Peter Lynch Would Love These 10 Companies

These companies meet nearly all of Peter Lynch’s key criteria for great investments.

Welcome back, Fluenteers! 👋🏻

Peter Lynch, one of the world’s most renowned investors, managed the Fidelity Magellan Fund from 1977 to 1990. During his tenure, the fund delivered an average annual return of approximately 29%, significantly outperforming the market. Lynch achieved this by following a philosophy of “investing in what you know,” focusing on companies with strong balance sheets, undervalued growth, and overlooked or unloved opportunities.

Here are ten companies that fit his criteria, and maybe you can achieve returns like Peter Lynch himself with this list.

Happy compounding!

Peter Lynch Stock #10: Crocs (Ticker: $CROX)

“Buy what you know.” This is that idea in its purest form.

Peter Lynch loved companies that regular people could understand. Crocs makes shoes that are instantly recognizable, wildly polarizing, and secretly brilliant. Once mocked. Now multiplied.

The business is built around one thing: Croslite™.

A proprietary foam resin that’s soft, durable, and addictive. Nurses swear by it. Kids wear them out. Gen Z made it cool again.

It’s not just the foam. It’s what they’ve done with it.

The Classic Clog is the anchor. Around it, Crocs has built:

Jibbitz™, the personalization engine that drives repeat purchases

Platform and Mega Crush, which turned the clog into a fashion item

HEYDUDE, an acquisition that added a whole new casual comfort category

The result? A rare combo of mass appeal and operating leverage.

Margins north of 50%.

High returns on capital.

A balance sheet that gives them options.

They don’t need to chase trends, they become trends. Lightning McQueen, Balenciaga, 7-Eleven... and it all works. Because it’s Crocs.

This is what Lynch meant by “The story’s simple, and it’s getting better.”

Customers love the product. The brand has legs. And it’s still growing globally.

It’s not just a shoe. It’s a phenomenon in foam.

Lynch would’ve seen it early, probably while walking past a store with his kids.

Peter Lynch Stock #9: Celsius Holding (Ticker: $CELH)

A product that sells itself, then keeps selling more.

Celsius doesn’t need a Super Bowl ad.

It’s already in your gym bag, your fridge, and your friend’s hand.

The company makes fitness-focused energy drinks that promise performance without the crash. Zero sugar. No artificial preservatives. Packed with caffeine and supplements like green tea and guarana.

Why it works?

The product delivers.

Try it once, and you’ll probably repurchase it.

That’s precisely the kind of consumer behavior Lynch loved: visible, habitual, and easy to understand.

Celsius has carved out a sweet spot between energy and health. Not quite Red Bull. Not quite Gatorade. But increasingly, a threat to both.

Growth has been explosive, fueled by:

A loyal fitness-first consumer base

Viral social media buzz and organic word-of-mouth

Rapid distribution gains through gyms, Amazon, and retail giants like Costco and Target

A strategic partnership with PepsiCo, unlocking shelf space nationwide

It’s not just hype. The numbers follow:

Triple-digit revenue growth in recent years

High gross margins for the beverage industry

Expanding operating leverage as volumes scale

A clean balance sheet with room to invest, not just survive

This is a company with a product you can see in real life, understand immediately, and track over time.

Lynch would’ve spotted it early, probably at a 5K, a college gym, or on his kid’s TikTok feed.

A simple story, backed by real demand, with a long runway ahead.

Celsius doesn’t just energize workouts. It energizes portfolios.

Peter Lynch Stock #8: Dollar General (Ticker: $DG)

Everyday essentials. Everywhere.

Peter Lynch loved boring businesses that quietly compounded. Dollar General is one of them.

It sells household essentials, such as paper towels, snacks, soap, and socks, across more than 20,000 stores in the U.S.

Not flashy. Not high-tech. Just relentlessly useful.

The formula is simple: small-format stores in rural and suburban areas, stocked with the essentials at low prices. No frills. No fuss. Just cash-generating square footage.

