10-Minute Breakdown: Nu Holding Ltd

Everything you need to know about Nu Holding in a digestible format!

Have you ever watched the Netflix series Money Heist (La Casa de Papel)?

If you have, you probably remember how The Professor carefully orchestrates every detail of the heist — from recruiting a team of outsiders to outsmarting a powerful system that was never built to be challenged.

Now imagine doing that… but instead of robbing a mint, you're disrupting the entire Latin American banking system.

That’s Nu Holdings in a nutshell.

Founded by a Colombian, backed by global capital, and powered by technology, Nu is leading a digital revolution in a region where traditional banks have long ruled with high fees, bureaucracy, and limited access.

Like The Professor, Nu’s approach is simple: empower the people with transparency, simplicity, and control over their money — all through an app.

But is Nu just a flashy fintech with fast growth and nice colors?

Or are they truly building the financial operating system of Latin America?

Let’s unpack it.

Happy reading!

What Will be Discussed?

Business Overview

Revenue Breakdown

Key Performance Metrics

Management

Capital Efficiency by Management

Investment Thesis

Financial Snapshot

Assets Sheet

Liabilities Sheet

Financial Health Check

Cash Flow Insights

Competitive Landscape

Potential Risks

Valuation Breakdown

Final Thoughts

1. Business Overview

Nu Holdings, also known as NuBank, is a leading digital banking platform operating primarily in Brazil, Mexico, and Colombia. Founded in 2013 by David Vélez, Cristina Junqueira, and Edward Wible, Nubank has rapidly expanded to serve over 114 million customers across these countries.

Nu Holdings offers a diverse range of financial products designed to simplify and democratize banking services. Its flagship offerings include an international credit card managed entirely through a mobile app, fee-free digital accounts known as NuConta, personal loans, life insurance, and investment services. The company's user-friendly mobile platform allows customers to track transactions in real time, adjust credit limits, and interact with customer support seamlessly.

The company's mission is to fight complexity and empower individuals by providing transparent, accessible, and low-cost financial services. This approach has been particularly impactful in Latin America, where traditional banking services often come with high fees and bureaucratic hurdles. By leveraging data and proprietary technology, Nu Holdings has been able to offer innovative solutions tailored to its customers' needs.

