Lessons From Dev Kantesaria You Can Use Today!

Dev Kantesaria’s Valley Forge Capital has crushed the S&P 500 with a focused portfolio. Here’s his philosophy—and how you can use it too!

Hi, partner! 👋🏻

Occasionally, I encounter a super investor and his fund, and I’m bewildered by their results, attitude toward investing, simplicity, patience, and overall approach.

A couple of years ago, I came across Dev Kantesaria, the founder of Valley Forge Capital with $4B AUM. Dev Kantesaria isn’t the typical name you hear when discussing super investors. Usually, you’ll hear names like Warren Buffett, Peter Lynch, Terry Smith, Charlie Munger, and other super investors who’ve shaped the investing world and philosophy.

Dev Kantesaria and his fund, Valley Forge Capital, have achieved an annualized return of roughly 15% since inception in 2007, beating the S&P 500, which annualized roughly 10.53% in the same period. These returns are attributed to his quality investment style, which involves focusing on the highest-quality businesses on the stock market. This type of high-quality investing is reflected in his portfolio, which includes names like Fair Isaac Corp., S&P Global Inc., Mastercard Inc., Moody Corp., and many more high-quality businesses.

In today’s article, we’ll go over who Dev Kantesaria is, his approach to investing, and how he achieves these generous returns.

P.S. Share the newsletter with your friends and family if you like it. This would mean the world to me. ❤️

Happy reading!

Who is Dev Kantesaria?

Dev Kantesaria is an American-born and raised investor and the founder of Valley Forge Capital Management, a hedge fund known for its concentrated investment strategy where he solely focuses on owning the highest quality businesses.

Kantesaria’s interest in business began at an early age, as young as eight. He pursued a Bachelor of Science in Biology at the Massachusetts Institute of Technology (MIT) and later attended Harvard Medical School. Not long after, He realized his true passion was in business, leading him to transition away from medicine.

“I’ve studied a lot of playbooks over the years starting at age eight, and the one that resonated with me the strongest was the Buffett Munger playbook which is to focus on business quality.” — Dev Kantesaria

After leaving the medical field, Kantesaria began his professional career as a management consultant at McKinsey & Co. in 1998 until 2000. After his journey at McKinsey & Co., he spent 6 years as a venture capitalist in the healthcare sector, gaining immense operational experience. After being a venture capitalist for 6 years, he becomes a General Partner for another 11 years. After these endeavors, Kantesaria started his fund in 2007.

Investing Strategy

To start this part with a bang, take in the following statement on his website.

‘‘At Valley Forge Capital Management (“VFCM”), we believe that having the proper temperament and discipline is key to superior investment returns. Practicing patience and remaining unemotional through market swings allows VFCM to take advantage of opportunities when we see others behaving irrationally or fearfully.’’ - Dev Kantesaria

This statement alone tells us much about who he is and how he approached investing. A fund manager who has earned +15% annualized returns since 2007 must be disciplined, patient, and unemotional.

VFC (Valley Forge Capital) focuses on quality businesses and holding these for as long as possible. We’ve all heard it plenty of times, just buy-and-hold the damn stock.

Kantesaria focuses on having a concentrated portfolio that holds the best businesses in the world. Why would you only allocate, let’s say, 4% to a business that is a high-conviction idea? Kantesaria argues, and I agree here, that you should have a couple of businesses in your portfolio that bear a high conviction. When you have these, you bet big on them.

As shown above, Kantesaria practices what he preaches.

Kantesaria holds large positions in his businesses that have a high conviction. And do note these businesses are where all quality investors agree that they are of high quality.

Kantesaria identifies companies with a MOAT (especially those with pricing power), competent management, and predictability in earnings and growth. He also favors businesses that are part of a monopoly or oligopoly with operational leverage and low reinvestment requirements. This strategy targets industries with long-term growth trends and companies capable of raising prices above inflation, ensuring profitability even during economic headwinds.