This model thrives where others can’t:

Towns too small for Walmart

Consumers living paycheck to paycheck

Shoppers who value speed, price, and proximity

Over 75% of Americans live within five miles of a Dollar General.

That kind of reach creates habitual traffic and high-frequency purchases.

Financially, it’s built to compound:

Strong unit economics with low buildout costs

Consistent same-store sales growth

High returns on capital and significant free cash flow

Store expansion funded internally, not with heavy debt

It’s a classic Lynch stock, “I can explain it to my kid in 30 seconds.”

And that’s exactly the point.

When consumer habits tighten, Dollar General gets stronger.

It’s where people go when they trade down, and often, where they keep going afterward.

A slow, steady, essential machine.

Still expanding. Still predictable. Still investable.

Peter Lynch Stock #7: Five Below (Ticker: $FIVE)

Fun, fast, and under $5, most of the time.

Peter Lynch loved walking into a store, seeing people excited to spend money, and realizing: this stock sells itself.

That’s Five Below.

It’s a high-energy retail chain targeting tweens, teens, and value-hunting parents. Bright colors, loud displays, and new inventory weekly. Everything is priced to feel like a deal, usually under $5, with a growing “Five Beyond” section for slightly higher-ticket items.

What it sells:

Phone accessories, toys, candy, beauty, seasonal goods

Trendy merch that rides cultural waves (Taylor Swift, slime, Squishmallows)

Impulse buys that don’t need a second thought

The model works because it makes spending feel good, without guilt.

And that behavior is repeatable.

Stores are cheap to open, quick to become profitable, and incredibly scalable.

The company sees 3,500+ U.S. store potential, and it’s still under halfway there.

Financially, Five Below checks all the boxes:

High sales per square foot

Strong margins for value retail

High returns on invested capital

Long runway of self-funded growth

It’s retail done right: fast inventory turns, engaged customers, and a loyal demographic that grows up but keeps coming back.

Lynch would’ve spotted it while shopping for birthday gifts with his kids.

Simple story. Fun experience. Powerful economics.

Five Below is low price, high quality, and that goes for the stock, too.

Peter Lynch Stock #6: Sprouts Farmers Market (Ticker: $SFM)

Health food without the Whole Foods price tag.

Peter Lynch loved niche retailers with loyal customers and repeatable habits.

Sprouts checks all the boxes, and stocks all the produce.

It’s a fresh-focused grocery chain built around natural, organic, and specialty foods, but without the pretentious markup.

Think Whole Foods quality in a more accessible, neighborhood-friendly format.

The store layout is simple and consistent:

Fresh produce at the center. High-turn health staples around the perimeter. Bulk bins, vitamins, and better-for-you snacks throughout.

Sprouts attracts a specific kind of shopper:

Health-conscious families

Millennials who read ingredient labels

Price-sensitive consumers who still care what’s in their food

The business wins by staying tight:

Stores are smaller than traditional grocers → lower rent, higher turns

Private-label brands drive margins and loyalty

Focus on perishables means less head-to-head with big-box retailers

Expanding DTC and digital integration without losing in-store identity

Sprouts isn’t trying to win the entire grocery market, just the slice that shops with intention.

Financially, it’s quietly efficient:

Steady free cash flow

Strong returns on invested capital

A disciplined store rollout strategy across the Sun Belt and beyond

Plenty of white space for growth without overstretching

This is classic Lynch: a business you can understand just by walking in.

Healthy margins. Healthy food. Healthy upside.

Sprouts doesn’t need to dominate, just execute.

Peter Lynch Stock #5: Texas Roadhouse (Ticker: $TXRH)

Steak, beer, and a 30-minute wait, that’s the business model.

Peter Lynch loved restaurants with packed parking lots and loyal regulars.

Texas Roadhouse delivers that, night after night.

It’s a full-service steakhouse chain with a focus on value, volume, and consistency.

