9 Niche Companies With Deep & Wide Economic Moats

These companies aren't discussed that much, and that makes these beautiful.

Welcome back, Fluenteer! 👋🏻

Everyone is busy discussing the most prominent companies, such as Google, Amazon, Meta, Tesla, and others. We are familiar with them, primarily due to the extensive coverage of these companies. But, there are some niche companies out there that aren’t discussed that much but benefit from either a deep or wide moat.

Here, we’re discussing nine companies that investors rarely discuss but possess a solid economic moat.

Happy compounding!

Niche Company #9: Spirax-Sarco Engineering (Ticker: $SPX.L)

Built for permanence. Grown through necessity.

Spirax-Sarco designs thermal energy control systems.

Steam, electric thermal, and fluid control solutions that keep global industries running.

Precision isn’t optional. It’s foundational.

Downtime isn’t acceptable. Spirax prevents it.

Compliance isn’t a target. It’s built-in.

Purpose-built. Quietly essential.

Spirax-Sarco isn’t loud.

It wins by being indispensable.

Power generation

Pharmaceuticals

Food & beverage

Chemicals

Heavy industry

Where there’s steam, heat, or process control, Spirax-Sarco is often the backbone.

Embedded by expertise.

Steam systems aren’t simple.

They demand deep process knowledge and flawless execution.

Specified early

Consulted regularly

Replaced rarely

Switching costs are practical, not contractual.

A change risks safety

A change risks efficiency

A change risks regulatory compliance

Once Spirax is in, it tends to stay.

The portfolio compounds itself.

Growth comes from the installed base.

Revenue expands without chasing new clients.

New system installations

Energy efficiency retrofits

Maintenance contracts

Spare parts

Ongoing technical support

Every system is a long-term relationship.

Every retrofit deepens that relationship.

Global scale. Local trust.

Presence in 60+ countries.

Spirax-Sarco sells through engineers, not marketers.

Local sales and service teams

On-site support

Region-specific manufacturing, where needed

High client retention through technical depth

They don’t sell parts.

They sell uptime.

Financial discipline over flash.

Gross margins: consistently >45%

Strong cash generation

Low capital intensity

Focused, application-driven R&D

Disciplined balance sheet

Growth is tied to industrial expansion and efficiency trends, not consumer cycles.

Steady beats spectacular.

Tailwinds that quietly grow the pie:

Global push for energy efficiency

Stricter emissions regulations

Industrial decarbonization efforts

Growing demand for steam system optimization

Each trend makes Spirax more relevant.

Not faster. Just inevitable.

For the patient. For the pragmatic.

Spirax-Sarco is not a momentum story.

It’s a compounding through reliability story.

Quiet execution

Global trust

Expanding install base

When heat needs to be controlled,

Spirax doesn’t pitch.

It shows up.

Niche Company #8: Heico Corp. (Ticker: $HEI)

Built to serve. Structured to endure.

Heico is a quiet powerhouse in aerospace and defense.

Specialty parts. Mission-critical systems. Performance without compromise.

Precision isn’t marketed. It’s required.

Failure isn’t an option. Heico designs to prevent it.

Speed isn’t the edge. Longevity is.

Niche focus. Broad reach.

Heico doesn’t chase scale.

It specializes in the irreplaceable.

FAA-approved aircraft replacement parts

Defense, space, and electronic components

Aftermarket support for commercial and military fleets

When reliability is non-negotiable, Heico is often behind the scenes.

Embedded through certification.

Aerospace isn’t easy to enter.

Every part demands qualification, not just production.

FAA Part 21 and Part 145 certified

PMA approvals across fleets

Parts must prove decades of safety, not months of performance

Switching isn’t just expensive.

It’s a regulatory minefield.

Qualification cycles take years

Displacing a trusted part is rarely worth the risk

Operational familiarity locks in future demand

The catalog compounds itself.

Growth is driven by expanding part coverage and deepening fleet integration.