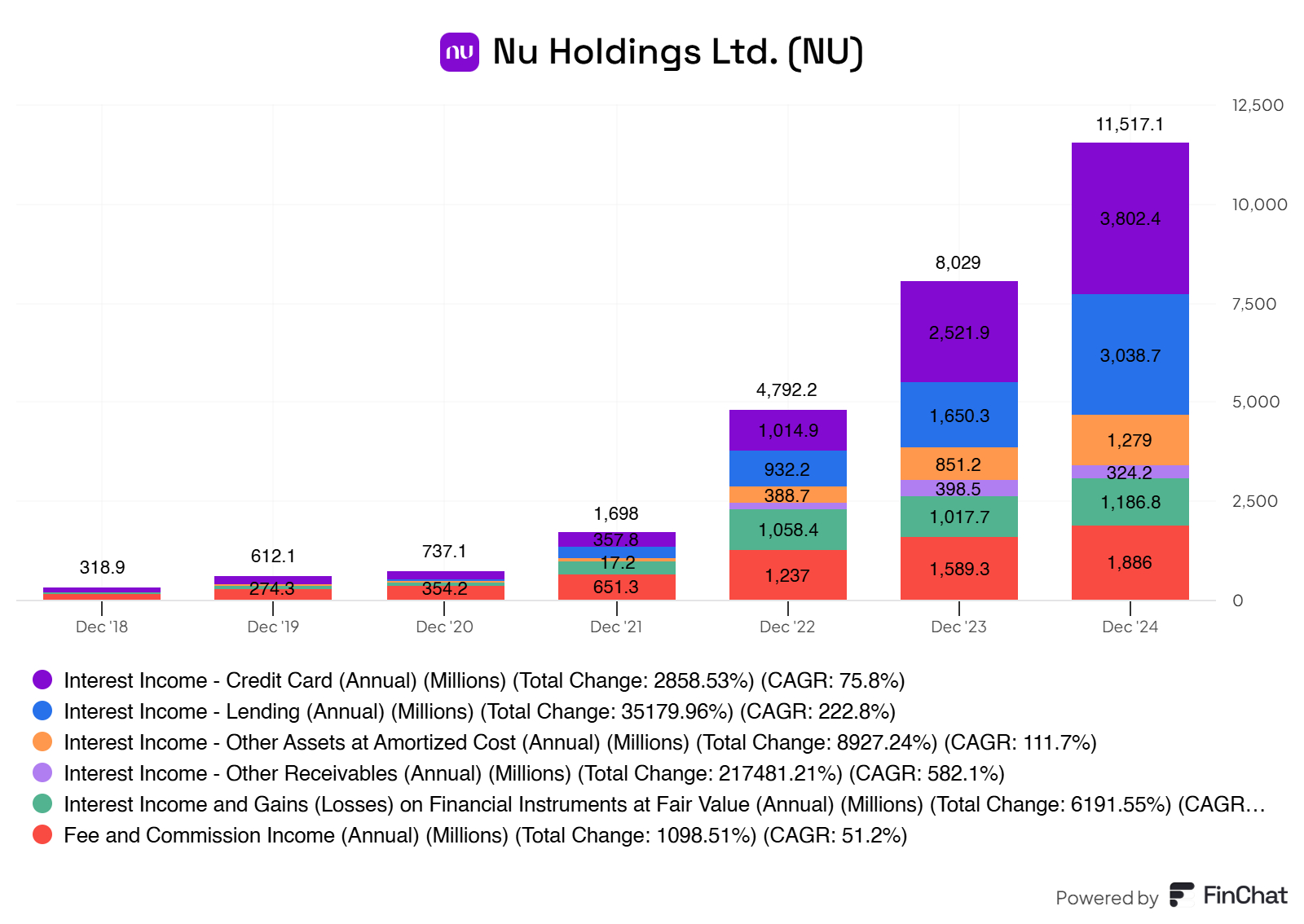

A) Revenue Breakdown

Credit Card Interest Income: Revenue comes from interest charged on outstanding balances.

Example: Maria in São Paulo uses her Nu credit card for groceries and pays only part of her balance each month.

→ Nubank charges interest on the unpaid balance — this is a major revenue driver.

Lending Interest Income: Comes from personal loans issued to customers via the app.

Example: Carlos takes out a R$5,000 personal loan via the Nu app to renovate his kitchen.

→ He repays monthly with interest — that interest goes straight to Nubank’s top line.

Other Interest Income (Amortized Assets & Receivables): These include interest from fixed-income assets and other receivables.

Example: Nubank parks some of its cash in government bonds or earns interest from customer account balances.

→ These are lower-risk sources of passive income.

Gains on Financial Instruments: Includes profits from financial assets held at fair value.

Example: Nubank holds financial assets like securities, and some appreciate in value.

→ When these assets are sold at a profit or revalued, Nu books gains.

Fee and Commission Income: Comes from interchange fees (from card transactions), insurance, and investment services.

Example: Ana swipes her Nu card at a café — Nubank earns a small fee (called an interchange fee) from the transaction.

→ Plus, if she signs up for Nu’s insurance or invests via their app, Nu earns commissions there too.

What do we notice with Nu Holding’s revenue segments?

Massive overall growth: Revenue grew from ~$319M in 2018 to over $11.5B in 2024 — a 36x+ increase.

Credit Card interest is king:

The largest and most consistent revenue driver.

Grew nearly 30x since 2018.

Reflects strong user engagement and high credit usage.

Explosive lending growth:

Lending interest income grew over 35,000%.

Suggests Nu is successfully expanding into personal loans, not just cards.

Diversified income mix emerging:

By 2024, no single revenue stream dominates.

Multiple segments are contributing $1B+ each — a sign of maturing monetization.

Fee & Commission income is solid and recurring:

Grew over 10x since 2018.

Strong foundation from interchange fees, insurance, and investment products.

TL;DR

Nu started with one strong product (credit card) and grew into a multi-segment financial powerhouse, scaling lending, monetizing payments, and leveraging financial assets — all through a digital-first platform.