In addition, Kantesaria favors businesses with minimal capital expenditures and research and development requirements, leading to higher returns on tangible assets and more efficient use of free cash flow.

After finding a business that fits Kantesaria's criteria, he evaluates it and waits until he can buy shares below its intrinsic value with a modest margin of safety and potential for significant appreciation as the market sees the company’s true value. After buying into the business, Kantesaria plays the waiting game. Kantesaria adopts a long-term investment horizon, often holding companies for a decade or more, allowing the intrinsic value of high-quality businesses to compound over time.

‘‘I don’t need to have a share price every day, every month, or year. I know I bought an excellent business at a fair price.’’ - Dev Kantesaria

The performance of his fund is nothing short of excellent. Kantesaria has generated consistent returns for his investors, reflecting the power of his investment strategy and philosophy. Although his philosophy is the "standard," not everybody acts on it, and their returns show it. Kantesaria practices what he preaches, and his returns are a testimonial to his simple yet effective approach to investing.

You might have noticed that Kantesaria’s investment approach and philosophy align almost perfectly with those of Warren Buffett and Charlie Munger. This is not a coincidence! Kantesaria has mentioned plenty of times that he has studied Warren and Charlie for most of his career, and he resonates with their approach's simplicity yet effectiveness.

VFC believes that a concentrated portfolio of high-conviction ideas is the only way to significantly outperform relevant benchmarks over the long term. Therefore, new positions at VFC must meet rigorous criteria for business quality, financial metrics, and operational standards.

What Are Dev Kantesaria’s Criteria for Quality?

We’ve clearly shown that Kantesaria invests in high-quality businesses. According to Kantesaria, roughly 50 companies globally meet his strict criteria.

His criteria?

Strong competitive advantages: These include elements like brand strength, economies of scale, or network effects. For example, network effects occur when a product or service becomes more valuable as more people use it, like social media platforms or payment networks.

High return on capital: A high ROIC indicates that a company efficiently converts investments into profits. For instance, an asset-light business model allows a company to scale without massive reinvestment, boosting profitability.

Recurring revenue models: Businesses with recurring revenue often have a subscription-based model, ensuring consistent cash flow and higher customer retention. Predictable revenues help reduce volatility in financial performance.

High free cash flow margins: Free cash flow indicates how much profit is truly available after all operating and capital expenses. A company with high margins can reinvest in growth, reduce debt, or return cash to shareholders.

Minimal capital requirements: Businesses that don’t need significant ongoing investments (e.g., factories or equipment) to grow are more scalable. This means higher profits can be reinvested in R&D or shareholder returns rather than upkeep.

Long growth runway: A long growth runway suggests the market for a company’s products or services is still expanding. For example, e-commerce penetration in global markets continues to grow, leaving room for companies in this space to scale.

Exceptional management teams: Effective leaders allocate capital wisely, avoid over-leveraging, and align with shareholder interests. They are often identifiable by a consistent track record of improving operational performance.

Low leverage: Companies with low debt have lower financial risk and are better equipped to handle economic downturns. This allows them to reinvest in growth or acquisitions during favorable times.

Predictability and simplicity: Simple businesses are easier to analyze and manage. Predictable revenue streams and customer behaviors reduce risks, making these businesses less prone to external shocks.

Valuation discipline: Buying even high-quality businesses at inflated prices increases risk. Valuation discipline ensures a margin of safety, allowing for potential underperformance without catastrophic losses.

In-Depth Holding Analysis

Let’s go over Dev Kantesaria's few holdings in a bit more depth. It’s indisputable that Kantesaria’s holdings are those of high quality, but what makes these companies of such high quality? I will not go over their fundamentals.

P.S. Dev Kantesaria holds both a Visa and a Mastercard. They’re both the same business and are extremely similar. I will cover solely Mastercard to avoid repeating myself too much, thank you for your understanding.

Let us begin with Fair Isaac Corp.

