runs a single vacuum-optimized Merlin. Fully expendable, it can push roughly 23 metric tons to Low-Earth Orbit or about 8 metric tons to Geostationary Transfer Orbit.

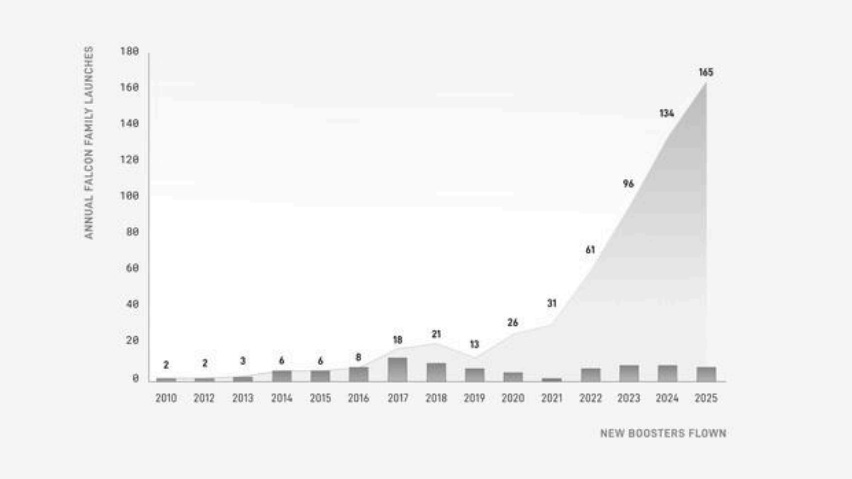

What those specs don’t capture is the operational record behind them. Through March 31, 2026, Falcon 9 has completed approximately 620 orbital launches at a mission success rate above 99%. One booster has flown and landed 34 times. In 2025 alone, SpaceX flew 165 Falcon 9 missions, which accounted for more than half of every orbital launch attempted anywhere on Earth that year.

To put that last number in context: one rocket, built by one company, carried more payload to orbit in a single year than the rest of the world’s launch industry combined.

Key Falcon 9 firsts, from the prospectus:

First orbital-class reusable booster landing (December 2015)

First autonomous drone ship landing (April 2016)

First booster to fly 34 times (as of March 31, 2026)

Over 570 successful booster landings to date

Only NASA-certified U.S. vehicle for crewed ISS missions

19 successful human spaceflight missions with 100% mission success rate

Engines designed and manufactured entirely in-house (Merlin family)

The Merlin engine sits among the highest thrust-to-weight ratio rocket engines in operational service today, and SpaceX builds every part of it in-house. Design, manufacturing, qualification, testing: all of it happens at SpaceX’s own facilities in Hawthorne, California, and McGregor, Texas.

At this stage in its life, Falcon 9 is less a development program than a cash machine. As SpaceX shifts its primary engineering resources toward Starship, Falcon 9 keeps flying, keeps landing, and keeps generating high-margin recurring revenue with a fleet that is largely already paid for.

One accounting detail worth understanding: SpaceX qualifies its boosters for up to 40 flights, but depreciates them over a maximum of 25. The gap reflects two practical realities. First, Starship is coming, and when it arrives at scale, Falcon 9 demand will fall. Second, certain government contracts prohibit flying boosters with more than five prior flights on their missions, which limits how fully any given booster can be utilized across its certified life.

In other words, the boosters may be capable of more than the books give them credit for.

Falcon Heavy notable missions: Arabsat-6A, STP-2 (U.S. Air Force), AFSPC-44, ViaSat-3 Americas, Jupiter-3, Psyche (NASA asteroid probe), Europa Clipper (NASA Jupiter moon probe), Dragonfly (NASA Saturn probe, upcoming), and the upcoming Nancy Grace Roman telescope. Falcon Heavy was certified for NSSL missions in 2019.

Dragon: The Human Spaceflight Vehicle

Dragon comes in two versions, and between them they’ve redefined what commercial spaceflight looks like.