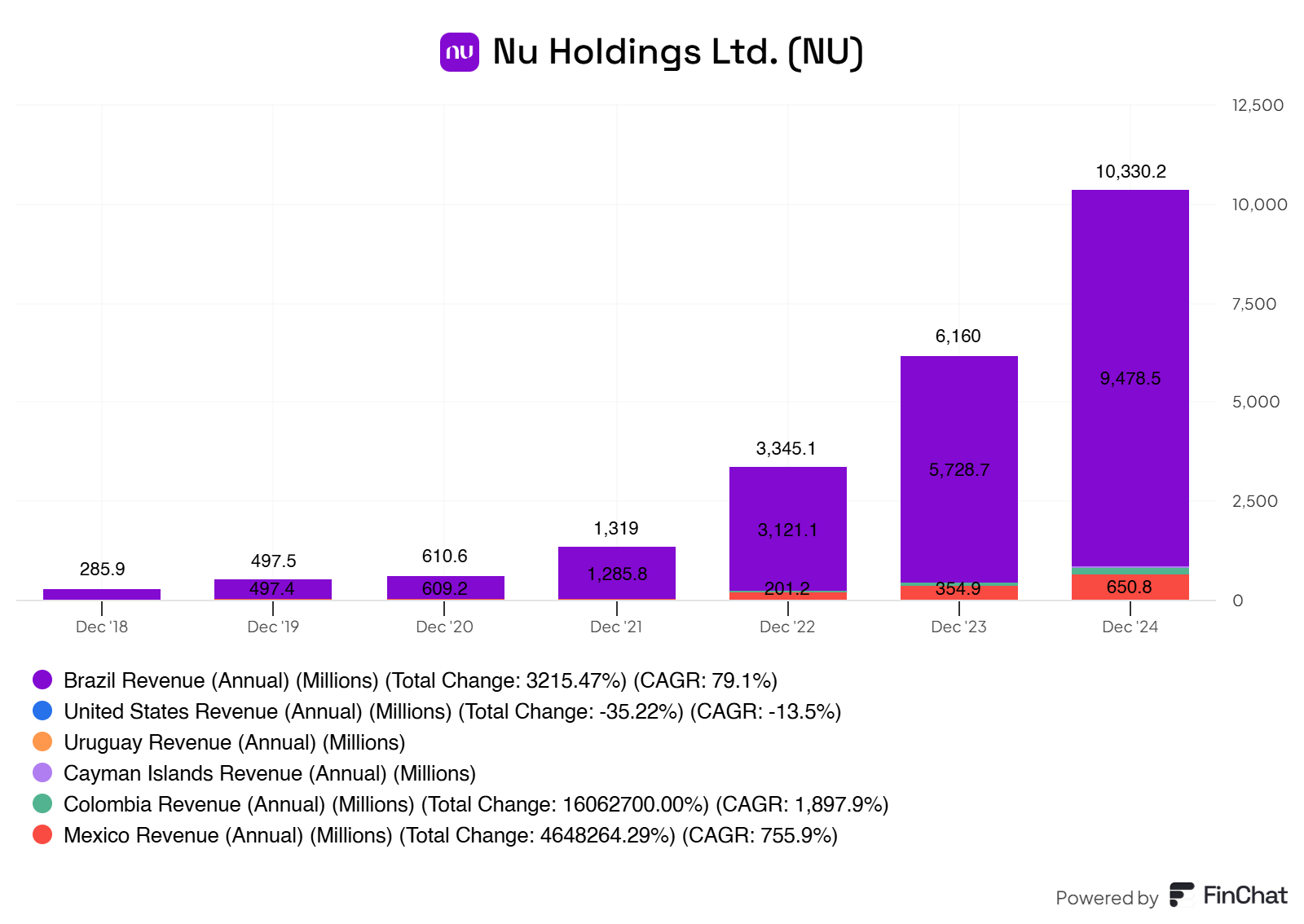

So, where is this revenue coming from?

As expected, Nu Holding’s revenue primarily comes from Brazil.

But they’re also operating and expanding in

Uruguay

Cayman Islands

Colombia

Mexico (this segment is growing the fastest)

United States

They are highly dependent on Brazil. I’m not usually a fan of such a large dependence on one country, but with Nu Holding’s efforts in expanding operations, I could let this one slide.

Nu Holdings was founded in 2013. Expecting a recently founded business to immediately have a global footprint would be absurd. Therefore, cutting some slack is appropriate. I believe, and the numbers back it up, that expansion in similar countries like Mexico (socially and economically more alike) will drive up in the coming years. Hopefully, other countries will follow along.