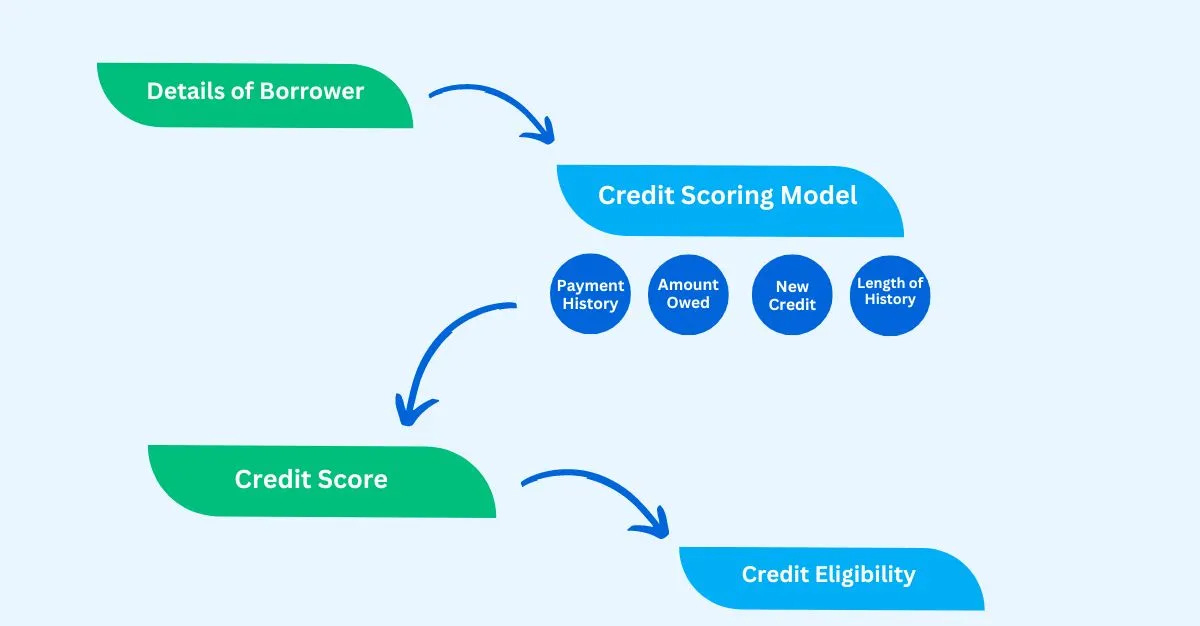

Fair Isaac is the dominant player in the credit scoring industry. Here is a quick summary of how this scoring works:

Fico comes to play in the scoring part of the process. Together with its software and the gathered information, Fico gives a credit score. It’s a fairly simple business model. That software part is partially Fico’s MOAT as well. Its proprietary algorithms and historical data make it tough for competitors to hop into this market and try to get a piece of the pie.

Fico generates significant revenue from recurring sources, such as licensing fees and subscription-based Saas solutions. This, in return, provides a predictable and stable cash flow for the business. Since there’s a subscription and software, Fico benefits from excellent margins, and Fico can maintain and sometimes even improve these margins. This, in return, gives Fico the ability to convert a significant portion of its revenue into free cash flow, a part most investors love.

In addition to this, Fico is a very asset and CapEx light. Fico is a software business, and these types of businesses usually require less CapEx. This allows Fico to reinvest in R&D, expand its offerings, and return cash to shareholders.

Last but not least, Fico has an extremely long runway. The increasing digitization of financial services and the growing dependency on credit scoring and analytics provide Fico with a long growth runway. There’s competent management at the wheel of the business, and they’re capable of using every aspect of Fico to their advantage, rightly so.

Small side note: lenders, banks, and other financial institutions rely heavily on Fico’s score for their risk assessment. Switching to alternative providers would involve significant time, cost, and risk, creating an extremely sticky customer base.

S&P Global.

S&P Global is the leader in credit ratings for financial indices (like the S&P 500) and market intelligence. These services are extremely important to the global financial system.