No gimmicks. No reinvention. Just hearty food at fair prices, served fast, with country music and peanuts on the floor.

Customers don’t come for innovation. They come for the same $15 ribeye they ordered last time, and the time before that.

The model runs on:

High foot traffic and table turnover

Strong unit-level economics

Scratch kitchens with simple, replicable menus

A culture of decentralization, local managers run the show, not corporate

This isn’t fast food, but it’s fast casual dining.

That keeps margins tight, experiences reliable, and customers loyal.

Financially, Texas Roadhouse sizzles:

High and stable return on capital

Consistently strong same-store sales

Conservative balance sheet with steady dividend growth

Expansion funded by operating cash flow, not dilution

And importantly, it grows without losing its soul.

Each new location feels like the last, on purpose.

Lynch would’ve spotted this one after seeing lines out the door on a Wednesday night.

It’s a simple business, with sticky habits and efficient execution.

More steak. More stores. More upside.

Peter Lynch Stock #4: Trex Company (Ticker: $TREX)

Wood decks rot. Trex doesn’t. That’s the pitch.

Peter Lynch loved companies that offered a better product at a better price over time.

Trex does exactly that, by replacing traditional wood with long-lasting composite.

It pioneered the composite decking category, using recycled plastic and wood fibers to create outdoor products that don’t warp, splinter, or need staining.

The result? A deck that looks like wood but outlasts it, and often pays for itself in maintenance savings.

Homeowners love it. Contractors recommend it.

And once it's installed, it's there for decades.

Trex has a dominant share in a growing market:

Composite decking penetration is still under 25% of total decking in North America

Trex holds the #1 brand position, with the scale and reputation to match

Low-cost manufacturing, proprietary formulations, and a vast pro channel network

Growth is built into the model:

Rising demand for low-maintenance outdoor living

Ongoing conversion from wood to composite

Upsell into railings, lighting, cladding, and fencing

Green tailwinds: made from 95% recycled material

Financially, it’s rock solid:

Strong gross margins and expanding operating leverage

Capital-light manufacturing with high returns

Consistent free cash flow and smart capital allocation

This is the kind of business Lynch would’ve discovered while remodeling his deck, then bought after realizing the neighbors were doing the same.

Trex isn’t chasing fads. It’s replacing an outdated material with something better.

Quietly. Permanently. Profitably.

Peter Lynch Stock #3: Progyny (Ticker: $PGNY)

Fertility benefits that actually work, for patients and employers.

Peter Lynch loved businesses solving real problems in growing markets.

Progyny tackles one of the most personal and expensive: fertility.

It’s a benefits platform that helps employers offer fertility, surrogacy, and family-building services through a smarter, more supportive system.

No more one-size-fits-all coverage. Progyny gives employees a care advocate, bundled services, and access to top clinics with better outcomes.

For patients: fewer failed cycles, more success, less stress.

For employers: cost control, retention, and a powerful DEI story.

Adoption is spreading fast:

Used by over 460 large employers, including Google, Microsoft, and Amazon

Embedded into Fortune 500 HR packages

Covers millions of lives, and counting

What makes the model powerful:

High switching costsare once embedded into HR systems

Recurring revenue through self-insured contracts

Expanding wallet share as employers add adjacent services (e.g., menopause, adoption support)

Network effects as clinic data improves outcomes across the board

Financially, Progyny is built for long-term compounding:

Consistent revenue growth

Scalable platform with healthy margins

Strong client retention and high NPS

Capital-light with efficient reinvestment

Lynch would’ve asked his HR department how fertility benefits worked, and bought the stock after realizing nobody was happy with the old system.

Progyny isn’t just selling benefits.

It’s solving a deeply human need, with precision and empathy, and building a category-defining business while doing it.

Peter Lynch Stock #2: Latham Group (Ticker: $SWIM)

If you’re putting in a pool, there’s a good chance it’s Latham.

Peter Lynch loved spotting picks-and-shovels businesses in growing lifestyle trends.