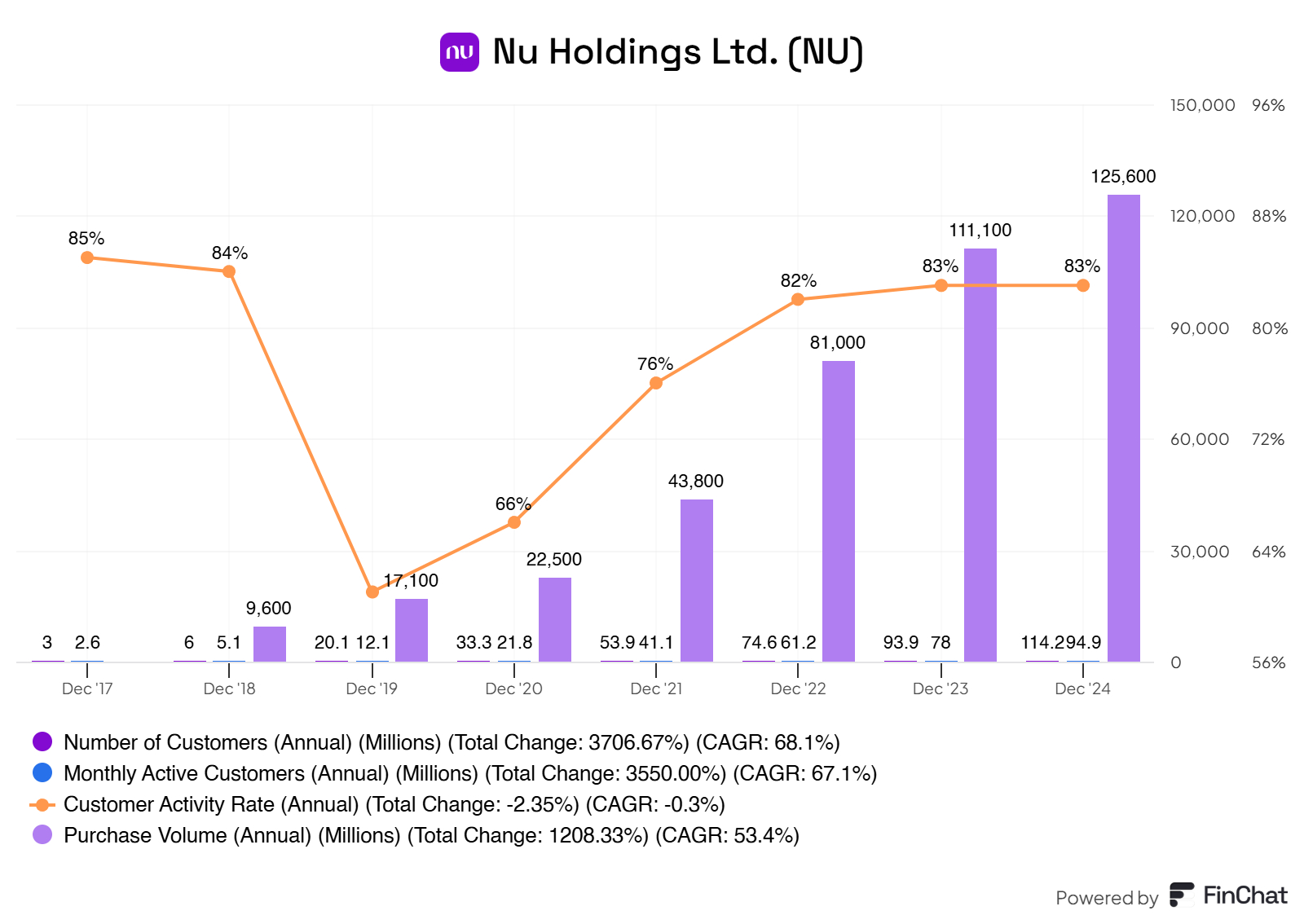

Key Performance Indicators

Let us go over the key performance indicators for Nu Holdings.

Explosive Customer Growth: From 3 million in 2017 to over 125 million in 2024 — a 3700%+ increase. Shows widespread adoption across Latin America.

Monthly Active Users (MAUs) Keeping Pace: MAUs grew nearly in line with total users—from 2.6M to 114.3 M, a CAGR of 67.1%, indicating strong user engagement, not just signups.

Customer Activity Rate Stabilizing: The activity rate dipped sharply in 2019 (down to 58%) but rebounded fast. It stabilized at ~83% from 2022 to 2024. This means 8 out of 10 customers actively use the platform—very healthy.