Dragon Cargo handles uncrewed resupply to the International Space Station, carrying up to 6,000 kilograms on the way up and returning up to 3,000 kilograms on the way down. That return capability matters more than it might sound: Dragon is the only spacecraft in operation that can bring significant cargo mass back from the ISS to Earth. It docks autonomously using NASA’s International Docking System Standard, has completed over 30 cargo missions to the station, and gets reused across multiple flights after refurbishment. SpaceX first demonstrated this in 2012, becoming the first commercial spacecraft to deliver and return cargo from the ISS.

Dragon Crew carries people. Up to seven of them, for missions lasting as long as nine months, docked to the station. It runs 16 Draco thrusters for orbital maneuvering, plus 8 Super Draco engines that can pull the capsule away from a failing rocket within milliseconds, at any point during ascent. On May 30, 2020, Dragon Crew became the first private vehicle to carry astronauts to orbit, launching NASA’s Bob Behnken and Doug Hurley on the Demo-2 mission. Since then, it has flown 78 crewmembers from 20 countries across roughly 15 successful missions, pioneered the first polar-orbit human spaceflight, enabled the first all-commercial astronaut crew, and supported the first commercial spacewalk.

Dragon is currently the only U.S. vehicle NASA has certified under its Commercial Crew Program to transport astronauts to and from the ISS.

Starship: The Everything Vehicle

Starship is what everything else has been building toward.

The first flight test launched on April 20, 2023. SpaceX has since completed 12 test flights, with the 12th in May 2026. First payload delivery to orbit is expected in the second half of 2026.

The vehicle is two stages, both designed to be caught and reflown.

Super Heavy, the first stage, runs 33 Raptor engines in its current V3 configuration. After separation, it doesn’t land on its legs. It returns to the launch site and gets caught mid-air by mechanical arms on the launch tower, what SpaceX calls the “chopstick” system. It is one of the stranger things to watch work correctly.

Starship, the upper stage, runs six Raptors: three optimized for sea level, three for vacuum. It reenters the atmosphere protected by heat tiles, executes a propulsive landing burn, and gets caught by the same arm system. Its payload bay has a volume that rivals the pressurized sections of the International Space Station. In the V3 fully reusable configuration, it can carry 100 metric tons to Earth orbit. Future versions are projected to reach 200.

The engine underneath all of this is the Raptor, and it is not a modest upgrade over what came before. Each Raptor produces nearly triple the thrust of a Merlin engine, with higher efficiency and better performance on heavy-lift profiles. Raptor 3 cuts nearly a full ton of vehicle mass versus prior generations by simplifying the plumbing and removing heat shields. The full-flow staged combustion cycle it runs is the most propellant-efficient rocket engine architecture currently in production.

Starship Flight Test Milestones (from the prospectus):

Multiple successful integrated flight tests with complete vehicle ascent

First catch of Super Heavy booster using “chopstick” arms on the same tower it launched from

Upper stage return within three meters of the intended landing point

Transfer of approximately five metric tons of cryogenic propellant between tanks in space, the first such in-space cryogenic transfer, directly enabling future orbital refueling and lunar/Mars missions

Successful in-space relights of Raptor engines

Multiple controlled atmospheric reentries

12th flight test in May 2026: Debuted next-generation Starship vehicle and Super Heavy booster with the next evolution of Raptor engine, launching from a newly designed pad

Why Starship Changes Everything: SpaceX designed Starship from the ground up to be the world’s first fully and rapidly reusable launch vehicle. The business logic is almost absurdly simple: a rocket that can be turned around the same day it lands, flying hundreds of times per year, carrying 100+ metric tons per flight, would make almost any conceivable space mission economically viable.

A single Starship launch is designed to deploy up to 60 V3 Starlink satellites, representing a twenty-fold increase in broadband downlink capacity deployed per launch compared to a Falcon 9 launch. For orbital AI compute, Starship is the only path: deployment of 100 gigawatts per year via satellites carrying over 100 kilowatts of compute per metric ton would require transporting approximately one million metric tons to orbit annually, a scale achievable only with full Starship reusability at massive cadence.