Latham is that pickaxe in your neighbor’s backyard.

It’s the largest manufacturer of in-ground residential pools in North America. Specializing in fiberglass and vinyl liner pools, Latham’s products are easier to install, have lower maintenance, and are longer-lasting than traditional concrete.

And crucially, they’re prefabbed off-site.

That cuts install times from weeks to days and solves the skilled labor shortage that’s stalling backyard projects across the country.

The business swims in a wide moat:

Largest scale and dealer network in the category

Proprietary fiberglass molds and automation that competitors can’t replicate

Lifetime warranties on shells build trust with installers and homeowners alike

Asset-light model with licensing revenue from branded components

Homeowners are spending more on outdoor living. And once a family decides to get a pool, they don’t wait for a downturn to cancel.

Financially, it’s structurally sound:

High-margin product mix

Efficient manufacturing footprint

Long replacement cycle = minimal competition from used inventory

Pricing power in a fragmented industry

There’s still plenty of room to grow:

Fiberglass penetration is still low compared to concrete

Geographic expansion across the Sun Belt and the Midwest

Cross-sell into covers, liners, steps, automation, and branded accessories

Lynch would’ve spotted this after seeing trucks deliver pool shells around his neighborhood.

Simple idea. Premium product. Strong share.

Latham doesn’t sell pools. It sells summer, faster, better, and with fewer headaches.

Peter Lynch Stock #1: Middleby Corporation (Ticker: $MIDD)

The kitchen behind the kitchen.

Peter Lynch loved companies hiding in plain sight, especially B2B businesses that power everyday life, even if consumers don’t know they exist.

Middleby fits that mold perfectly.

It’s one of the world’s leading makers of commercial kitchen equipment, serving restaurants, hotels, hospitals, and convenience stores. Walk into a Chipotle, Starbucks, or Pizza Hut, chances are you’re seeing Middleby hardware in action.

Ovens. Grills. Refrigeration. Beverage systems. Automated fryers.

If it makes food faster, hotter, safer, or more consistent, Middleby likely makes it.

The business is built on:

A portfolio of premium brands (TurboChef, Blodgett, Taylor, and more)

Deep relationships with foodservice chains and kitchen consultants

Strong pricing power via reliability, energy efficiency, and performance

A growing ecosystem in residential luxury and food processing

This isn’t just about selling hardware, it’s about enabling efficiency:

Higher throughput in smaller footprints

Energy savings in high-volume kitchens

Automated cooking that reduces labor dependence

Financially, it’s a quiet compounding machine:

Healthy operating margins and strong free cash flow

Repeat revenue from parts, servicing, and replacement cycles

Smart bolt-on acquisitions that expand the category and capability

Capital discipline with steady buybacks and reinvestment

Middleby doesn’t rely on trends. It relies on kitchens operating smoothly, all day, every day.

Lynch would’ve spotted this one by talking to a restaurant manager, or poking around behind the counter.

Simple business, once you see it.