Purchase Volume is Soaring: It grew from $9.6B in 2018 to $125.6B in 2024 — a 1200%+ increase. Showing increased usage per customer over time.

Key Takeaways:

Nu isn’t just acquiring users — it’s activating and retaining them at scale.

The activity rate is remarkably high for a company with 100M+ users — often, this metric drops with scale.

Purchase volume growth shows rising trust and utility — people use Nu as their primary financial hub.

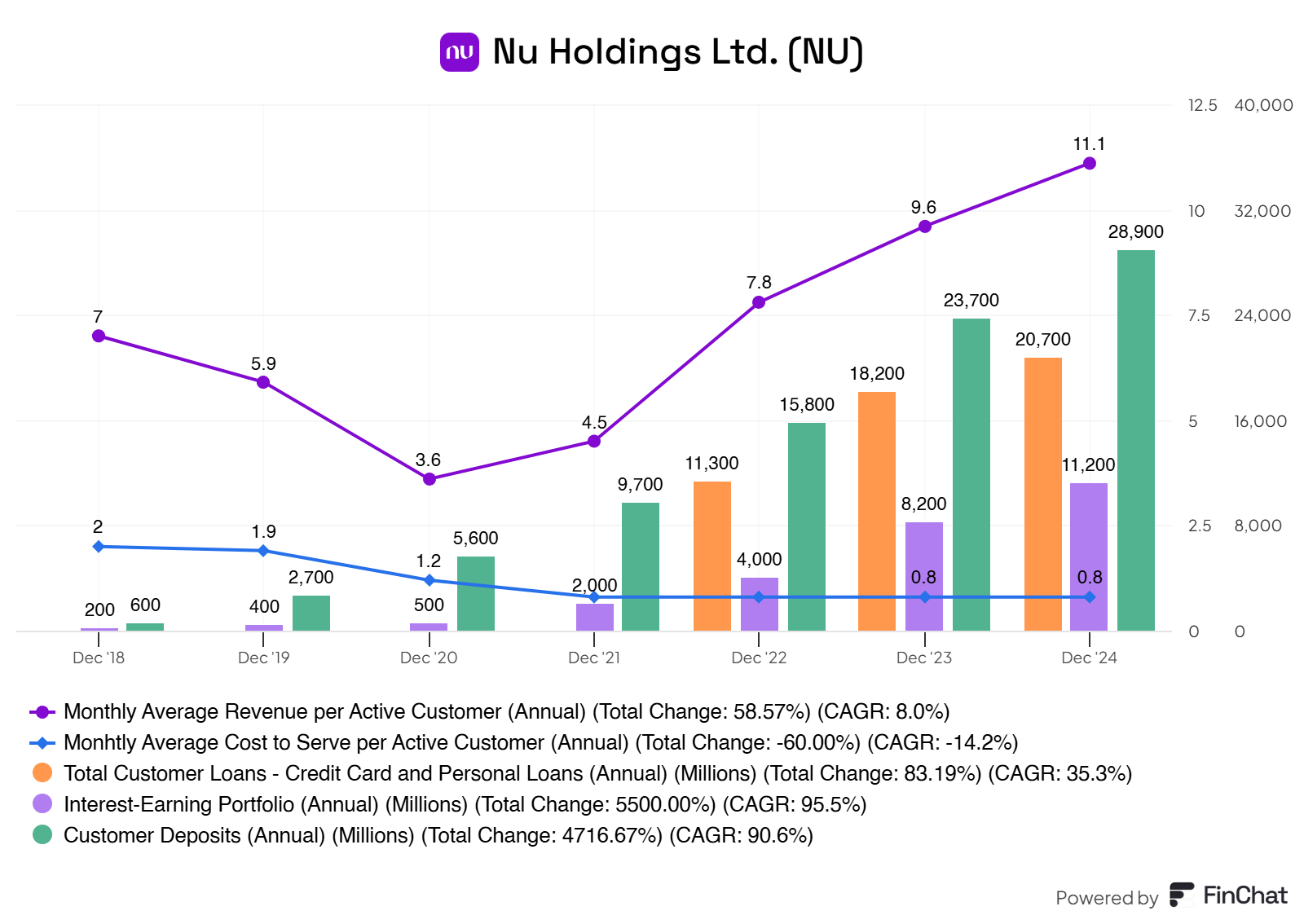

Revenue per Customer is Rising: Monthly average revenue per active customer grew from $3.6 in 2020 to $11.1 in 2024. That's a 58.6% total increase — meaning Nu is monetizing its users more effectively over time.