Most of their revenue comes from a recurring-based model, such as subscriptions-based data and analytics services. S&P Global Ratings generates fees tied to bond issuance, which means revenues increase during periods of high debt issuance, offering cyclical upside with a stable baseline.

As a knowledge-driven business, S&P Global requires few capital expenditures, which allows it to maintain high free cash flow margins and reinvest in acquisitions, innovation, or shareholder returns.

Its credit ratings are embedded in global debt markets, and financial institutions, corporations, and governments rely on them to issue debt. Switching away from S&P’s services is costly and impractical, creating sticky customer relationships.

Expansion in ESG (Environmental, Social, and Governance) data and analytics positions S&P Global at the forefront of a rapidly growing market. Increasing demand for data-driven decision-making fuels growth in its Market Intelligence and Indices divisions.

The company has four major segments: ratings, Market Intelligence, Indices, and Platts (commodities analytics). This diversification reduces its dependency on a single revenue source and makes it resilient in various economic environments.

S&P Global is known for disciplined capital allocation, with management consistently reinvesting in high-return projects, strategic acquisitions, and returning excess capital to shareholders. Recent acquisitions like IHS Markit have strengthened its data and analytics offerings.

Through dividends and stock buybacks, S&P Global has delivered high returns on capital and exceptional shareholder value. Its ability to generate high free cash flow year after year enables long-term reinvestment in the business while rewarding shareholders.

Mastercard

Mastercard operates one of the largest global payment networks, connecting billions of consumers, merchants, and financial institutions. The network effect strengthens its moat: as more users and merchants adopt Mastercard, the network becomes increasingly valuable and harder to replicate.

As a payment processor, Mastercard does not bear credit risk like banks. Instead, it earns a percentage of transaction volumes, making its business capital-light and scalable. Growth in transactions requires minimal additional investment, leading to high operating margins.

Mastercard consistently generates exceptional free cash flow, which can be reinvested into growth initiatives, share buybacks, or dividends. Its asset-light model supports operating margins above 50%, highlighting its efficiency and profitability.

Mastercard benefits from recurring revenue streams tied to global transaction volumes, which grow with consumer spending, e-commerce expansion, and financial inclusion in emerging markets. Its international footprint makes it less dependent on any single economy, adding resilience to its revenue streams.

Cashless transactions continue to rise globally, providing Mastercard with a long growth runway. Opportunities in digital wallets, contactless payments, and fintech partnerships further enhance the company's growth potential.

Building a global payment network like Mastercard’s requires decades of investment, trust, regulatory approvals, and partnerships. These create high barriers to entry, shielding it from new competitors.

Mastercard’s management has a track record of disciplined capital allocation, including strategic acquisitions and partnerships to strengthen its position in emerging markets and digital payments.

Moody’s Corp

Moody’s is one of the "Big Three" credit rating agencies (along with S&P Global and Fitch), providing credit ratings integral to the global financial system. Its moat is built on regulatory reliance (regulators require ratings), brand trust, and high barriers to entry due to decades of credibility and an established network.

A significant portion of Moody’s revenue comes from recurring sources, such as subscription-based data and analytics services through Moody’s Analytics. This creates a predictable and stable cash flow, even during economic downturns.

Moody’s operates an asset-light business model with exceptionally high profit margins. The company converts a significant portion of its revenue into free cash flow, allowing for reinvestment, acquisitions, and shareholder returns through dividends and share buybacks.

Moody is pivotal in global debt issuance by providing credit ratings influencing investor decisions and borrowing costs. As debt issuance continues to grow globally, especially in emerging markets, Moody’s stands to benefit significantly.

While credit rating revenue can be somewhat cyclical (tied to bond issuance), Moody’s Analytics segment provides countercyclical stability. It offers data, research, and risk management solutions that remain in demand regardless of market conditions.

The industry requires regulatory approvals, decades of trust-building, and a massive data infrastructure, creating significant barriers for new competitors. Its entrenched position ensures dominance and pricing power.