New certified parts

Fleet maintenance cycles

Parts upgrades and retrofits

Custom electronic solutions

Ongoing support contracts

Every plane in service can create decades of recurring revenue.

Global footprint. Technical proximity.

Heico supports operators across the globe.

Sales happen through technical relationships, not advertising.

Direct engagement with airlines, defense agencies, and OEMs

On-site technical presence

Fast-response aftermarket teams

Strong customer stickiness through certification depth

They don’t sell inventory.

They sell trusted continuity.

Disciplined financial engine.

Gross margins: consistently strong

Asset-light model

High ROIC through niche leadership

Conservative balance sheet

Serial acquirer of high-quality bolt-ons

Heico doesn’t chase trends.

It compounds by owning critical small spaces.

Tailwinds through time.

Heico quietly benefits from:

Global fleet expansion

Increased aircraft utilization

Defense modernization cycles

Growing demand for cost-effective, certified aftermarket parts

Each structural trend pulls Heico forward, steadily and predictably.

For the patient. For the precise.

Heico isn’t built for stock screeners.

It’s built for longevity, trust, and operational excellence.

Embedded through regulation

Grows through specialization

Compounds through recurring demand

When fleets need to fly,

Heico isn’t an option.

It’s the solution.

Niche Company #7: Markel Group (Ticker: $MKL)

Built patiently. Scaled deliberately.

Markel Group is a quiet compounder.

Insurance, industrials, and niche businesses are woven into a decentralized holding.

Consistency isn’t a slogan. It’s the playbook.

Optionality isn’t a bet. It’s designed in.

Agility isn’t a risk. It’s how Markel compounds.

Structured for endurance. Positioned for flexibility.

Markel is not just an insurer.

It’s a carefully assembled ecosystem.

Specialty insurance and reinsurance

Markel Ventures: wholly owned businesses

Long-term equity portfolio

It’s Berkshire-inspired.

But built in its own lane.

Embedded through specialization.

Markel doesn’t underwrite everything.

It focuses on hard-to-price, hard-to-place risks.

Niche markets

Low competition

Underwriting-driven culture

Switching providers is often not worth the effort.

Markel’s value isn’t price—it’s understanding the risk others can’t.

Long underwriting cycles

Deep domain expertise

Relationship-driven retention

The portfolio compounds quietly.

Markel’s growth engine runs on three flywheels:

Specialty insurance: underwriting profits, not premium scale

Markel Ventures: non-insurance businesses with steady cash flows

Investment portfolio: equity-heavy, long-term focused

Each arm reinforces the other.

Each arm compounds independently.

Decentralized. Close to the ground.

Markel empowers local leadership.

It doesn’t micromanage from headquarters.

Markel Ventures runs through autonomous operating companies

Insurance teams specialize by market and geography

Capital is allocated where it earns the best long-term return

They don’t buy headlines.

They buy durability.

Financial discipline. Structural compounding.

Insurance combined ratios: consistently below 100%

Investment returns: long-term, equity-biased, Buffett-style

Ventures businesses: steady, cash-generative, often family-owned acquisitions

Conservative balance sheet: long history of resilience

Growth isn’t fueled by debt or cycles.

It’s fueled by patience and precision.

Tailwinds through optionality.

Markel benefits from:

Rising specialty insurance demand

Growing investment leverage through float

Long runway for small private acquisitions

Embedded pricing power in niche markets

Each flywheel feeds the others.

Each decision widens the moat.

For the patient. For the thoughtful.

Markel is not built for traders.

It’s built for owners.

Embedded in specialty markets

Compounding through underwriting, ownership, and investment

Growing through steady, often unnoticed acquisitions

When others chase scale,

Markel quietly builds resilience.

And let time do the work.

Niche Company #6: Games Workshop (Ticker: $GAW.L)

Built with obsession. Grown by devotion.

Games Workshop is not a typical retailer.

It creates, controls, and curates a universe.

Creativity isn’t outsourced. It’s protected.