Cost to Serve is Shrinking: The cost per customer dropped from $2 to $0.8, a 60% reduction. This is a strong signal that scale is driving operating leverage—they're getting more efficient as they grow.

Explosive Growth in Customer Deposits: From $600M in 2018 to nearly $29B in 2024 — a 4716% increase. Suggests customers trust Nu as a safe place to park their money, not just for spending.

Customer Loan Book is Expanding: Grew from $6.1B in 2022 to $11.2B in 2024. More customers are taking credit — a strong monetization lever, but also adds risk.

Interest-Earning Assets are Surging: Interest-earning portfolio (e.g. loans, bonds, etc.) hit $20.7B in 2024. Shows Nu is increasingly deploying deposits to generate yield.

Big Picture:

Unit economics are improving: Higher revenue per customer, lower servicing cost.

Balance sheet strength is rising: More deposits and interest-earning assets.

Nu is evolving from a "fintech app" into a full-service digital bank with strong efficiency and monetization.

2. Management

Cristina Helena Zingaretti Junqueira (Co-Founder & Chief Growth Officer): Owns 2.60%, worth $1.0B

David Velez-Osomo (Founder, Chairman & CEO): Owns 0.03%, worth 12.2M

They’re significant skin in the game for all of management.

You know I have to put the famous quote in here.

‘‘Show me the incentive, and I will show you the outcome’’—Charlie Munger

Most, if not almost all, of their wealth is locked into Nu Holdings. This gives investors some peace of mind. If management makes an awful decision for the company, they’ll feel this in their own pockets as well.

Why is this important? This ensures that management is making decisions for the long term and creates actual shareholder value, company value, and value for their own wallets.

I reviewed their most recent 20-F filing to learn more about how management is compensated. Is their compensation aligned with shareholders' interests and long-term value creation?

Comp Structure: Executive compensation consists of three parts — fixed salary, profit sharing (for Brazil-based execs), and share-based compensation (RSUs and options). This mix aligns incentives with long-term shareholder value creation.

Performance Focus: Share-based comp is heavily emphasized. It’s awarded based on:

Individual and business unit performance,

Overall company performance, and

The strategic importance of performance for long-term goals.

No Golden Parachutes: Compensation is not tied to specific corporate transactions, such as a sale or merger. That’s good—there's less risk of executives prioritizing short-term deals over long-term growth.

Equity Alignment: Independent board members also receive a significant portion of their compensation in equity, promoting long-term alignment with shareholders.

Governance Caveat: Nu is a controlled company — founder David Vélez controls ~76% of the voting power, which grants him influence over major decisions, including director appointments and compensation policies. While he has skin in the game, this limits checks and balances.

Peer Benchmarking: Compensation is benchmarked against a peer group of high-growth fintech/software companies. This ensures competitiveness but could inflate pay if not balanced

Nu’s compensation structure is designed to retain talent and drive long-term performance through stock-based rewards. While this aligns well with shareholder interests, the founder's concentrated control adds governance risk. As long as performance and shareholder returns stay strong, the current setup can work — but it's something to monitor over time.

So, what do their capital allocation skills look like? Let us go over them!