Starship Infrastructure: Achieving the targeted Starship launch cadence will require:

Securing additional land and developing high-rate launch sites across multiple locations

Scaling production at Starfactory (Starbase’s mass production facility designed with 24-cell Gigabay integration for vehicles up to 85 meters tall)

Constructing propellant production facilities: air separation units and methane liquefaction plants co-located with launch sites

Securing a sufficient power supply

FAA approvals to support high-cadence operations while addressing public safety and environmental review

SpaceX is expanding Florida operations for Starship: a new pad at LC-39A expected by the end of 2026, plus Space Launch Complex 37 on Cape Canaveral Space Force Station with two orbital launch pads and two towers. Total: four operational Starship launch pads by the end of 2027.

Orbital refueling, required for lunar and interplanetary missions beyond LEO, has not yet been demonstrated at full scale. The cryogenic propellant transfer test conducted in-orbit marks early progress, but full orbital refueling remains a development milestone. Importantly, full upper-stage reusability and orbital refueling are not required for V3 satellite deployment or early orbital AI compute. They are required for lunar and Mars missions.

Launch Operations Data

In 2025 alone:

165 Falcon 9 launches, 157 of which used flight-proven boosters

159 flight-proven booster launches total

2,200+ metric tons delivered to orbit

11 of 12 NSSL medium and heavy-lift missions

All 5 U.S. crew and cargo missions to the ISS

SpaceX now operates a fleet of 24 flight-proven, reusable rockets, a number that grows constantly as new cores are qualified.

Government Space Business

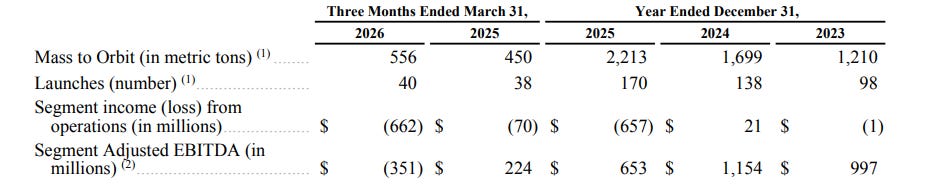

About one-fifth of SpaceX’s 2025 revenue came from U.S. federal government agencies, and the structure of those contracts is worth understanding. Every government launch contract SpaceX holds is a firm fixed-price with milestone-based payments. That means SpaceX bears all cost overrun risk. It also means SpaceX keeps every dollar of cost savings it engineers. For a company that has spent two decades driving launch costs down, that’s a structural advantage, not just a contractual detail.

The government market it’s operating in is large and getting larger. U.S. government space spending, excluding classified programs, totaled approximately $77 billion in 2024 according to the Space Foundation. SpaceX’s NSSL Phase 3 Lane 2 contracts alone run to approximately $13.7 billion through 2032, covering roughly 54 missions. The overall Phase 3 manifest has nearly doubled the mission count from Phase 2, growing to 84 missions total.

Customers include NASA, the Department of Defense, the General Services Administration, and certain Intelligence Community agencies. SpaceX is almost always the prime contractor on these engagements and rarely brings in subcontractors, which keeps margin in-house and operational control where SpaceX wants it.

Notable government programs:

NASA Commercial Crew Program: Crewed Dragon missions to ISS (exclusive U.S. launch provider)

NASA Commercial Resupply Services: Dragon cargo missions to ISS

NSSL (National Security Space Launch): Heavy and medium lift national security payloads

NASA Artemis Human Landing System: Starship is the designated lunar lander for NASA’s Artemis program to return Americans to the Moon

Starshield: Classified national security satellite network (described separately under Connectivity)

Part II: The Connectivity Business

The Origin of Starlink

Once SpaceX cracked booster reusability, it found itself sitting on an asset no one else had: the ability to launch enormous volumes of hardware to orbit at costs that made competitors’ business models look broken by comparison. The question was what to do with it.

The idea of a large-scale satellite internet constellation wasn’t new. Companies had been proposing versions of it since the 1990s. None of them worked, not because the concept was wrong, but because the economics of getting thousands of satellites into orbit were impossible to make add up. Launch cost killed every serious attempt before it got started.