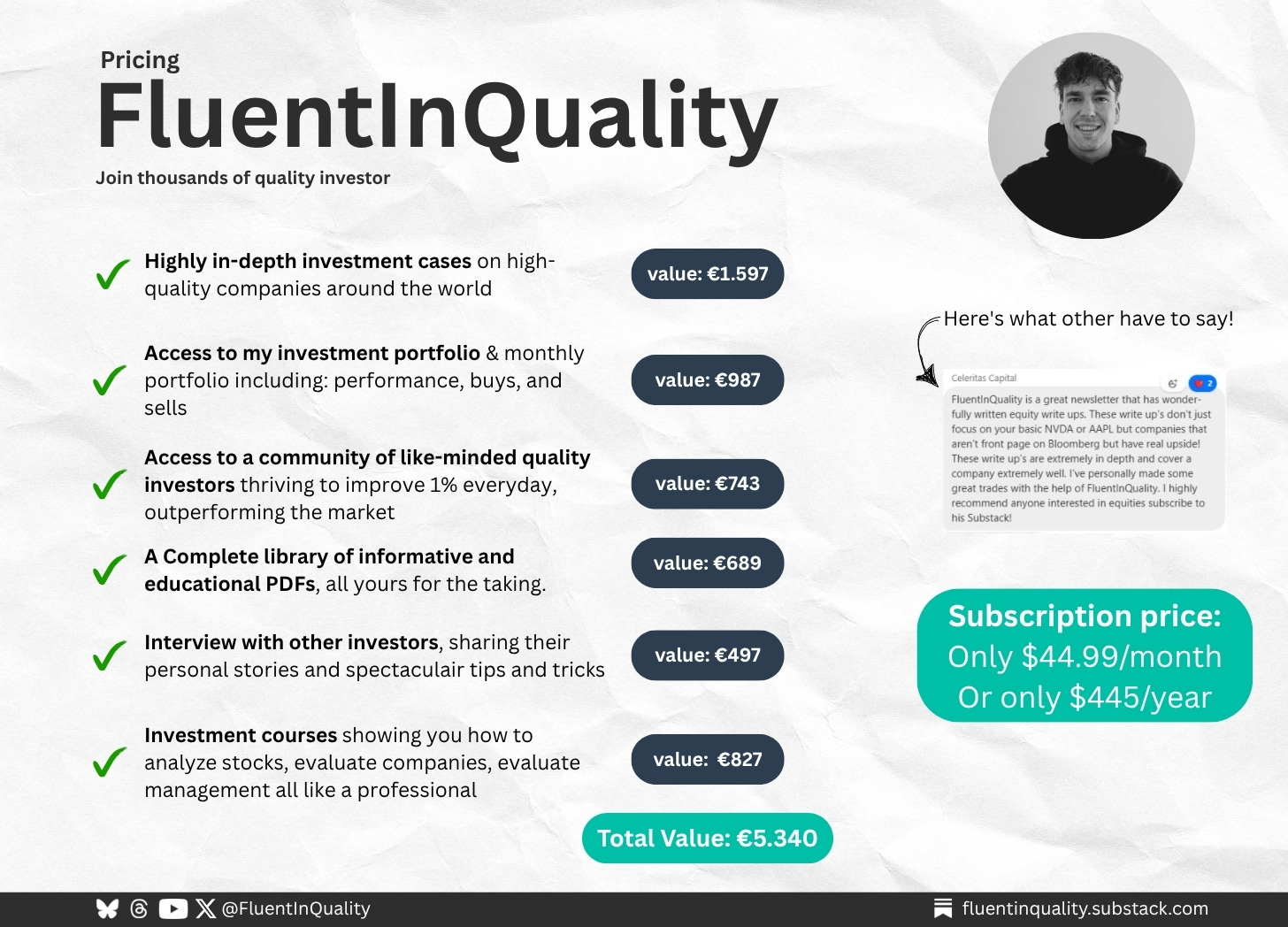

Ready to go from reading about great businesses to owning them with conviction?

✔️ Full research reports and timeless deep dives (valued at €1,597)

✔️ Monthly buy/sell portfolio updates with commentary (€987)

✔️ Access to a private Discord of high-conviction investors (€743)

✔️ Tools, templates, investor interviews & PDF briefs (€2,013)

Total value: €5,340 — yours for just €44.99/month or €445/year.

No fluff. No noise. Just real work, trusted by 1,200+ long-term investors.

This isn’t just insight. It’s an investing advantage.

Delivered weekly. Backed by research. Built to compound.

🟢 Become one of The Fluent Few

Let’s build wealth the right way—brick by brick.

PS…. if you’re enjoying FluentInQuality, can you take 3 seconds to refer this edition to a friend? It will go a long way in helping me grow the newsletter (and bring more quality investors into the world).

Great investments don’t shout, they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.

Thanks for recommending Finchat.