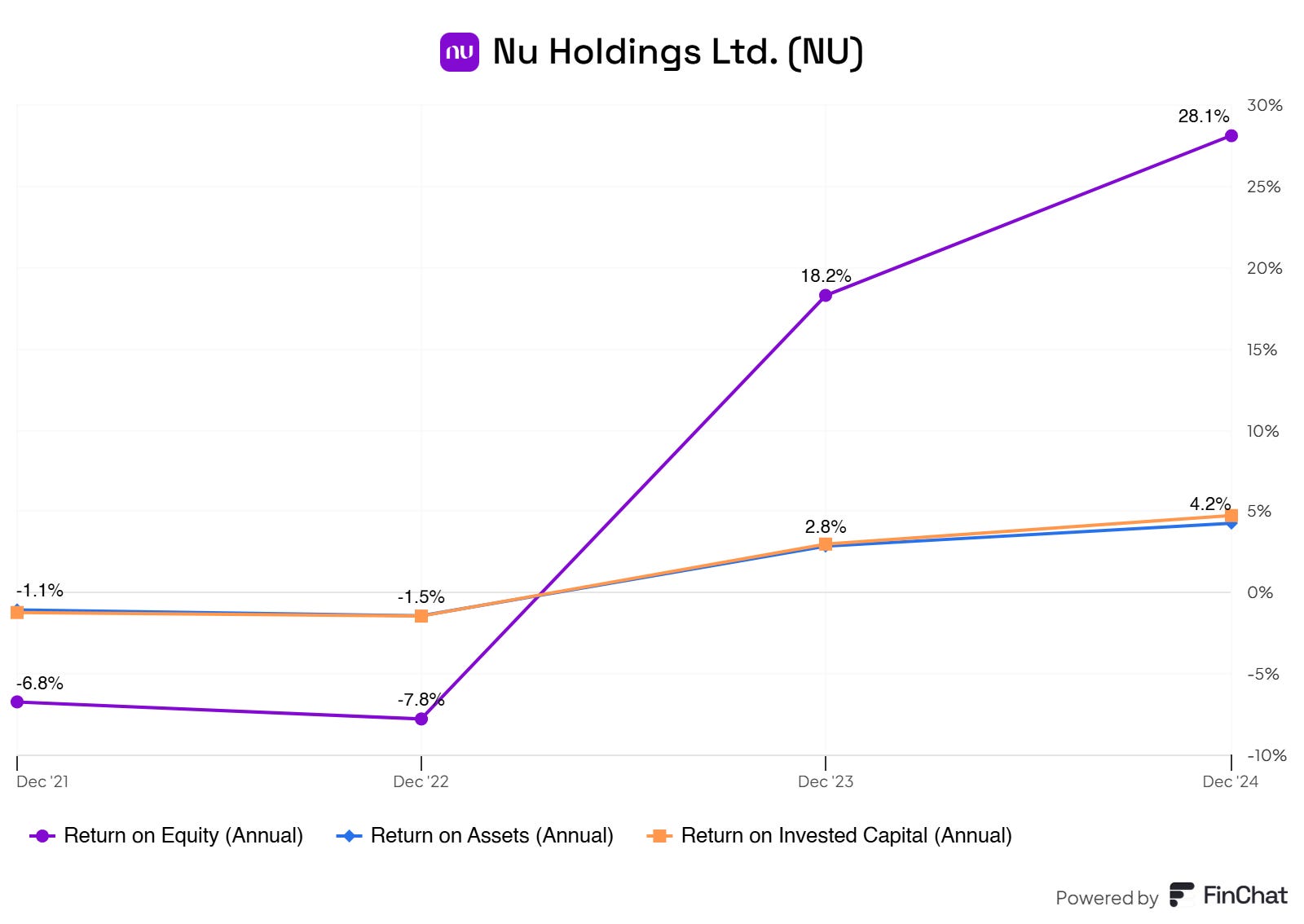

A) Capital Efficiency by Management

Return on Equity (ROE): This is phenomenal. Banks live and die by ROE. A 28% ROE is world-class, especially for a young, scaling bank. Indicates strong profitability relative to shareholder equity — they’re extracting serious value from the capital they’ve raised.

Return on Assets (ROA): ROA is especially important for banks, as their assets = loans + deposits. 4.2% is very solid — most traditional banks operate between 1–2%. Shows Nu is operating efficiently and profitably without bloated assets.

Return on Invested Capital (ROIC): ROIC measures how well Nu turns investor capital into profits. Consistent with ROA and trending positively — they’re becoming more disciplined and effective allocators of capital. As of now, not impressive but we need to remembers it’s a bank, not a software company. We can cut Nu Holding’s some slack here.

Takeaway:

From loss-making to high-return bank in 2 years — that’s a major inflection.

The rise in ROE suggests Nu has found operating leverage and can now scale profitably.

Unlike some “growth-at-all-costs” fintechs, Nu is proving it can turn scale into returns.

Nu Holdings isn’t just growing — it’s evolving into a high-quality, high-ROE digital bank.

This is where it gets interesting.

In the next section, we’ll dive into Nu’s financials, risks, and valuation — including my full investment thesis and whether I believe it’s a buy today.

This part is for FluentInQuality members only.

👉 Start a free 7-day trial to unlock it — no risk, cancel anytime.

Already convinced?

Get 33% off for life on your monthly or annual subscription.

Your edge starts here.

Pick your path:

🔵 Free Trial

🔴 33% Off Forever