Customers aren’t buyers. They’re lifelong hobbyists.

Growth isn’t transactional. It’s community-led.

Focused product. Expanding world.

Games Workshop doesn’t sell toys.

It sells a rich, ever-evolving universe.

Warhammer 40,000

Warhammer: Age of Sigmar

Middle-earth Strategy Battle Game

The company doesn’t chase trends.

It builds depth that pulls people in—and keeps them.

Locked in through passion.

This isn’t a casual hobby.

It’s a lifestyle.

Players invest hundreds of hours painting, building, and learning.

Rules evolve, armies grow, and loyalty compounds.

Switching isn’t a choice. It’s starting over.

Games Workshop builds barriers through:

Deep lore

Continually updated rule sets

Vast miniatures catalog

Emotional investment from the community

The ecosystem sustains itself.

Revenue streams are tightly interwoven:

Miniature sales

Paints, tools, and hobby supplies

Rulebooks, codices, and expansions

Licensing across video games, TV, and more

Direct-to-consumer stores and online platforms

Every new release revitalizes the base.

Every hobbyist becomes their own marketing engine.

Global reach. Intimate connection.

Presence across continents.

But the magic happens locally.

Company-owned retail stores

Hobby centers that drive community engagement

Global fan events and tournaments

Strong online and social presence

Customers don’t just buy models.

They live in the universe.

Financial engine driven by discipline.

Gross margins: consistently >65%

Tight cost control

Minimal debt

Focused R&D on core games

Direct distribution powers profitability

The company doesn’t burn cash on hype.

It reinvests in world-building and production scale.

Secular tailwinds with unique resilience.

Games Workshop benefits from:

Growing global tabletop and hobby gaming demand

Increasing digital monetization through licensing

Strong pipeline of cross-media expansions (TV, video games, publishing)

Long-term growth of niche, high-engagement communities

The fanbase isn’t fleeting.

It’s generational.

For the builder. For the believer.

Games Workshop is not about speed.

It’s about depth.

Fans build armies.

The company builds worlds.

Both build loyalty that lasts decades.

When others sell products,

Games Workshop sells belonging.

Niche Company #5: Brown & Brown (Ticker: $BRO)

Built with discipline. Scaled through consistency.

Brown & Brown is an insurance broker that quietly compounds.

It connects businesses to coverage—efficiently, reliably, relentlessly.

Relationships aren’t optional. They’re the core product.

Growth isn’t spiky. It’s methodical.

Scale isn’t the story. Execution is.

Laser focus. Broad exposure.

Brown & Brown isn’t in the business of underwriting risk.

It’s in the business of solving it.

Retail brokerage: commercial and personal lines

National programs: specialized insurance solutions

Wholesale brokerage: niche markets, hard-to-place risks

Services: claims, risk management, and consulting

Each arm feeds the next.

Each strengthens the flywheel.

Embedded through trust.

Insurance brokerage isn’t bought on price.

It’s earned through service.

Brokers are long-term partners, not vendors.

Switching costs are rooted in familiarity, not contracts.

Clients rely on brokers to navigate complex, changing coverage landscapes.

Retention isn’t enforced.

It’s maintained through performance.

A platform that expands itself.

Growth comes from both sides:

Organic: new clients, expanding coverage, upselling services

Acquisitive: bolt-on brokers, niche specialists, local footprints

Key drivers:

90%+ retention rates

Cross-selling across divisions

Localized autonomy paired with centralized efficiency

Decentralized leadership with clear accountability

Every acquisition widens reach.

Every renewal deepens roots.

National scale. Local feel.

Brown & Brown operates across the U.S. and beyond.

But wins by staying close to the client.

Local offices with decision-making power

Relationships built face-to-face

Deep community presence in mid-sized markets

They don’t sell policies.

They sell confidence.

Financial rigor. Operational excellence.

Consistently high operating margins

Lean cost structure

Minimal capital needs

Strong, predictable cash flow

Proven discipline in capital allocation

The business isn’t built on underwriting risk.