SpaceX’s reusability advantage changed the arithmetic completely. By placing thousands of small satellites in Low-Earth Orbit rather than a handful of expensive ones in Geostationary Orbit, Starlink could deliver broadband internet with latency in the tens of milliseconds, roughly comparable to terrestrial fiber, to anywhere on Earth. The satellites went up starting in 2019. Customers came online in 2020.

What had been economically impossible for thirty years became a shipping product in roughly eighteen months.

The Constellation

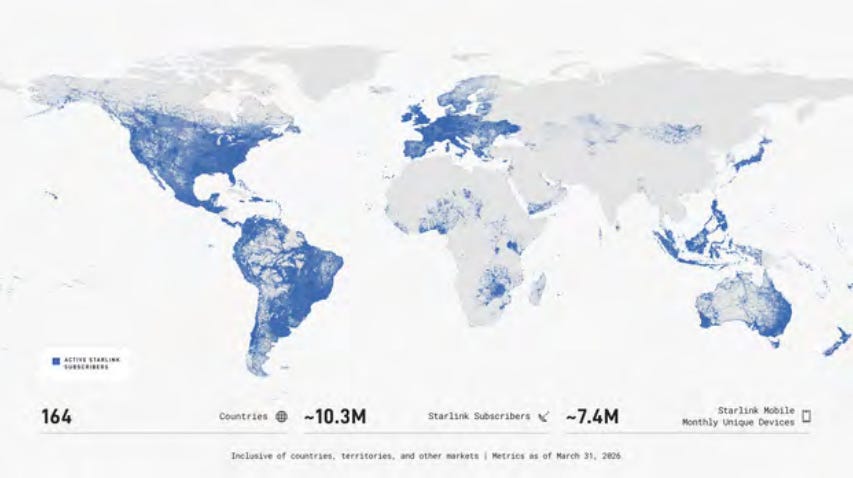

As of March 31, 2026:

~9,600 Starlink broadband and mobile satellites in Low-Earth Orbit

SpaceX owns approximately 75% of all active maneuverable satellites in orbit globally

Over 23,000 inter-satellite lasers are creating a dynamic mesh network in space

3,100 new satellites were launched in 2025 alone, approximately five times more than the total number of satellites in the entire second-largest LEO constellation

Over 400 ground station sites globally

The inter-satellite laser mesh network is a key differentiator: data can route entirely through orbit without touching terrestrial backhaul infrastructure. This enables global, ultra-low-latency routing and reduces dependence on ground infrastructure.

Satellites execute over 1,000 automated collision avoidance maneuvers per day guided by SpaceX’s autonomous system. To date, no failures of the autonomous collision avoidance system have resulted in satellite loss.

Starlink Performance Specifications

The performance numbers are worth sitting with for a moment. Starlink delivers peak residential download speeds exceeding 400 Mbps, with median speeds during peak hours around 225 Mbps as of March 2026. Round-trip latency runs as low as 21 milliseconds. On commercial aviation, passengers are getting download speeds above 400 Mbps with the same sub-25ms latency, on a plane, while legacy GEO satellite systems are still delivering low single-digit Mbps speeds with 500-plus millisecond lag. The gap isn’t closed.

The physics behind that gap is straightforward. Every Starlink satellite orbits at roughly 550 kilometers above Earth. GEO satellites sit at 35,786 kilometers. Light travels fast, but distance still adds latency, and 65 times the altitude means 65 times the round-trip signal delay at minimum. SpaceX describes Starlink as the only low-latency network available globally, and on current evidence, that’s a defensible claim. Coverage extends to every point on Earth’s surface, including the poles.

Behind the coverage sits a manufacturing operation that has quietly become one of the more remarkable industrial stories in the sector. SpaceX’s Redmond, Washington, facility was producing an average of roughly 70 satellites per week through early 2026, roughly 3,640 per year at full rate. Its Bastrop, Texas facility, which opened in 2023, produces tens of thousands of Starlink kits per day and is set to more than double in size during 2026, adding production of gateway antennas, solar cells, and AI compute satellites.