Moody’s management has a history of prudent capital allocation. It has focused on strategic acquisitions and investments that strengthen its data and analytics capabilities. For example, its acquisition of Bureau van Dijk enhanced its ability to provide valuable insights to customers.

Its services are critical for issuers, investors, and governments, creating high switching costs. Institutions heavily rely on Moody’s insights to make informed decisions. This reliance makes Moody’s revenue streams incredibly stable and predictable.

Moody’s delivers exceptionally high returns on invested capital (ROIC) and has a long history of rewarding shareholders through dividends and stock buybacks. Its ability to grow revenue and profits over the long term reflects its strong operational efficiency and market dominance.

Intuit

Intuit is a leader in financial software solutions, with flagship products like TurboTax, QuickBooks, and Credit Karma dominating their respective markets. Its strong brand recognition and trust among consumers and small businesses create a competitive advantage.

Intuit has a subscription-based revenue model, with most of its income coming from recurring services such as QuickBooks Online and TurboTax’s annual tax preparation subscriptions. High customer retention ensures stable and predictable cash flows.

Intuit operates a highly profitable business model with strong margins and consistent free cash flow generation. The software and SaaS model allow the company to scale efficiently without heavy capital investments.

Intuit requires minimal capital expenditures as a software company compared to industrial or physical product businesses. This asset-light model allows for higher reinvestment in R&D and shareholder returns.

QuickBooks benefits from network effects. Accountants, small businesses, and app developers integrate into its ecosystem, making it more valuable for all users. This ecosystem makes it difficult for customers to switch to competitors, creating a sticky customer base.

Intuit continuously invests in AI, automation, and cloud-based technologies, enhancing the functionality and efficiency of its products. For example, its AI-driven tax preparation and bookkeeping solutions improve user experience while driving efficiency.

Intuit’s growth is supported by the increasing digitization of finance, particularly among small businesses and individuals managing their finances online. Acquiring Credit Karma and Mailchimp expands Intuit’s footprint in personal finance and marketing automation, opening up new growth opportunities.

Intuit’s leadership has a track record of disciplined capital allocation, including strategic acquisitions like Mailchimp and Credit Karma. These acquisitions align with the company's mission of financially empowering consumers and businesses. The company consistently returns value to shareholders through dividends and share buybacks.

ASML

ASML is the sole supplier of extreme ultraviolet (EUV) lithography machines, a cutting-edge technology essential for producing the most advanced semiconductor chips. This monopoly creates a significant moat, as competitors cannot replicate its technology or expertise.

ASML’s equipment is indispensable to leading chipmakers like TSMC, Samsung, and Intel, enabling them to manufacture smaller, more powerful, and energy-efficient chips. Its tools are foundational to AI, 5G, autonomous vehicles, and IoT innovations, making ASML a critical player in technological advancement.

ASML’s technology is protected by decades of R&D investment, a deep pool of intellectual property, and complex manufacturing processes. The high cost of developing and producing EUV machines creates barriers that prevent new entrants from competing.

Due to its unique position and the critical nature of its equipment, ASML has strong pricing power. This enables it to maintain high margins and pass on cost increases to customers.

The global demand for semiconductors is expected to grow significantly as industries increasingly rely on digital technology. ASML’s EUV and DUV (deep ultraviolet) lithography systems are key enablers of this growth, providing the company with a sustainable growth trajectory for years to come.

In addition to selling lithography machines, ASML generates recurring revenue from service contracts, upgrades, and spare parts for its installed base. This recurring income ensures predictable cash flows and strengthens customer relationships.

ASML consistently delivers high operating margins and strong free cash flow, reflecting its efficiency and profitability. Its asset-light model enables the company to reinvest heavily in R&D while returning capital to shareholders through dividends and share buybacks.

ASML has long-term partnerships with leading semiconductor manufacturers like TSMC, Samsung, and Intel. These relationships are built on trust and reliance, ensuring a steady demand for ASML’s products and services.