It’s built on handling it efficiently.

Secular growth with compounding stability.

Brown & Brown quietly rides:

Growing insurance complexity

Rising risk awareness across industries

Increasing demand for personalized brokerage support

Ongoing consolidation in the fragmented brokerage space

Each trend feeds the broker’s role.

Each cycle builds resilience.

For the steady. For the disciplined.

Brown & Brown isn’t chasing headlines.

It’s building a network.

Broker by broker

Client by client

Year by year

When others sell coverage,

Brown & Brown sells clarity.

And keeps showing up when it matters.

Niche Company #4: Ametek (Ticker: $AME)

Built for precision. Scaled by design.

Ametek is an industrial technology leader.

It builds the instruments and motors that power essential systems worldwide.

Precision isn’t an add-on. It’s the baseline.

Scale isn’t the headline. Reliability is.

Growth isn’t cyclical. It’s engineered.

Focused niche. Global relevance.

Ametek doesn’t chase volume.

It specializes in the critical.

Electronic instruments: measurement, monitoring, testing

Electromechanical systems: specialty motors, pumps, and engineered materials

Core markets: aerospace, medical, power, factory automation, and more

Where accuracy matters, Ametek matters.

Embedded through specification.

These aren’t plug-and-play products.

They’re designed into the system from the start.

Long product validation cycles

Deep engineering collaboration with OEMs

High switching costs due to qualification and integration complexity

Replacement is costly.

Not in price, but in process disruption and performance risk.

A portfolio that drives itself.

Ametek’s growth engine runs on two tracks:

Organic: product innovation, deeper market penetration, operational excellence

Acquisitive: bolt-on purchases of high-margin, niche technology companies

Key levers:

Embedded customer relationships

Aftermarket servicing and upgrades

Cross-selling across divisions

Repeat business from expanding industrial bases

Every acquisition strengthens capability.

Every new spec locks in future demand.

Global platform. Local execution.

Ametek sells worldwide.

But it wins by being close to the application.

Technical sales model

Local engineering support

Broad geographic footprint

Multi-decade customer partnerships

They don’t sell catalog items.

They solve precision problems.

Financial consistency. Disciplined growth.

Gross margins: consistently strong across cycles

High free cash flow conversion

Minimal capital intensity

Long track record of accretive M&A

Balanced, disciplined capital allocation

Ametek doesn’t swing for the fences.

It compounds by stacking durable, high-quality businesses.

Structural tailwinds. Durable demand.

Ametek benefits from:

Increasing demand for precision measurement

Global industrial automation trends

Aerospace and medical equipment innovation

Growing energy efficiency and safety regulations

Each secular driver feeds the need for their instruments.

Each customer win can last decades.

For the precise. For the persistent.

Ametek isn’t chasing flash growth.

It’s methodically building an advantage.

Specialty niches

Embedded products

Repeatable, scalable execution

When others sell equipment,

Ametek sells precision.

And keeps delivering where it counts.

Niche Company #3: Tatton Asset Management (Ticker: $TAM.L)

Built with intent. Scaled with care.

Tatton Asset Management is a quiet enabler of UK financial advisors.

It delivers investment solutions that free advisors to focus on clients.

Simplicity isn’t a product. It’s the value proposition.

Scale isn’t noisy. It’s deliberate.

Growth isn’t forced. It’s earned.

Focused offering. Expanding platform.

Tatton doesn’t try to be everything to everyone.

It specializes in what advisors actually need.

Discretionary Fund Management (DFM)

Model portfolio services

Investment management through low-cost, scalable solutions

Adviser platform support through Paradigm

The strategy is sharp.

The execution is focused.

Embedded by design.

Advisors don’t switch lightly.

Tatton makes it easy to stay and hard to leave.

Seamless platform integration

Competitive fees

Consistent investment performance

Ongoing regulatory and technical support through Paradigm

Switching costs are practical:

Operational disruption, client migration hassle, and time spent rebuilding trust.