Vertical integration has done to manufacturing costs what reusability did to launch costs. Since 2022, the average cost to manufacture a Starlink Kit has fallen roughly 59%. Satellite manufacturing cost per gigabit of downlink capacity dropped approximately threefold from V1 to V2 Mini. From V1 to V3, SpaceX expects a total cost reduction of around nine times.

The pattern is consistent enough at this point that it’s probably worth taking seriously as a strategy, not just a result.

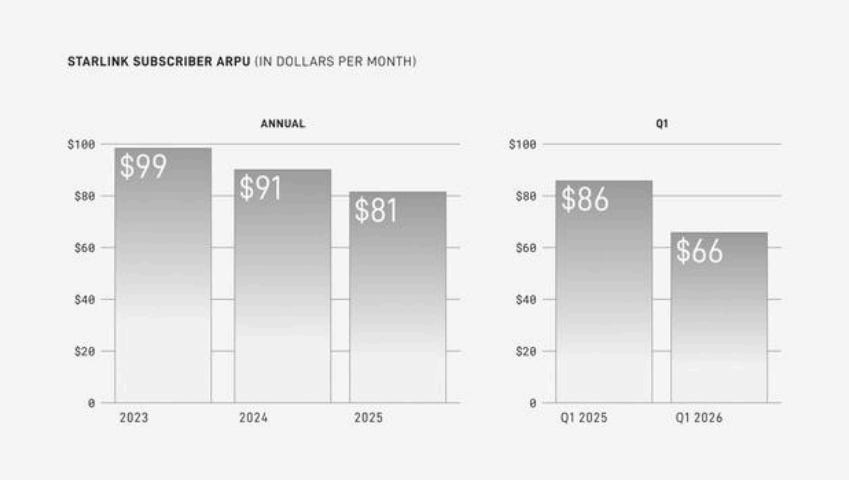

The Subscriber Business

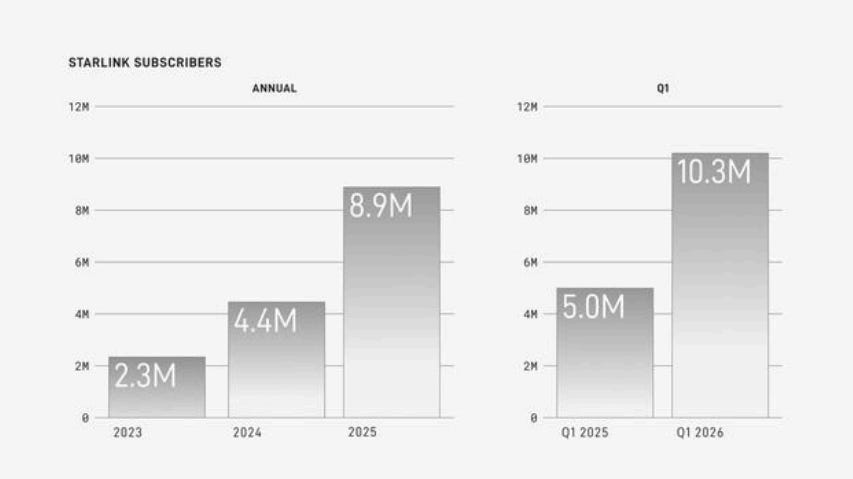

As of March 31, 2026: ~10.3 million Starlink Subscribers across 164 countries, territories, and other markets.

Year-over-year growth: up 105% from 5.0 million subscribers in Q1 2025.

A “Starlink Subscriber” is a unique Service Line directly assigned to a Starlink.com account registered to a person or entity without a direct, negotiated enterprise agreement. Because multiple people may share a single Service Line (e.g., a household), the actual number of individual human end-users accessing Starlink is already meaningfully higher than 10.3 million.