Aspen Technology

AspenTech is a leader in providing asset optimization and process engineering software for energy, chemicals, and manufacturing industries. Its solutions are deeply embedded in customers' operations, making them critical for optimizing efficiency, reducing costs, and improving productivity.

AspenTech benefits from specialized expertise and decades of accumulated industry knowledge, which are difficult for competitors to replicate. Its software is tailored for complex industrial processes, requiring significant R&D and customer relationships to compete effectively.

AspenTech’s solutions are often mission-critical for its customers, making switching to competitors costly and risky. Once integrated, the reliance on its software creates a sticky customer base and ensures recurring revenue.

Most of AspenTech’s revenue comes from subscription-based licenses and maintenance contracts, providing predictable and stable cash flows. Its transition to a subscription model has further strengthened its recurring revenue streams.

AspenTech operates with exceptionally high gross and operating margins, reflecting its scalable software business model. The company generates significant free cash flow, enabling reinvestment in R&D, strategic acquisitions, and shareholder returns.

Due to its specialized offerings and critical role in optimizing industrial processes, AspenTech has the ability to command premium pricing for its software solutions. Its customers see AspenTech’s software as a cost-saving investment, justifying its high pricing.

AspenTech is positioned to benefit from global trends like digitization, industrial automation, and the energy transition. Industries increasingly rely on data and AI-driven solutions to optimize operations, which aligns perfectly with AspenTech’s offerings.

AspenTech’s management has a proven track record of disciplined capital allocation and strategic acquisitions that enhance its product portfolio. Recent acquisitions have expanded its reach into asset management and sustainability, further strengthening its market position.

My Takeaway

It’s indisputable that Dev Kantesaria is an exceptional, highly disciplined investor and one of the top five quality investors.

His insights and wisdom have inspired me to think differently, particularly about my portfolio. I’ve often struggled with the question, "How much do you allocate to your stocks?" His perspective has provided me with a fresh and insightful approach. Dev Kantesaria argues that if you pick 17 stocks, you’re doing something wrong—and he’s right. I’ve realized I have a few high-conviction ideas, and my focus should be on these rather than adding a good company to my portfolio with just a 5% allocation. I’m determined to take action. Over the coming months and years, I will scale down my portfolio and double down on my highest-conviction ideas.

Focusing on a few deeply researched ideas brings me peace of mind and allows me to truly understand my portfolio. I’m learning more every day, and sometimes I stumble upon golden nuggets of wisdom, like Dev Kantesaria’s insights. It’s my responsibility to absorb these lessons, deepen my understanding, and take action. If it doesn’t work, at least I’ll know I tried. If it does, it could benefit me for decades, and I’ll thank my younger self for staying curious and taking that leap.

Additionally, Dev Kantesaria has given me a refreshing perspective on quality—what defines a high-quality business, how to analyze its MOATS, and much more. This deeper understanding of true quality investing has helped me set clearer expectations for the type of returns I can achieve when properly applying his philosophy.

Do not be surprised when this year there will be some (major) changes in my investment approach. Dev Kantesaria has given me extremely valuable new insights, and I will try my best to implement these to +1 my investing and +1 the quality that I provide to you all.

Look for the best business models in the world and bet big on them.

That was it for today! If you’re new here, subscribe to never miss out on any post.

And remember

Great investments don’t shout—they compound quietly.

- Yorrin (FluentInQuality)

Dev is a fascinating, articulate investor; thanks for your work on his approach and portfolio. A couple of things:

1. He has sold the Aspen position as of his most recent 13F filing.

2. He doesn't view S&P's IHS Markit acquisition positively; he sees it as weakening its business. He would prefer they stick with the higher quality businesses of ratings and indices.

3. He recently bought MSCI. It is certainly high quality, but I haven't been able to come to a valuation that would have afforded him a margin of safety.

In essence, a company growing slower but longer beats the company growing faster but eventually dying out.