The model compounds itself.

Tatton’s growth engine is self-reinforcing:

Assets under management (AUM) grow with new advisor inflows

Paradigm strengthens advisor relationships

Operational scale drives margin expansion

High client retention leads to long revenue tails

Every advisor onboarded increases AUM.

Every relationship deepens the moat.

National presence. Local trust.

Tatton is deeply embedded across the UK advisory landscape.

Partnered with over 900 adviser firms

Strong regional representation

Advisor-centric service teams

Multi-channel support across platforms

They don’t sell funds.

They sell simplicity, support, and peace of mind.

Financial strength. Operational discipline.

Gross margins: consistently strong

Capital-light model

High cash generation

Minimal debt

Scalable cost base

Tatton doesn’t need financial engineering.

It compounds through predictable, asset-linked revenues.

Tailwinds with structural stability.

Tatton quietly rides:

Ongoing shift towards outsourcing investment management

Increasing regulatory burden on financial advisors

Consolidation in the UK advisory market

Rising preference for low-cost, model portfolio solutions

Each advisor transition strengthens Tatton’s relevance.

Each regulatory step increases their value.

For the steady. For the strategic.

Tatton isn’t built for headlines.

It’s built for quiet, high-quality growth.

Scalable platform

Sticky advisor base

Repeatable, cash-generative model

When others compete on complexity,

Tatton wins by making it simple.

And by standing exactly where the advisor needs them.

Niche Company #2: Graco Inc. (Ticker: $GGG)

Built to last. Scaled through precision.

Graco is a quiet leader in fluid handling.

It designs equipment that moves, measures, and controls fluids with exceptional accuracy.

Performance isn’t optional. It’s engineered.

Downtime isn’t tolerated. Graco prevents it.

Growth isn’t rushed. It’s carefully layered.

Narrow focus. Broad application.

Graco doesn’t chase categories.

It dominates specialized fluid management.

Paint and coatings spraying

Lubrication systems

Industrial pumps and dispensers

Process equipment for precise material handling

Graco’s reach spans industries:

Automotive

Construction

Food processing

Manufacturing

Energy and beyond

If it sprays, pumps, or moves fluids, it’s likely a Graco system.

Embedded through process control.

Graco’s equipment becomes part of the production line.

It’s not a tool that gets swapped out. It’s built into the workflow.

Switching risks of production stoppages

Equipment integrates with specific materials and systems

Reliability, consistency, and serviceability drive customer loyalty

Once installed, replacement is rare.

Service and upgrades keep customers in the ecosystem.

The install base compounds itself.

Graco grows through two levers:

Organic: product innovation, process improvements, geographic expansion

Acquisitive: bolt-ons that strengthen niche dominance

Key drivers:

Aftermarket parts and servicing

Replacement cycles for wear-intensive equipment

System upgrades tied to efficiency gains

Cross-selling across industries and geographies

Each sale is an entry point.

Each install expands lifetime value.

Global scale. Local reliability.

Graco operates worldwide but wins by being close to the floor.

Local distribution networks

On-site technical support

Rapid-response service teams

Deep partnerships with equipment integrators

They don’t sell products.

They sell uninterrupted operations.

Financial discipline. Operational consistency.

Gross margins: consistently strong

Low capital intensity

High cash conversion

Disciplined M&A

Debt minimal, balance sheet clean

Graco doesn’t chase financial gimmicks.

It compounds through reliability, scale, and steady reinvestment.

Tailwinds with industrial durability.

Graco quietly benefits from:

Global manufacturing growth

Rising demand for efficiency and precision

Tightening environmental and material control standards

Continued automation across industries

Each trend increases Graco’s relevance.

Each production upgrade can create decades of demand.

For the persistent. For the process-driven.

Graco isn’t built for rapid cycles.

It’s built for endurance.