ARPU (Average Revenue Per User):

ARPU has declined from $99/month in 2023 to $66/month in Q1 2026. SpaceX explains this is deliberate:

International expansion into lower-income markets with lower-priced plans

Introduction of entry-level service tiers to maximize the addressable market

The company explicitly expects ARPU to continue declining as the subscriber base outside North America grows

The strategic bet is volume over price: 10 million subscribers at $66/month generates more total revenue than 2 million subscribers at $99/month, and the unit economics improve as network capacity grows. The prospectus discloses a global weighted average monthly residential broadband ARPU target of $31/month as the market matures, based on Omdia data, $43 in high-income markets, $16 in upper-middle income markets, and $9 in lower-middle and low-income markets.

Total addressable market for Starlink Broadband: ~$870 billion, based on approximately 1.8 billion global households.

Connectivity Segment Financial Performance

Connectivity is SpaceX’s cash engine. It generated $4,423 million in operating income in 2025, growing 120% year-over-year. This cash funds both the Space segment’s Starship R&D (which consumed $3,004 million in R&D in 2025 alone) and the AI segment’s infrastructure buildout.

Enterprise Solutions: Named Partners

The prospectus names SpaceX’s major enterprise customers across sectors:

Aviation (fleet-wide commitments or installations): United Airlines, Southwest Airlines, American Airlines, Qatar Airways, Lufthansa Group, British Airways, Alaska Airlines, Hawaiian Airlines

Maritime (full-fleet deployments): Carnival Corporation, Royal Caribbean Group, MSC Cruises, Norwegian Cruise Line Holdings

The global commercial fleet potential: ~23,900 commercial aircraft (per Oliver Wyman), ~24,500 privately owned aircraft (per Corporate Jet Investor), ~99,000 commercial merchant ships 100 GT or larger, ~21,000 fishing vessels, ~4,000 cruise ships and private yachts.

Land Mobility: John Deere (fleet connectivity), California Fire Department (emergency response), Brightline Florida (passenger rail), Italo Treno (Italian passenger rail)

Enterprise broadband global market opportunity: $200 billion across SMB and enterprise (per Grand View Research).

Government Solutions and Starshield

Civil Government: SpaceX provides connectivity for FEMA (disaster recovery coordination), NOAA (at-sea testing and environmental monitoring), the Government of the Philippines (remote island connectivity), the Government of Jamaica (maritime and remote digital access), and the Government of Ecuador (education and healthcare connectivity in isolated communities).

Starshield: A secure satellite network built specifically for national security applications. It leverages Starlink technology, manufacturing, and launch infrastructure, but with high-assurance cryptographic capabilities tailored to military requirements. Three core mission areas: Earth observation, global secure communications, and hosted payloads.

Starshield satellites can integrate a wide range of sensors and instruments, enabling government customers to deploy mission-specific capabilities in LEO without building standalone spacecraft for every program. Revenue from Starshield is included in the Connectivity segment under Government Solutions.

The government satellite communications market (public programs, excluding classified): $5 billion per Novaspace in 2025.

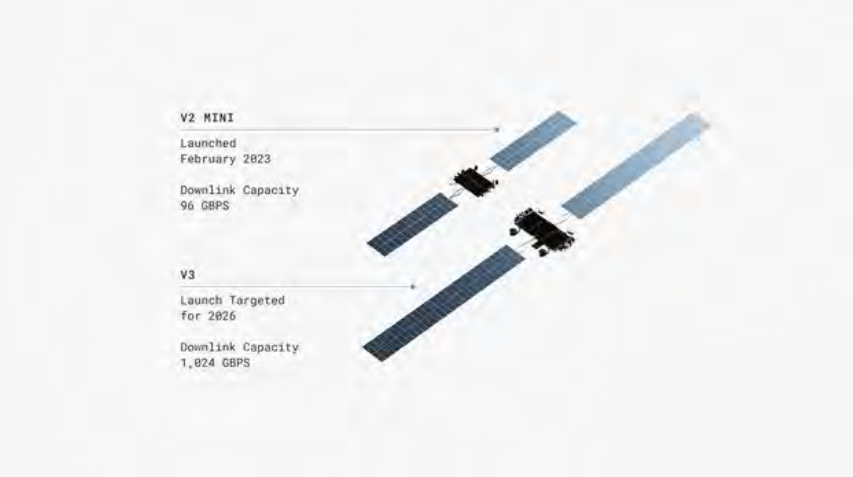

Next-Generation Satellites

V3 Broadband Satellites:

Downlink capacity: 1 Tbps per satellite (vs. V2 Mini)

Deployment: Using Starship, beginning H2 2026

Starship can deploy up to 60 V3 satellites per launch

Cost reduction: 9x vs. V1 from initial generation to V3

One V3 launch capacity equals the broadband downlink of approximately 20 Falcon 9 launches

Current constellation capacity: Over 700 Tbps cumulative downlink.

Starlink Terminal Economics:

Three primary consumer configurations:

Standard: Wide field of view; fixed residential and small business

Mini: Laptop-sized; mobility and travel; built-in Wi-Fi router; runs on 12V or portable battery

Performance: For demanding environments; maximum download speed over 450 Mbps; 110W+ power draw

All terminals support in-motion connectivity up to 100 mph and global oceanic coverage.

Starlink Mobile: The Direct-to-Device Network

Current status (as of March 31, 2026):

~650 V1 Mobile satellites in orbit

~7.4 million monthly unique devices served

~30 countries covered

~30 MNO partner agreements across 6 continents

Services: SMS messaging, over-the-top voice (WhatsApp, FaceTime), basic data

Regulatory approval in the U.S., Canada, the U.K., Japan, Australia, and several other countries

Named MNO Partners: T-Mobile (United States), One NZ (New Zealand), Optus (Australia), Telstra (Australia), Rogers (Canada), KDDI (Japan), Salt (Switzerland), Entel (Chile and Peru), Kyivstar (Ukraine), VMO2 (United Kingdom)

The EchoStar Spectrum Acquisition: In September 2025, SpaceX signed an agreement to acquire AWS-3, AWS-4, and H-Block spectrum licenses from EchoStar Corporation. Transaction approved by FCC on May 12, 2026; expected close: November 2027. The transaction involves 261,792,453 shares of Class A common stock plus cash consideration.

This spectrum acquisition is transformational for Starlink Mobile. The acquired AWS-4 and H-block frequencies are standardized for terrestrial 5G mobile broadband (3GPP bands n66 and n70). With V2 Mobile satellites and this spectrum:

Gen2 service is designed to provide 5G-like connectivity to existing unmodified devices in the United States (using spectrum leased from MNO partners) and potentially globally

The ultimate vision: Full 5G NR-NTN compliance providing broadband data and IoT connectivity, essentially eliminating mobile dead zones entirely

V2 Mobile Satellites: Deployment begins in 2027 (on Starship, approximately 50 mobile satellites per launch). Designed to provide broadband data and IoT connectivity in addition to messaging and voice, requires EchoStar spectrum acquisition to close and regulatory approvals in each market

The total addressable market for Starlink Mobile: $740 billion, based on approximately 8 billion globally connected mobile devices and a $8/month weighted average ARPU.

Additional Connectivity Markets

The prospectus identifies several emerging categories beyond traditional broadband and mobile:

Plaser Program: SpaceX allows third parties to purchase Starlink inter-satellite laser hardware and connect their own satellites to the Starlink mesh network, enabling orbital data routing without building their own relay architecture. This creates a new market for in-orbit data transport.

IoT: With 22 billion IoT devices globally in 2025 (forecast 47 billion by 2031), the Starlink Mobile Gen2 service is designed to support low-bandwidth IoT devices on the same constellation.

Enterprise Failover: As connectivity becomes mission-critical for enterprise operations, Starlink is positioned as the preferred backup for any business that cannot afford terrestrial network downtime.

You’ve covered the rockets and the satellites.

Everything behind this wall is where the real analysis lives.

The AI business. The complete financials. The IPO structure. The $28.5 trillion market opportunity. The full risk landscape. The vision statement.

Nine parts. Every number from the S-1. Nothing held back.

This is the most complete SpaceX breakdown available anywhere.

→ Join Fluent Few Premium — €25/month or €275/year

First 14 days on me. No questions asked.