Products that last

Relationships that stick

Revenue streams that quietly expand

When others sell equipment,

Graco sells precision.

And becomes part of the process itself.

Niche Company #1: Dino Polska (Ticker: $DNP.WA)

Built from the ground up. Expanded one store at a time.

Dino Polska isn’t a blitz-scaling retailer.

It’s a disciplined supermarket chain with local loyalty at its core.

Growth isn’t a land grab. It’s methodical expansion.

Pricing power isn’t shouted. It’s quietly earned.

Scale isn’t the strategy. Accessibility is.

Local by nature. National by footprint.

Dino Polska thrives in Poland’s heartland.

It doesn’t need to dominate big cities—it wins in small towns.

Small-format, conveniently located stores

Fresh products, everyday essentials

Tight, repeatable store model

The formula is simple:

Build stores where people live, not just where traffic flows.

Deep roots in the community.

Dino isn’t just a store. It becomes part of daily routines.

Proximity drives frequency

Product mix fits local demand

Private label and fresh counters create stickiness

The shopping habit forms quickly.

The switching incentive is low.

The model scales itself.

Dino’s growth engine is straightforward but powerful.

Company-owned store network

Standardized layouts for fast replication

Integrated logistics and distribution centers

High control over the supply chain

Focused, predictable expansion strategy

Each new store feeds the distribution system.

Each new region increases purchasing leverage.

Close to the ground. Fast to build.

Dino doesn’t rely on franchising.

It owns the process from site selection to store operation.

In-house real estate development

Streamlined construction teams

Rapid store openings in underdeveloped regions

Local hiring builds community trust

They don’t chase flashy locations.

They place stores where people need them.

Disciplined growth. Strong financial backbone.

Gross margins are protected by private label and tight cost control

Consistent cash flow generation

Self-funded expansion

Conservative balance sheet with low leverage

Focus on volume and repeat traffic over high-ticket sales

Dino doesn’t rely on debt or promotional pricing.

It scales through operational excellence and local density.

Structural tailwinds. Local resilience.

Dino benefits from:

Urbanization of smaller towns

Rising disposable income in rural areas

Low competition in its core markets

Shifting consumer preference toward convenience and proximity

As Poland modernizes, Dino’s relevance grows.

As regions develop, Dino’s footprint deepens.

For the builders. For the patient.

Dino Polska isn’t a momentum story.

It’s a story of careful, ground-level growth.

Store by store

Region by region

Habit by habit

While others aim to dominate metros,

Dino quietly becomes indispensable everywhere else.

Before you go!

Follow me on X/Twitter so we can interact. 😌

🔥 Ready to go from reading about great businesses to owning them with conviction?

You’ve just gotten some of my archive of the best gems that no one talks about…

Now imagine having the full edge—every single week:

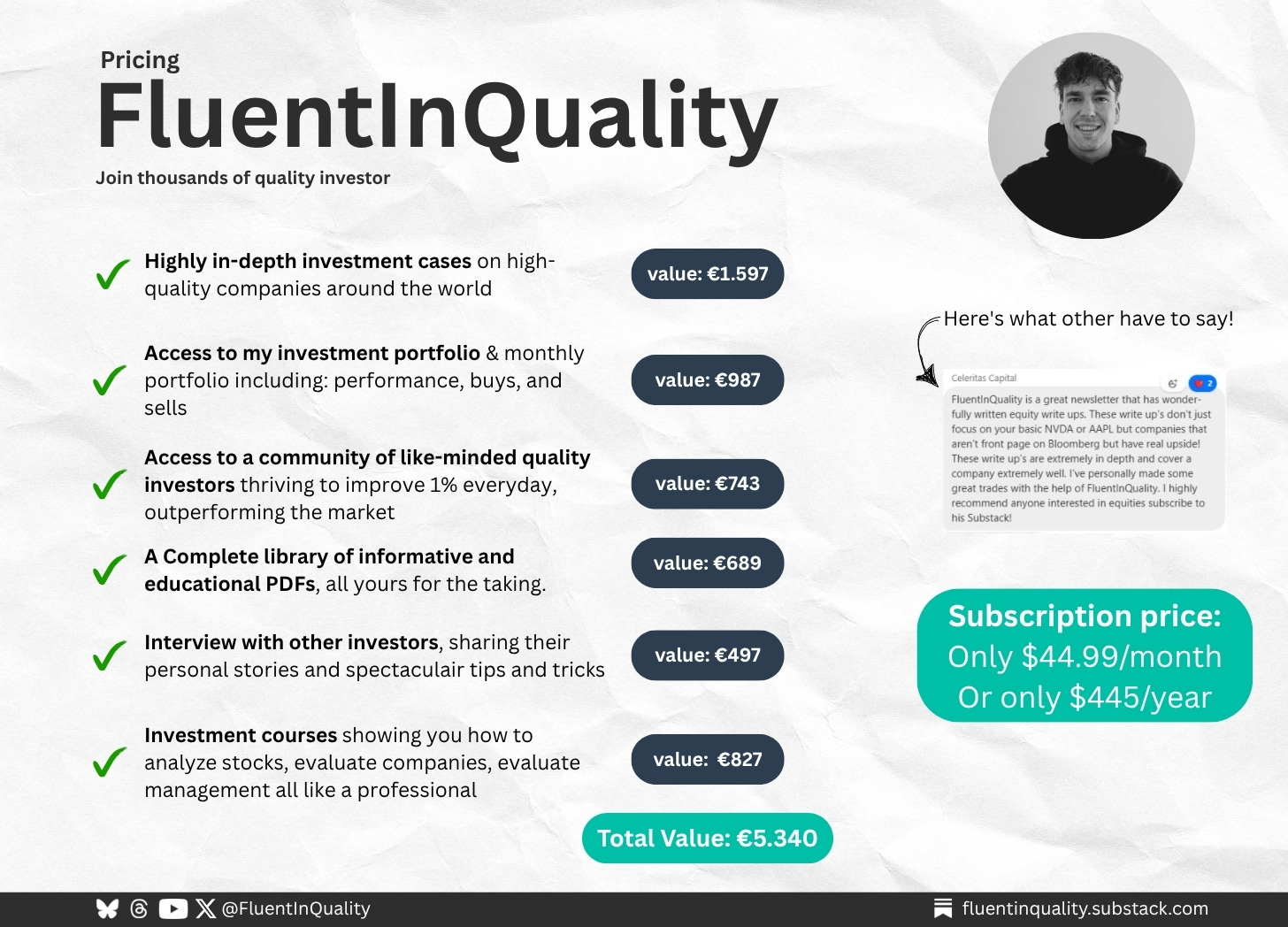

✔️ Full research reports and timeless deep dives (valued at €1,597)

✔️ Monthly buy/sell portfolio updates with commentary (€987)

✔️ Access to a private Discord of high-conviction investors (€743)

✔️ Tools, templates, investor interviews & PDF briefs (€2,013)

Total value: €5,340 — yours for just €44.99/month or €445/year.

No fluff. No noise. Just real work, trusted by 1,200+ long-term investors.

This isn’t just insight. It’s an investing advantage.

Delivered weekly. Backed by research. Built to compound.

🟢 Become one of The Fluent Few

Let’s build wealth the right way—brick by brick.

PS…. if you’re enjoying FluentInQuality, can you take 3 seconds to refer this edition to a friend? It will go a long way in helping me grow the newsletter (and bring more quality investors into the world).

Great investments don’t shout, they compound quietly.

- Yorrin (FluentInQuality)

Sources I Recommend

I use Finchat for all the charting, analysis, and keeping up with earnings calls. You can now get 15% off your subscription. Click here and start today!

Disclaimer

By accessing, reading, or subscribing to my content—whether on Substack, social media, or elsewhere—you acknowledge and agree to my disclaimer. Read the full disclaimer here.